Growth of store branding in the US over 25 years

Based on recent reports, private label products are vital to the growth of retailers. In the past, private label brands competed with the national brands using the price-value proposition. With the tag of generic product offerings, they often attracted lower prices than the national brands. Moreover, they instilled less inspiration, trust, and confidence in consumers in the earlier monopolistic market. In spite of all these revelations, private label brands grew in the US by offering low priced options to other consumers. The scenario made retailers to push continuously for more generic product offerings into diverse classifications of marketplace since private label products signified high margins and assure profitability regardless of the marketing initiatives (Fernie, Moore, & Fernie, 2003). Overtime, store branding in the US has become more sophisticated with retailers in private label products developing and vending their own goods.

The changes in market dominance made national brands to compete vigorously for the same customer with the store brands. Notably, the earlier viewed monopolistic market filled with trust and confidence for national brands changed gradually to a liberal one. Store brands could easily employ price reduction strategies to tap into the consumer market share of the national brands. On the other hand, the national brand counterparts used product differentiation strategies to remain relevant in the constantly changing consumer market; they did this in collaboration with right retail partners (Floor, 2006). The US market, just like the European market, has witnessed massive competition in which store brands are taking on their national counterparts, and the latter fighting back using different strategies. The desire to boost profits and margin has pushed retailers in the US market to design and implement complex and aggressive strategies. In addition, they want to build strong brand equities, seal the breaks that producers are not satisfying, as well as remain relevant in the competitive market.

The approaches have seen consumers shift their loyalty to acquire products that meet their needs; the consumers are opening their doors to retailers. According to the GfK Roper Reports, over 80% Americans have knowledgeably bought a private brand, and approximately half of the 80%are purchasing more private products nowadays than they did in the past. This reputable organization has been carrying out studies on buyer purchasing behaviors and attitudes since 1973. Therefore, it has unquestionable data. In one of the reports, consumers agreed that they used to go for “name brands” despite the high prices. However, the trend has since changed with 62% revealing that they bought store brands during their last shopping outings in the month of December 2008 (Landor Associates, 2011). In a research ordered by the PLMA in 2009, GfK found out that even with the improvement of the economy, 9 out of 10 US residents would not stop purchasing private brands. This research together with another one commissioned by Future BuySIM showed how national brands are facing fierce competition from their private counterparts. Even though a comparison of price and value gives the national brands a competitive edge over the store brands, 60% of American consumers agreed that store products are better than the national brands. Moreover, 40% of those interviewed by GfK admitted that they were unable to detect the difference between national brands and private brands (Mullick-Kanwar, 2012). Of those interviewed, 39% agreed that products from private brands were more interesting than national brands given their unique products in the market.

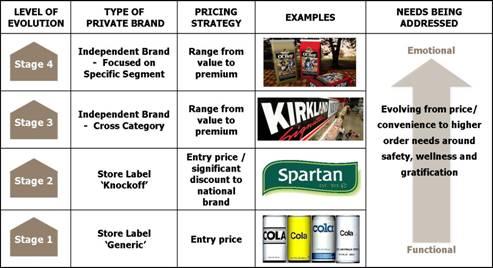

An analysis through a consumer need-state lens reveals how store branding has evolved overtime in the US. Consumers agreed that private brands provide unique items, hence satisfying the diverse tastes and preferences of the expansive American population (Silverstein, 2012). These local outlets also have correct timing in releasing their products to the market, giving them a great competitive edge over their national counterparts. As Blessing (2010) notes, store branding was the starting point for private brands in the US. Their evolution has threatened the monopolistic position of the national brands in the market threatened. Markedly, their entry pricing has been the major strategy in infiltrating the monopolistic market. Taking an example of President’s Choice cookies, consumers agreed that the product taste better than other dominant national brands. This report marked the drastic change for private brands to diversify their strategies in order to capture the attention of the market. The table below by Blessing (2010) shows the evolution of some private brands.

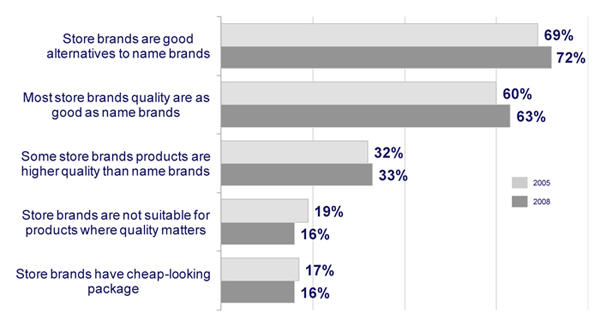

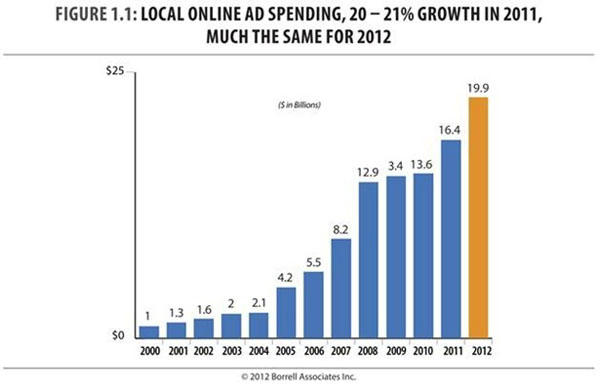

The graphs below illustrate how the store brands are gaining entry into the market with consumers changing their preferences, as well as the changing margins in local online spending. From the graphs, quality of brands appeared significantly with consumers admitting that the quality of most store brands matches that of national brands.

Why are so many retailers active in this type of marketing?

The evolution in the US market is taking the shape similar to what had occurred in the UK. Retailers are evolving to a point of acting as manufacturers. They are highly active in the market to get consumers’ feedback and preferences. In responding to the needs of consumers, private brands tailor products that meet consumers’ needs. With the analysis of the situation in the UK, retailers in the US are relying on the continuous evolution that is taking place in the market, and the trend is expected to continue into the future (Schneide, 2002). Several retailers have noted changes like consumers’ desire for value, distinct market segregation, as well as consumers’ openness to sound-completed brands.

Consumers in today’s economy are dynamic; they remain loyal only to outlets that consider their needs when manufacturing products. The desire for value plays a critical role in making consumers change their preferences in buying products. The increasing trend has seen consumers prefer private brands to national brands. Therefore, retailers are capitalizing on the increasing consumer base. For example, Hale (2014a) noted that by the end of 2013, out of the $643 billion retails sales, the US retail landscape had reached $112 billion. Since the country is still in the path of economic recovery due to the effects of the 2007 Economic Recession, the value is still below market expectation. With the high number of consumers preferring private brands, retailers are aiming at marketing their products using this option in order to gain consumer loyalty. Notably, between 2009 and 2013, sales in the private brands registered an increase of one share point, indicating the potential that the marketing option still has in the expansive US market (Paine, 2010). The European market took this same path in its growth. A scrutiny of the unexploited potential in this sector has made retailers remain heavily active in this type of marketing even with the sluggish growth of the economy. Moreover, the inactive relation between retailers and manufacturers that has existed overtime is significant to the massive interest of retailers in the private brands (Karolefski, 2002). With increased consumer reservations on spending on food, as well as lack of continuous flow of innovative products has made retailers, like Starbucks, to copy the giants in the field to sell products that meet the expectations of consumers at a low cost.

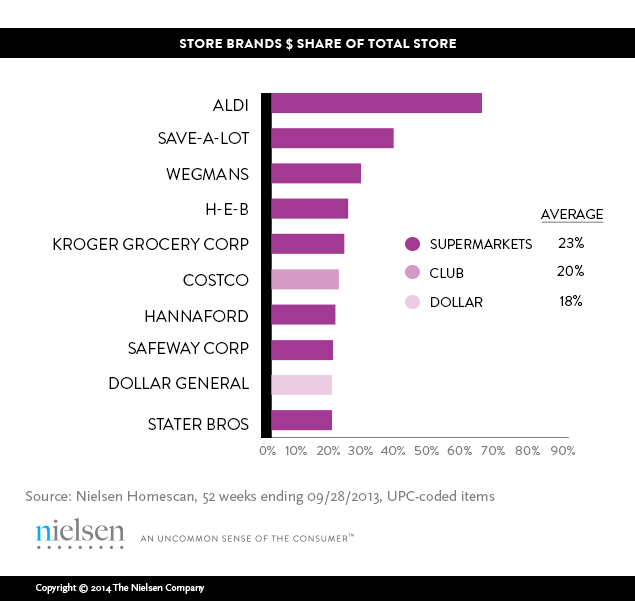

An analysis of 10 store brand retailers in the US have revealed how marketing of this nature has been fruitful. The graph below shows the performance of the 10 store brand retailers in terms of the average private-label dollar share.

The graph shows that private brands have been successful given the initiative by retailers to convert the store brand buyers to buy from their stores. For example, Aldi has been successful in converting the highest number of consumers to purchase in its stores (Peckenpaugh, 2013).

Retailers have segregated the market in terms of age, lifestyle, and gender. With this approach, consumers are turning their focus on the private label (Private Label Growth for Consumer Product Companies, n.d.). In the GfK report of 2009, consumers agreed that the penetration of private labels has been due to enhanced retailer capabilities. Retailers are taking advantage of the consumers’ position in rating store products as having similar qualities as the national brands. Therefore, the high interest has pushed retailers to invest heavily in the premium store brands. In terms of perceptions and attitudes, consumers’ sentiments had improved between 2008 and 2009, pushing up the search for store brands (Hale, 2014b).

Most consumers have agreed that store brands are essential in their daily lives, and they are not for people on tight budgets anymore. From the analysis, retailers have moved in to develop premium brands to meet the continuous needs of consumers (Store-brand groceries now on premium shelves, 2013). Moreover, spot-checks on the presence store brands revealed that some segments have high rewards. This scenario has made retailers to invest in this type of marketing; they can tailor their products to fit the available market size. Besides, some store brands having high selling categories do not require strong and expansive marketing muscles (O’Brian, 2014). This has made it possible for retailers to venture in this marketing option. Some of these products include milk, sugar, cheese, and fruit canned.

How does a major national brand defend itself?

In response to the continuous evolution in which store brands are slightly gaining entry into the market, national brands have come up with different strategies to remain operational. In this competitive market, operators have to decide whether to “fight them or join them.” According to Hoch (1996), store brands had slightly infiltrated the market with 15% of total dollar sales in 1996. The competitive grocery environment has made national brands to view store brands as their real competitors in the national platform. Even though private brands are offering low prices to tap into the market, national brands can adopt the product differentiation strategy (Schellbach, 2014). This approach will enable them maintain consumers who prefer unique products even if the prices are high. Markedly, some consumers remain loyal to these outlets given their tags or names. As a result, as a way of maintaining market presence, the national brands should make their products easily identified among different groups of products (Ahmad, Anders, & Marcoul, 2013).

With the expansive services and engagements within national brands outlets, attempts to lower prices can result in massive losses. This approach is similar to the strategy by Pepsi Company in its bid to compete the Coca-Cola Company in the sales of soft drinks. The Pepsi Company decided to increase the quantity of the soft drinks, but left the prices intact. This strategy has worked well for the beverage company. At the same time, the national brands can move swiftly to segment their markets in terms of age, race, and gender (Schepke, 2012). In the US, different cultures view pricing differently. For example, the Hispanics and the Black Community are very concerned with the prices of commodities. In this aspect, national brands have to change even the quantity of products in order to maintain presence in the market.

Another worthwhile approach that national brands can use is separating themselves from private brands (Spector, 2013). This strategy will enable national brands to improve on quality while leaving the prices the same. The additional services such as improved packaging add value to consumers, making them maintain loyalty with the national brands. Quality is essential to most consumers when deciding on the brand to purchase with 85% of consumers interviewed by Gallup Poll in 1990 agreeing that they put quality as a factor when purchasing products (Hoch, 1996). Retailers at the national brands have to apply their economies of scale in providing price gaps – an initiative that store brands do not have the financial strength to do and remain sustainable in the market. The national brands can defend their positions by adopting this approach. National brands can as well opt to play a passive role as a way of defending their positions since rapid reactions in a highly volatile market can result in situations that are irreversible (Anselmsson & Johansson, 2014).

Conclusion

National brands have to continue investing in the brands given the high penetration power that store brands have displayed in recent times. National brands must move closer to consumers to get their issues, and address them straightaway. Even though private brands are gaining confidence in the previously monopolized market, there is need to respond continuously to consumers’ demands, as well as offer high quality products. With the numerous opportunities still unexploited in the store branding across the US and world over, retailers have to move speedily into the market to supply products that do not only meet the preferences of customers, but also ensure continuous existence with limited supervision.

References

Ahmad, W., Anders, S., & Marcoul, P. (2013). Production Arrangements and Strategic Brand Level Competition in a Vertically Linked Market. Web.

Anselmsson, J., & Johansson, U. (2014). Manufacturer brands versus private brands: Hoch’s strategic framework and the Swedish food retail sector. International Review of Retail, Distribution and Consumer Research, 24(2), 186-212.

Blessing, R. (2010). The Evolution of Private Brands. Web.

Fernie, J., Moore, C., & Fernie, S. (2003). Principles of retailing. Amsterdam: Butterworth-Heinemann.

Floor, K. (2006). Branding a store: How to build successful retail brands in a changing marketplace. London: Kogan Page.

Hale, T. (2014). Where are the Remaining Growth Opportunities in Store Brands? Web.

Hale, T. (2014). How 10 retailers are pushing private label’s potential. Web.

Hoch, S. J. (1996). How Should National Brands Think about Private Labels? Web.

Karolefski, J. (2002). Marketing and Promotion: Retail Supermarkets. Web.

Landor Associates. (2011). Web.

Mullick-Kanwar, M. (2012). The Evolution of Private Label Branding. Web.

O’Brian, H. (2014). Paper war rages between national brands, private labels. Web.

Paine, L. (2010). The evolution of private labels at retail. Web.

Peckenpaugh, D. J. (2013). Top 35 Private Label Retailers. Web.

Private Label Growth for Consumer Product Companies. (n.d.). Web.

Schellbach, R. (2014). Store Branding: How a store becomes an unmistakable brand? Web.

Schepke, J. (2012). 5 Essential Components of Localized Marketing Strategy for National Brands. Web.

Schneide, S. (2002). Private Label Brands. Web.

Silverstein, B. (2012). Are consumer brands losing their mojo to store brands? Web.

Spector, B. (2013). The evolution of a private-label brand strategy at J.C. Penney. Management & Organizational History, 4(8), 387-399.

Store-brand groceries now on premium shelves. (2013). Web.