Introduction

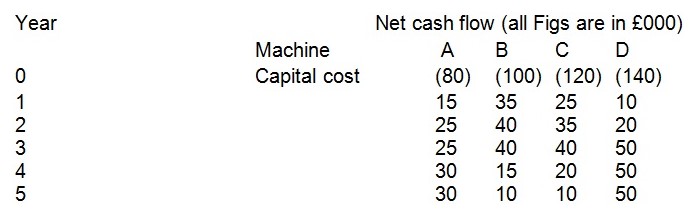

This paper is a class assignment that supposes the student to be a graduate trainee at Pevensey PLC with a responsibility to second the company’s secretary, Mary Fulton. It is considered that Mary has requested the graduate trainee to evaluate a project with respect to helping the company in purchase a machine. The graduate trainee has at the disposal 4 machines to consider (and make only an appropriate selection) – details of machines are shown as follow:

The figures presented above are estimated Net Cash Flows and have been projected based on machine operational costs for the reflected years (this subtracts from revenues). The machines (A, B, C, and D) are considered to be sold each for £10,000 at the end of a 6 year period with an exception of machine D (that would be sold for £50,000).

Funding of the project is internal and the cost of capital of the company is considered, ignoring taxation. From the data, the project is appraised using discounted and non-discounted cash flow with corresponding calculations for the benefit of the Board of Directors (BOD). Strengths and the weaknesses of the technique employed are also presented for the benefit of appropriate recommendations.

Benefit of the Appraisal

Ordinarily, companies are under the obligation of making purchases, utilizing opportunities, and implementing projects that are sure of enhancing value for shareholders (Frankly 2000). In any case, it is common to find situations whereby the availability of capital for the purchases of projects are limited and have to be effectively managed using techniques that would actualize more returns and value within a given period of time.

For Pevensey PLC, an appraisal for purchasing the machine is more essential not just for returning value but also to put the BOD members abreast of the vitality of the purchase of the machine.

Used Analytical Tool: Net Present Value

The various machines have their values in an estimate that uses the Discounted Cash Flow (DCF) valuation. According to Bhandar (2003), DCF is appropriate for finding the Net Present Value (NPV) of the machines. And the valuation requires the estimation of the size/timing of various increments in cash flow for purchase of the machine. NPV has been noted to significantly interrupt the discount rate; hence the selection of an appropriate hurdle rate is essential for arriving at a reliable decision (Modiglini & Miller 1958).

It is given that each of the machines is sold for £10,000 at the end of a 6 year period, with an exception of machine D that would be sold for £50,000. As an acceptable return on the purchase, the hurdle rate reflects the risk that is involved with making a purchase of a more value oriented machine – this basically measures the volatility of the amount of money committed to the project, and takes into consideration the mix of the project-financing.

Peel & Bridge (1998) however suggested the use of other models including CAPM and/or APT which are also very effective for the estimation of discount rate for such project like the evaluation of machine purchase requirements. The suggested models utilize the Weighted-Average–Cost-of-Capital (WACC) which in most cases is a reflection of a considered financial mix (Huikku 2007). It is known that in choosing a DR for a particular purchase decision; the WACC would be applied to the whole company (Baumol 1999; Chan 2004). However, a more advanced DR could be a better option when there is an indication of a high increment in risk that could envelope the company.

The use of an IIR as a DR is capable of ensuring a zero NPV. Using an IIR would ordinarily ensure the measurement of efficiency of the cost of the machinery and also have an equal effect on the decision that has been supported by the NPV approach (particularly, this is possible in a situation whereby the environment is not constrained). It is opted that when the decision is arrived at from an IRR and is grater than the hurdle rate, then the evaluator has to accept such as been valid. However, when a certain project is mutually exclusive, then the generally recognized decision-rule that takes into account a project with higher IRR could be reversed such that the machine with a lower NPV would then be accepted.

When the present value of the project’s net cash inflows are in excesses of the outflows, then the NPV has to be positive and the project is to be accepted. The following formula was used in calculating the discount factor:

- DF = 1/(1 + r)n

The Table below reflects NPV:

There are however certain instances whereby the NPV DR could have numerous zeros, as such rendering the IRR non-unique. The uniqueness of the IRR is precedent by a net investment of over a year period (in our case however the period is six years) and is been complimented by the net revenue. In a situation whereby the cash flow signs have changed repeatedly, there is the possibility of an existence of more than a singular IRR. Copper noted the limitation of the IRR equation in solving every analytical situation, except it is helpful through the use of iterations (Copper 1999).

A pronounced shortcoming of IRR as an approach happens to be that it is usually easy to misunderstand in terms of conveying the factual profitability (especially for something like a machine to be purchased). This happens not to be emergent in the case of this study due to the fact that there is almost no reinvestment of an intermediate cash flow for the machines; hence the factual rates for the return would definitely be reduced. The noted fact therefore suggests the need for the usage of a modified-internal-rate-of-return (MIRR).

Although, academically, the NPV has always been preferred for usage, studies have shown that IRR has a generally more acceptable usage (Farragher, et al 1999; Steven 2003) – but both could also be made use of in concert.

In an environment where resources are constrained, there is need for an efficient measure to be adopted for maximization of the general NPV of the company. Quite a number of analysts do consider it rather intuitively appealing to carryout evaluations that present percentages of the rates for the returns.

Strengths and the Weaknesses of the Technique Employed

The following are noted:

Weakness

- Difficult to understand

- Can give misleading answers if negative cash flow in later years

- Interpolation or complex math

Strengths

- Managers familiar with percentages

- No need to predict discount rates

- Requires exercise of judgement

Recommendations

In order to ensure stability of a company, economically, effective decision making as a resource is vital and must be systematical and analytical backed by sound judgment. This paper has presented an appraisal, based on capital budgeting, for the purchase of a machine and involves an assessment of how feasible the decision arrived at is backed by DCF as an analytical tool.

I would recommend for Pevensey PLC, through the company’s secretary Mary Fulton, that among the 4 machines considered, machine A should be purchased based on its low NPV.

Reference List

Baumol, W 1999, Business Behaviour, Value and Growth, Macmillan, New York.

Bhandar, S 2003, ‘Discounted Payback: A Criterion for Capital Investment Decisions’, J.Bus. Manage, vol. 14 no. 3, pp. 10-31.

Chan, Y 2004, ‘Use of Capital Budgeting Techniques to Capital Investment Decisions in Canadian Municipal governments’, J. Bus.Fin.Account.vol. 24 no. 2, pp. 40-58.

Copper, W 1999, ‘Capital Budgeting Models Theory vs Practice’, Bus.Forum, vol. 26 no. 2, pp.15-18.

Farragher, E, Kleiman, S, & Sahu, A 1999, ‘Current Capital Budgeting Practices’, Eng. Econ. Vol. 44 no. 2, pp. 137-310.

Frankly, L 2000, ‘Decision Action: Using the Financial Appraisal profile’, J.Chart.Manage, vol. 3 no. 4, pp. 36-44.

Huikku, J 2007, ‘Explaining the Non-adoption of Post-Completion Auditing’, European Accounting Review, vol. 16 no. 2, p.363-398.

Modiglini, F & Miller, M 1958, ‘The cost of Capital, Corporation Finance and the Theory of Investment’, Am.Econ.Rev, vol. 48 no 3, pp. 261-295.

Peel, M & Bridge, T 1998, ‘Capital Budgeting Practices: A Survey’, Manage.Account, vol. 45 no 11, pp.20-47.

Steven, M 2003, Economics: Principles in action, Pearson Prentice Hall, New Jersey.