The IFRS Foundation is a non-governmental and non-profit making organization whose principal objectives are directed to the interests of the general public (IFRS 2011). The organization aims at developing a set of high-quality products and easy to comprehend globally accepted international financial reporting standards through the organization’s standards-setting body, IASB. The organization promotes the global application of these standards and seeks to address the needs of emerging economies as well as small and medium enterprises. IFRS foundation further seeks to bring about a convergence of national accounting standards and international financial reporting standards to generate high-quality solutions.

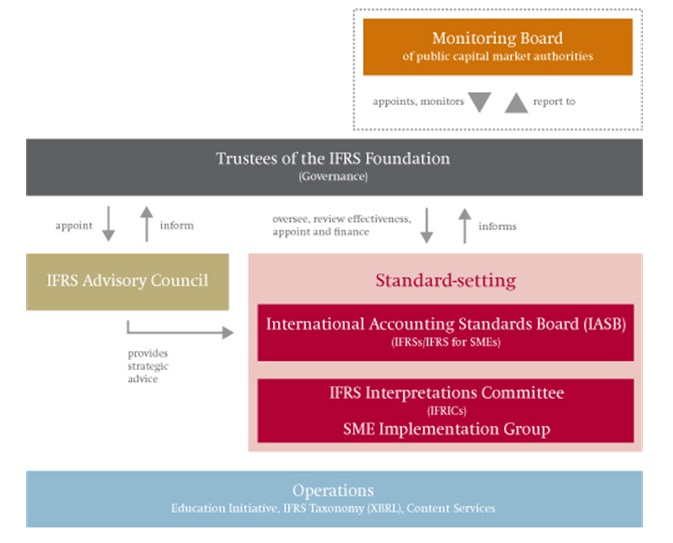

The organization’s structure takes the form as shown in the figure below.

The foundation’s operations are executed under the oversight and governance of the trustees who are publicly accountable to the monitoring board of public authorities through a memorandum of understanding (IFRS 2011). The trustees appoint the international accounting standards board which is responsible for setting standards as well as development and adoption of international financial reporting standards. Also, the trustees appoint members of the international accounting standards board, international financial reporting interpretation committee, and the standards advisory council and have the power to evaluate performance and terminate nonperforming members of the boards (IFRS 2011).

The monitoring board plays a key role in the IASC Foundation through the appointment and monitoring of the foundation’s trustees. It acts as a link between the trustees and the public authorities which is enhanced through a publicly availed memorandum of association (IASB 2008). The board actively participates in the appointment of trustees and ensures that the trustees effectively execute their duties following the foundation’s constitution.

The trustees, who are accountable to the monitoring board and the capital market authorities, are responsible for the governance of IASC Foundation operations. The trustees appoint members of IASB, IFRIC, and SAC and monitor their performance to enhance the overall performance of the organization. The trustees are further expected to have an adequate understanding of the international issues that directly impact the activities of the organization and should also promote the work of the IASB.

The international accounting standards board is charged with the responsibility of setting the standards as well as the development and implementation of IFRS (IASB 2008). The board comprises fifteen members who are equipped with relevant skills and experience in the standard-setting process and accounting. The board fulfills its duties through an open and transparent due process where discussions and public contribution is encouraged. IASB further engages the foundation’s investors, financial analysts, accounting standard setters among other stakeholders to further enhance its performance.

International Financial Reporting Standards Interpretations Committee is charged with the responsibility of interpreting the application of international accounting standards and international financial reporting standards and provides guidelines on other issues not necessarily addressed in the standards (IASB 2008). The committee is also expected to publish the draft interpretations for public comment within a reasonable time before finalizing their interpretation.

The International Financial Reporting Standards Advisory Council guides the international accounting standards board on agenda decisions and priorities of the board. Besides, the council provides information regarding organizational and individual views on major standard-setting projects to the IASB and further provides advice to the IASB and the trustees.

Reference List

International Accounting Standards Board, 2008. International financial reporting standards IFRS 2008, London: Kluwer.

International Financial Reporting Standards, 2011. IFRS Foundation official website, online. Web.