Abstract

This paper compares and contrasts the process of accounting standard-setting and financial statement presentation among different accounting regulatory agencies in America. The key focus is on the SEC, FASB, IASB, and GASB because they are the main regulatory bodies in America. Comprehensively, this paper shows that these regulatory bodies share similar principles, such as transparency and expedience, in the standard-setting process. However, an evaluation of their advantages and disadvantages, in the context of how they affect the financial sector, shows that all the four organizations need to improve their response to changing accounting issues in America.

Introduction

Proper financial reporting is an integral part of the efficient performance of both public and private organizations (Sawani, 2009). Different financial bodies are responsible for ensuring the accurate reporting and presentation of financial figures in America. They include the International Accounting Standards Board (IASB), the Governmental Accounting Standards Board (GASB), the Financial Accounting Standards Board (FASB), and the Security Exchange Commission (SEC). This paper compares and contrasts the standard-setting processes of these organizations and evaluates their advantages and disadvantages, in the context of the roles they play in improving the performance of the accounting sector.

Standards-Setting Process

IASB

The IASB is an independent body that sets standards for formulating and promoting internationally accepted accounting standards. The body develops these standards through a consultative process that involves international partners (Pacter, 2014). This consultative process is the “due process” and it involves getting the views of individuals and organizations around the world about the development of accounting standards (Sawani, 2009).

The “due process” comprises of six stages that include setting the agenda, planning the project, developing and publishing the discussion paper (including public consultation), developing and publishing the exposure draft, developing and publishing accounting standards, and establishing the procedures after setting a standard. This accounting-setting process shares many similarities with the same process associated with other regulatory bodies in this paper.

GASB

The GASB’s standard-setting process closely aligns with the same process as that of IASB because they both have a consultative accounting standard-setting process. By encouraging the broad participation of stakeholders, it objectively considers the views of all people and opens up to review and criticism from independent bodies, such as the Financial Accounting Foundation (Marsh & Fischer, 2011).

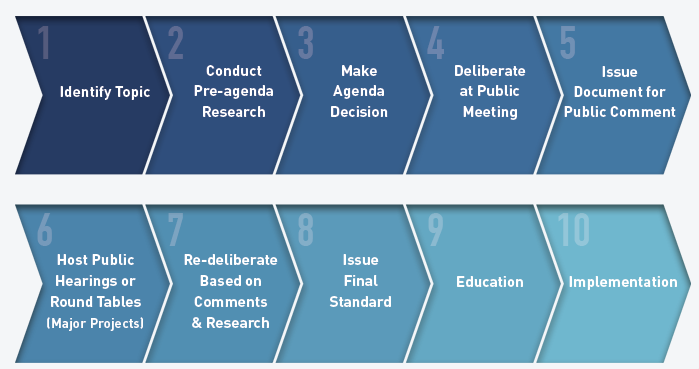

The organization’s rules of procedures allow public participation to increase the transparency of the standard-setting process (Sawani, 2009). GASB’s standard-setting process is broader than that of IASB because it involves ten stages that include topic identification, conducting pre-agenda research, making agenda decisions, deliberating at public meetings, issuing documents for public review, hosting public hearings, re-deliberating (based on emerging concerns and research), issuing final standards, education, and implementation. The diagram below provides a visual representation of the 10-step process.

FASB

Established in 1973, the FASB establishes, publishes, and updates financial reporting and accounting standards in private organizations (Marsh & Fischer, 2011). The organization is a private entity and mostly works with other accounting bodies to improve accounting setting standards in the US (Sawani, 2009). Nonetheless, its standards-setting process is similar to that of the GASB because both organizations refer to the process as “due process.”

It includes board meetings, public hearings, and soliciting comments from the public. The organization implements these processes in several stages, albeit systematically. Regarding its financial reporting standards, the FASB emphasizes the need to make financial reports useful to the users. Consequently, it strives to solicit and analyze comments from interested and knowledgeable parties (Marsh & Fischer, 2011).

SEC

The SEC regulates capital markets in the United States (U.S). Similar to the other regulatory bodies highlighted in this report, the SEC’s standard-setting process is open, thorough, and deliberate (Macey, 2010; Marsh & Fischer, 2011). The process is also independent and modeled on the private sector. In other words, the SEC often looks to the private sector for leadership in improving existing accounting standards (FASB is mostly responsible for the standard-setting process).

The regulatory body mostly looks for members of the FASB to create an oversight body that comprises of people from different economic sectors, such as investors, business people, and accountants (Macey, 2010). Presumably, these people represent the public. Therefore, the process is inclusive of all stakeholders because it contains the views of people from different economic sectors. Comprehensively, these insights show the standard-setting processes for the main regulatory agencies in the US financial sector.

Strengths and Weaknesses of the Standard-Setting Bodies

IASB

Advantages

Financial experts have lauded the work of IASB because it has helped in increasing international financial flows, as many investors find it easy to do business in different jurisdictions because of a streamlined accounting process (Pacter, 2014). The organization also promotes a globalized orientation of financial reporting that delimits organizations from thinking about national-level accounting standards only (Pacter, 2014).

Disadvantages

According to Fosbre, Kraft, and Fosbre (2009), the IASB is ineffective in overseeing its mandate because it lacks transparency, legitimacy, and accountability. These concerns stem from the lack of a democratically elected body to oversee the operations of the organization (Fosbre et al., 2009). Some observers also say that IASB does not fully integrate the views of all stakeholders because it fails to carry out proper impact assessment tests before it introduces new standards in the market.

GASB

Advantages

Experts have lauded the GASB for improving accounting standards in the public service sector (Sawani, 2009). In this regard, it helps promote civic education about government projects by improving accountability and transparency in government activities. The improvement of pension reporting is a key area attributed to the role of GASB in America’s financial sector (Sawani, 2009).

Disadvantages

Many observers agree that the scope of roles undertaken by the GASB and its process of setting standards are the main problem areas for the organization (Marsh & Fischer, 2011). For example, Pacter (2014) says that the accounting standards of GASB cast a wide net on government accounting processes, thereby increasing bureaucracy and limiting government control over its accounting processes because it has to seek the services of other parties in accounting for its finances. Some observers also argue that GASB does not have the competency needed to develop accounting standards in some sectors of the economy because of its inability to evaluate both qualitative and quantitative aspects of financial performance (Marsh & Fischer, 2011).

SEC and FASB

This paper has revealed that the SEC and FASB share many similarities in terms of their standard-setting processes and roles in the financial sector. Consequently, for purposes of this analysis, the advantages and disadvantages highlighted in the subsequent sections apply to both organizations.

Advantages

The FASB and the SEC have an enhanced information-processing system that allows stakeholders to develop accurate financial documents. As seen from the works of both organizations in improving accounting standards in the industry, observers say their ability to collaborate with other financial organizations and integrate other systems in their model is a significant advantage of both organizations (Macey, 2010). These functions, coupled with their oversight role in the industry offer immense benefits to investors, businesses, and other stakeholders in the sector.

Disadvantages

Some loopholes in the accounting standards set by both the FASB and the SEC give an opportunity for companies to understate, or overstate their financial numbers. For example, some accounting provisions developed by the FASB are conservative because they require companies to report key financial indices, such as sales, profits, and assets below the alternative approaches they should use. Such accounting flaws could lead to the understatement of financial numbers.

The treatment of intangible assets in financial statements is one area where observers have highlighted weaknesses in how FASB and SEC oversee their mandates. For example, the elimination of the pooling method for the purchase method underscores one weakness of the FASB in undertaking its roles. Such weaknesses show that these organizations have loopholes in their enforcement of accounting standards.

Conclusion

This paper demonstrates that the standard-setting process for the four regulatory institutions discussed in this paper share more similarities than differences. For example, all of them incorporate an open standard-setting process that involves the views of all stakeholders. Similarly, they all involve multiple review processes for formulating accounting standards. Their differences mostly stem from their mandates. Nonetheless, these organizations need to do more work to address some of the loopholes and ambiguities that characterize their accounting standards. Future research should investigate such strategies.

References

FAF. (2016). GASB Standard-Setting Process. Web.

Fosbre, A., Kraft, E., & Fosbre, P. (2009). The Globalization Of Accounting Standards : IFRS Versus Us GAAP. Global Journal of Business Research, 3(1), 61-71.

Macey, J. (2010). The Distorting Incentives Facing the U.S. Securities and Exchange Commission. Harvard Journal of Law & Public Policy, 33(1), 639-670.

Marsh, T., & Fischer, M. (2011). FASB/GASB Recognition and Reporting Differences: A Nonprofit Sector Perspective. Journal of Accounting and Finance, 11(1), 21-30.

Pacter, P. (2014). Global Accounting Standards— From Vision to Reality. The CPA Journal, 6(1), 8-10.

Sawani, A. (2009). The Changing Accounting Environment: International Accounting Standards and US implementation. Journal of Finance and Accountancy, 1(2), 1-10.