Introduction

Successful marketing requires recognition and authority at the top decision-making level. Marketing programs must be carefully planned and based not merely on knowledge of internal corporate affairs, but also on knowledge of external environments. A homeostatic point of equilibrium between customer wants and needs, is called for on the one hand, and corporate goals and resources on the other. Business organizations are more likely to make fundamental and continuous corporate adjustments to the demands of shifting market environments. To date, relatively few have truly adopted a market orientation, despite the lip service that has been paid to marketing as an orientation in business.

Such factors as continued economic growth, increased disposable income, vigorous domestic and foreign competition, accelerating technology, automation, population decentralization, expansion, and innovation will spur the appearance of this new marketing form. Marketing is concerned with setting goals, establishing policies and programs, and implementing business action for the entire firm (Dobson and Starkey, 2004).

Its major tasks are to translate consumer wants and needs, actual and potential, into profitable products and services that the company is capable of producing; to cultivate markets to support these products; and to program the distribution activities necessary to reach the markets. Marketing is not merely a limited specialized activity of the business, but rather a perspective for the total management team. It does not function as a separate entity in the business, nor is it more important than any other primary activity, such as manufacturing or finance, yet through actual and potential sales it does establish constraints within which the other activities must be performed. The managerial approach to marketing stresses the problem-solving and decision-making responsibility of marketing managers.

Strategic Planning

Planning begins with the assumption that the institution is a uniform, intractable structure directed in minutiae by control. Although very much authoritarian, the personal nature of real authority gives way to impersonal “policies” and “procedures (Drejer, 2002). Planning becomes not a set of specific plans to be realized but a continuing desperate attempt to write enough regulations to control every aspect of the organization, to be enforced by the guardians of the establishment. And the control is strictly top-down, issuing in mandates without commensurate resources or authority; there is no bottom up, except the accountability for carrying out dictates.

The problem is that results cannot be mandated. Planning not only takes on the characteristics of the institution, it reinforces them. Rather than changing the system, planning is adapted to the defense of the system. Following Dobson and Starkey (2004) “Governing the choice between strategic options should be the notion of competitive advantage. The firm has to identify unique opportunities for itself in its chosen area” (p. 9).

Customer and consumer wants and needs are central to the marketing concept. Strategic planning must use research findings and concepts that will help in determining actual and potential wants and needs as a basis for guiding decisions. Strategy is the process of deciding how to best position the organization in its competitive environment in order to achieve and sustain competitive advantage, profitably. Strategy is formed at both corporate level (what industries/markets should we operate in) and business unit level (in what segments should we compete — and how) (Dobson and Starkey, 2004).

Different Types of Strategies

Different types of strategies allow companies to select the best approach to marketing and management. If the planning process has been faithfully followed, the strategies are obvious. They have been gradually realized by the intense and open discussions of all the other components of the plan (Drejer, 2002). Some may come directly from the internal and external analyses, but most will arise out of the critical issues.

There are, however, two technicalities that will have to be reinforced repeatedly: that is, strategies are not programmatic or operational initiatives. They are strategic, involving every aspect of the organization and establishing a context for everything within the organization. Second, they are neither categorized under the specific objectives nor arranged in any kind of priority. The main marketing strategies which help companies to achieve competitive advantage are cost leadership, differentiation and focusing strategy (Moore, 2001).

Cost leadership

Cost leaders must maintain an acceptable level of satisfaction of buyer needs. Cost leadership is often in conflict with differentiation i.e. to achieve differentiation adds cost thereby removing the potential cost leadership advantage. Low cost is where the business manages its cost base to ensure that it is the lowest cost producer — thereby either winning a greater volume of business through lower prices than competitors can sustain and continue to be profitable, or charging comparable prices and therefore achieving a higher level of profitability. The cost leadership strategy often requires a lean’ culture and is usually perceived as unattractive’ with the consistent focus on cost management and efficiency. A tendency to be production or operations led therefore emerges.

This produces a concentration on standardization of products, components and processes with the minimization of variation (Drejer, 2002). A fine balance needs to be achieved between maintaining a narrow range of products/services and meeting the varying needs of different customer groups. It is these tensions between either providing a differentiated approach to match customer need and gain competitive advantage, or pursuing cost leadership to gain profit margin and value advantage, that often leads in practice to a mixed approach. This means that the advantages of neither competitive position are achieved. This being stuck in the middle’ yields no competitive advantage and erodes the position of the business unit (Dobson and Starkey, 2004).

Differentiation

Differentiators must maintain a broadly equivalent cost base to that of competitors to achieve above-average profitability. Differentiators must select cost effective forms of differentiation, which cannot be easily or immediately replicated or leapfrogged by competitors (Moore, 2001). The differentiation strategy is often the most attractive’ in that it provides the opportunity for a more creative approach to the market. Industry wide is where the business operates across the breadth of the industry providing products/services for a wide range of customer needs. An example in the car industry would be Vauxhall with an extensive range across a broad base of customers.

For this reason the organization tends to be marketing led. It is vital in these business units that the cost/benefit analysis of any new form of differentiation is thoroughly evaluated. In addition, sensitivity analysis must be used to look at the viability of the associated cost base at different levels of sales performance and in different market conditions. The primary challenge with differentiation is one of competitor replication, where the advantage is temporary and, once replicated, becomes an increase in the industry/market cost base for all competitors. This upward migration of the cost base can over time destroy an attractive market segment (Drejer, 2002).

Differentiation and price are linked. Normally achieving differentiation enables a price premium to be charged. However, this additional price potential may be sacrificed to enable increased volume/market share to be achieved. This in itself may provide a further competitive advantage as high volume drives down unit costs. Price is also a factor which itself influences customer perception.

In certain markets/segments high price is seen as overcharging or the customer — naturally leading to lower price competitive offerings being chosen. However, in other markets/segments price is in itself a positive differentiator. In this case premium price reinforces the perception of premium product — in fact a lower price would damage the competitive positioning (Moore, 2001). Examples would be luxury cars or exclusive hotels where the tangible additional value provided, versus a lower profile competitor, is significantly less than the price premium attracted. The price reinforces the positive perception. Here brand image and exclusivity are directly supported by price. To reduce price would actually reduce attractiveness (Drejer, 2002).

Focusing strategy

Some companies choose to focus on a particular segment only. Particular segment has chosen to concentrate attention on a defined segment of the market. This is called a focus strategy. An example would be BMW pursuing the luxury car segment. Uniqueness is where the business provides a distinct basis of differentiation (uniqueness perceived by the customer and regarded as valuable) which enables business to be won and normally a price premium attracted.

The model enables us to consider the requirements of each strategy and therefore to identify action themes. For many more complex organizations operating in sophisticated markets an industry-wide’ approach locks the business into the mindset’ of differentiation or cost leadership. This may lead to inappropriate approaches being taken to certain segments of the market. Directors and managers will usually focus on sales (volume and value) and profit performance.

Future plans are often based on what has been achieved in the past with an emphasis on growth and, for larger businesses, increased market share. The impact on the business of a divergence from plan is not fully considered or even perhaps recognized. The assumptions made in any plan will never be perfect and changes may occur in many areas. Directors and managers need to understand the financial characteristics of the business — how it will respond to change. To identify these financial characteristics we need to ensure that we have the right information to enable judgments to be made (Dobson and Starkey, 2004).

Internal and external Environment of A Corporation in the Planning Process

The environmental scan sets the stage for a successful strategic planning conference and is the most important activity. The scan is usually prepared by anyone in the organization who is in a position to see the relationship of the organization to its environment. In large organizations, the strategic-planning staff complete the scan. In medium-sized organizations, the comptroller can prepare the scan, while in a small organization, anyone who has a good understanding of the organization’s environment can perform the scan (Moore, 2001). The environmental scan identifies and analyzes the key societal and demographic trends, forces, and phenomena.

All have, or may have, an impact on the formulation and execution of organization strategies. The environmental scan may also include a situation audit, which is an analysis of trends, past, present, and future, and provides valuable statistical and financial information for the development of the strategic plan (Drejer, 2002).

SWOT

SWOT is a widely used thinking framework for identifying Strengths, Weaknesses, Opportunities and Threats. It enables key factors to be visibly recorded as a high level summary of a business (or personal) situation. It is a summary that is simple but powerful. The technique is commonly used by consultants to document the key factors arising from the review of a particular project or business. The use of SWOT enables an assessment to be made of the overall internal state of a business and the direction in which it is heading, through looking at its Strengths and Weaknesses. It also enables a judgment to be made about aspects of the external business environment, which can affect the performance of the business, through looking at the Opportunities and Threats it faces in the wider world (Dobson and Starkey, 2004).

Strengths are defined as those internal qualities, assets, or conditions that contribute to the organization’s ability to achieve its mission-those things that can be capitalized on, that reflect the best of the system. For that reason, not only should those strengths that directly relate to the existing mission be considered here but also any other particular attribute that the organization has accrued.

That is to say, emphasis should not be on strengths that are comparable to other like organizations but primarily those strengths belonging only to the planning organization (Moore, 2001). A recognition of strengths is important in planning because it signals to the organization the areas in which success may be most easily compounded. Real strengths represent achievement and, therefore, are testimony to the organization’s ability to perform, as well as its potential for even greater achievement. In fact, excellence is nothing more than strength pursued to its ultimate (Drejer, 2002).

The weaknesses of a marketing organization are those internal characteristics, conditions, or circumstances that are impeding or even preventing the realization of the current mission. They are, obviously, not the opposite of strengths, although the same item may appear on both lists. Whereas strengths represent achievement, weaknesses usually indicate either a lack of performance or the inability to perform.

However, weaknesses are quite often simply the result of benign neglect. Therefore, they are not necessarily a reflection of the current capacity or intent of the organization but either its present priorities or capability. There are two provisos in the development of weaknesses. First, if an issue or a concern is not identified here as a weakness, then it should never be raised again. This should be taken as an opportunity to leave the past behind. Second, weaknesses should not be cast in the form of solutions; any suggestion that begins with “lack of” is a solution and is unacceptably premature. Contrary to a popular romantic notion, there is no advantage in weakness; the only possible benefit is sympathy. All must be either solved or removed (Dobson and Starkey, 2004).

Opportunities are those issues of time and circumstance that are uniquely those of the organization because of what it is, where it is, and when it is, and there is always just one best opportunity for truly recreating an organization. Opportunities refer to market growth potential and market development, positive and progressive changes in economic environment and demand (Drejer, 2002).

Critical issues are the juncture between the planning process and the planning discipline provide a compelling rationale for the strategic deployment of resources. Threats are negative and inevitable; in the extreme, they disable or destroy. Threats refer to external factors which have a negative impact on the marketing organization, its market share and competitive position (Drejer, 2002).

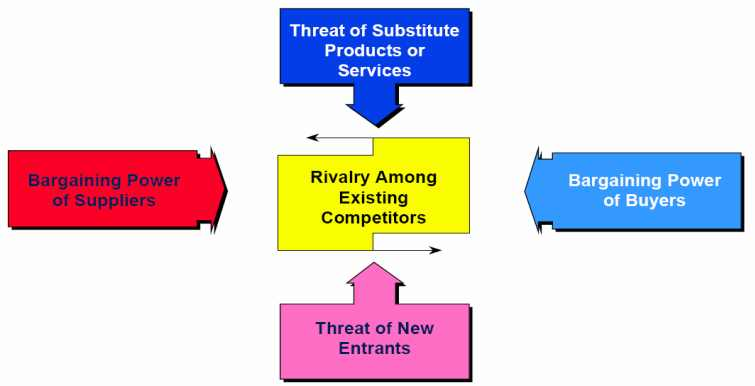

Porter’s 5 Forces

This is a model that enables the competitive environment in which the organization operates to be analyzed. It was developed by Michael Porter and is often referred to as the Porter 5 Forces’ model. It helps to identify the strength of the competitive forces that impact on the industry. Whereas the previous stage Environmental Mapping’ examined more generally the wider commercial context affecting all industries, this approach is focused on the specific industry in which the organization operates. The model identifies five industry forces that directly influence an organization (Moore, 2001).

Competition among existing firms — this is the natural competitive rivalry which exists between the various businesses operating within the industry marketplace. Threat of new entrants — this is the potential likelihood of, and ease of, entry for new firms into the market.

An example would be the entry of Japanese contractors into the UK construction market. Threat of substitute products or services — this is where a product or service, perhaps produced through a different technology, enters the market.

An example would be the entry of compact discs into the audiotape/record market — providing the same product, music’, through a different technology. Bargaining power of suppliers — this examines the relationship between businesses in the industry and the suppliers to those businesses. Where suppliers have a unique or restricted availability product they can exert a strong influence over prices and conditions of supply, therefore potentially putting pressures on the businesses purchasing their product/services. Bargaining power of buyers — this examines the relationship between businesses in the industry and the customers of those businesses. The purpose is to identify the relative strength of the business in the customer relationship (Dobson and Starkey, 2004).

The objective is to consider the industry marketplace and to identify the ability of each force’ to de-stabilize the existing situation. The power of the influence on the business of each force can then be ranked. This enables appropriate actions to be considered to take advantage of, or defend, the situation to be reflected in the strategy and plans of the organization (see Appendix 1). The structure of the industry will significantly effect the profit potential of the business operating in that industry. The strategy and actions of a business operating in the industry may improve or destroy the industry structure. Each business (and the relevant decision takers) must recognize and evaluate the impact, short term and long term, of actions taken on the overall industry structure and attractiveness (Drejer, 2002).

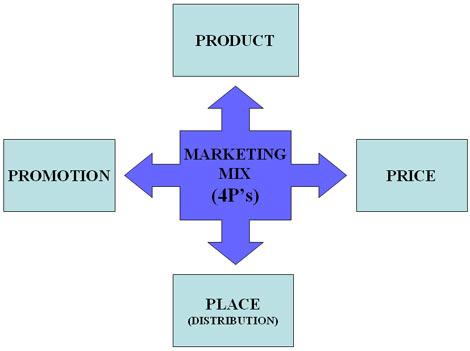

Marketing 4 P’s

Marketing mix consists of four elements: product, price, promotion and place, Product involves the adjustment of productive capacity and technology to consumer demand. Technically, it encompasses both product planning and product development, which in reality are synonymous. In consequence, we shall rely on the term product development in its broadest sense. Product development is concerned with offering the right goods at the right time, at the right price, in the right quantities, in the right place. Referring to the process of evolving new products, it is closely associated with market development.

It focuses on the future product line, on products that should be added or deleted, on the impact of products on price, promotion, warranty, and service, and on the development of criteria to evaluate product performance. By assessing new or modified products that can be added by acquisition and internal development, product development becomes the life blood of a business. Decisions in this area determine the products to be produced and stocked, as well as details concerning their appearance, form, size, package, quantities, timing of production, price lines, and anticipated market segments.

Product development combines the scientist’s function of analyzing, classifying, and organizing information into commercially feasible new products, and the marketer’s function of assessing unsatisfied wants and needs and identifying profitable market opportunities (Moore, 2001). Effective product development adopts a critical but positive posture. Management cannot be satisfied with current products, regardless of how good they are. Such an attitude and expression of expectations achieve an even better match of corporate offerings with consumer expectations (Drejer, 2002) (see Appendix 2).

Place means that a product is available at a right time at the right place. International marketing deals with geographically diverse locations so it relies on effective technology and distribution facilities. The idea is to establish effective management in multi-brand companies by developing a series of profit centers in which product executives assume responsibility for the total marketing effort for a line. This approach grows out of the inability of one executive to master the intricacies and details of marketing several dozens or hundreds of products. The large drug and soap companies pioneered the concept, and Procter and Gamble is one of the most successful in utilizing it (Dobson and Starkey, 2004).

Pricing strategies influence customers’ choice and position the company and product on the market. Although held responsible for profits, these managers generally cannot control costs of production or prices. Nor can they direct salesmen and advertising, or such supporting services as marketing research, package design, and product engineering. Authority for such activities is vested in others. Because of all these constraints, they are usually perched in a precarious position (Moore, 2001).

Promotions help companies to inform customers about new products and benefits, new discounts and product features. Promotions are a rational way of translating experience, research information, and thought into marketing action. It is a pragmatic, organized procedure for analyzing situations and meeting the future. Based on information about ends and means to determine various causal relationships, trends, and patterns of behavior, it is concerned with the selection of alternative strategies. In essence, purposeful research, experience, judgment, and decision making (all of which are directed toward guiding the corporate system and bringing it growth, survival, and adjustment) form the fabric of the marketing planning process. Marketing planning is an integrated, intelligent, rational process for guiding business change (Drejer, 2002).

How to Choose the Best Strategy

In order to choose the best strategy, the company should analyze its business environment and create clear vision, mission and objectives for further growth. Goal setting in an organizational sense is based on concepts of management planning and strategy. It includes:

- assessing the environment;

- creating a vision (defining the organization’s purpose, philosophy, mission, and goals);

- formulating strategy by setting measurable objectives, including the plans or tactics to attain those objectives;

- executing the strategy;

- controlling and evaluating the entire process (Thompson and Martin, 2005).

There are two technical devices that greatly serve to expedite the planning process: stipulations and cross-references. The first should be employed to clarify any aspect of a particular plan that was explained by the action team leader’s oral presentation but is not evident in the steps of the plan. Or, stipulations may be used by the planning team to limit or expand an action as long as the stipulations, always written directly on the plan, do not change the plan.

The planning team in this way can avoid sending a plan back to the action team. Cross-referencing is purely an administrative necessity. If it is not done during the acceptance of the plans, it will have to be accomplished later by the internal facilitator or those responsible for assigning the plans. It is simply a notation that two or more plans must be undertaken together, which raises a small but critical point (Drejer, 2002).

Many times, (almost) duplicate plans or plans that depend on each other will be presented under different strategies. They should not be combined, nor should they be eliminated. Both will be needed, in place, at the next update of the plan. So a brief note should be added to each, indicating the companion plan(s).Immediately after the session, the facilitator will debrief each action team leader individually, explain the planning team’s decisions and requests, and establish a date for any re-submissions (Dobson and Starkey, 2004).

At that time (usually one day), only the revisions of the action plans are considered. The only option the planning team does not have is returning the plans. The plans are either accepted or rejected. In addition to reviewing and selecting action plans to support the strategies, the planning team usually finds this an appropriate time to review again every component of the plan, just to confirm its own satisfaction with the content and coherence of the total plan. The final task of the planning team is to develop a recommended schedule of implementation for the strategies and plans, including a year-by-year cost projection (Thompson and Martin, 2005). The best strategy should be based on the specific goal that it supports.

The best strategy should be analyzed in terms of long-term and short-term growth of the company and possible risks. If a strategy does not support one of the goals, it will be rejected. Worthwhile objectives meet certain criteria and are achievable (Thompson and Martin, 2005). These conditions may be more stringent than they sound. Many times, too much is taken on in strategic-planning conferences, resulting in unrealistic expectations.

It is relatively easy to establish objectives at a strategic-planning conference, but when top management returns to the office, the “real issues” return to capture the executive’s time. Strategies should also be measurable in terms of quality, quantity, time, and cost. Ratios, percentages, rates, or incremental steps should be used to assess progress. While every attempt should be made to make objectives measurable, measurement is not absolutely essential. If the objectives are subjective or intangible, the successful accomplishment of the objective should be characterized or described. If a strategy cannot be measured or its successful accomplishment cannot be described, it is not a worthwhile objective (Drejer, 2002).

Strategy implementation

Typically, the implementation schedule with resource projections is a simple chart listing each plan, under each strategy, with a recommended beginning date (see Exhibit 28).It is very important that this schedule not be interpreted as assigning priorities to the plans. An organization must do all it can to realize the goals it has set for itself. It is one thing to have a vision with clear goals, objectives, and plans, but if they are to be of value, they must also be successfully executed. If strategic planning is the shadow and the spirit of successful organizations, than implementation is their flesh and blood. Much has been written about the importance of strategic planning, but planning by itself changes nothing (Dobson and Starkey, 2004).

The main stages of strategy implementation are action planning, organizational structure, human resource change, monitoring and control. Strategic management calls for a commitment to the vision of the organization. It is at this juncture that strategic plans tend to fail because chief executive officers tend to other “more pressing” matters. While there exists a strategic plan and the document accurately represents the vision of the organization, until top management gives the plan ongoing priority attention, it is just a document. The success of the planning process hinges on top management’s emphasis on following up and monitoring the plan.

The key to any successful execution is commitment. An organization needs to remain flexible to basic shifts in the environment, and it also needs flexibility to be responsive to everyday problems and opportunities. Pliable organizations capture opportunities when and where they occur. Flexibility can be inherent at the objective-setting level of the strategic plan. Allowing objectives to be changed by people at the working level creates empowered employees (Thompson and Martin, 2005). Empowered people will visualize opportunities and act to achieve results, and they form the heart of an innovative, responsive, and flexible strategic plan.

Tactics to accomplish objectives are also subject to change. The further down in the process one goes, the more valuable flexibility becomes in facilitating execution. The execution of the plan must not be stifled by bureaucratic rules and procedures. Reaching toward the goal and achieving results is what strategic planning is all about. With commitment to the strategic plan and with individual offices developing the tactics to execute it, a responsive feedback and evaluation system must now be drawn up (Drejer, 2002).

At the last stage, feedback ensures that the organization achieves what it set out to accomplish. If strategic management is a top management function and implementation a midlevel function, then feedback and evaluation belong to everyone. Feedback and evaluation are related to the whole idea of information management. Although the details of information management will be discussed later, it is important to set the general tenor of that discussion (Dobson and Starkey, 2004).

Research & Development- In Business

For a new business initiative it is essential to recognize the development stages through which the enterprise is likely to pass, and prepare for the issues and challenges which will be faced. For a business unit within a corporate it is important to recognize that the same development process applies — often with the same challenges! However, these challenges are sometimes eased by the protection of an established corporate parent able to soften the impact of negative cash flow and poor profitability at the relevant stages. Creativity becomes the responsibility of R&D, which is staffed by specialists in visualizing and realizing marginal or major product changes.

Ever since companies such as Dupont and Bell Labs first took, and successfully traveled along, this road, setting up a separate R&D group has been a popular way to enhance value at the concept stage. There are many ways of distinguishing innovations. These are based on degree of importance, breadth of application, and impact. The introduction of absolutely new products, variations of products, extension of new services, new packages, new advertising campaigns, and different pricing arrangements are all innovations. A continuum of innovation exists, ranging from very slight modification to radically new, important developments that give rise to new industries (Drejer, 2002).

Viewed from the consumer’s perspective, three types of product innovations may be delineated: fundamental, functional, and adaptive. Fundamental innovations create totally new products that have much greater impact than adaptive innovations. Where totally new products are developed, new industries are created. As a result, fundamental innovation may create a monopoly position within an industry for a period of time. For such new products, the creation of primary demand is more important than for products that are adaptations. Examples of fundamental innovations are television, airplanes, air conditioners, and dehumidifiers (Thompson and Martin, 2005).

Relationship between Marketing and R&D

Given the diversity of external demands (competitors’ actions, governmental regulations, and technological advances, in addition to pressing customer requirements) depending upon a single group, such as the self-contained R&D, could prove to be inadequate and dangerously myopic. The team could also be informally constituted where the channels for networking are indicated but no further. To assure profitable growth, companies must add new products that are tied to different phases of market development. When some products are declining, others should be enjoying market growth. Sometimes this is achieved by a merger; sometimes it is done internally (Thompson and Martin, 2005).

Regardless, the combination of the total product line as it relates to markets establishes a company’s position. Opportunity assessment, therefore, must cover a span of time, and continuously add growth opportunities to a company’s present product assortment. Technological developments and changing market environments are externally based, whereas research and development, and modifications of products, packages, marketing channels, and advertising campaigns, are internally based.

Opportunity assessment must account for both. Continued growth becomes possible by properly developing new products that fit assessed opportunities. Market opportunity considerations have resulted in the development of a new industry in the United States — an industry of discovery — the discovery of new technology, new methods, new processes and new opportunities (Drejer, 2002). Expenditures on research and development have risen sharply recently and resulted in new products and processes. Opportunity assessment requires the creation of a counterpart to research and development — a function of discovery of new markets and market opportunities that can act as a generator for innovation. This is a key function in a business. It is the driver of a business — the activity by which a business renews itself (Dobson and Starkey, 2004).

Objectives of R&D

The example of the airline industry allows to say that while individual airlines would be concerned about value construction from the time of entry into the terminal to when the passenger exits, travel agents would typically delve into how value may be enhanced by the actions of value providers all along the chain. The diverse sources of customer value would therefore be of prime importance to travel agents in selecting the respective providers (e.g., transportation to and from the airport, contractual arrangements with rental car companies, hotels, and airline reservation systems) (Thompson and Martin, 2005).

In product as well as service businesses conceptualization is indispensable to achieving high levels of value. After all, whether the firm provides vinyl binders or fast foods, automobiles or software, visualizing how value will be provided, how this will afford the firm a competitive advantage relative to its rivals, and constantly seeking to enhance the value concept, are critical to its continued success. Just as important, however, is making the concept come to life. A painter or sculptor or musician does not touch our sensibilities merely by his or her powers of imagination. The ability to communicate these images through sight, touch or sound counts for at least as much. Actually converting an idea, therefore, into a form by which others can realize value lies at the heart of value creation (Drejer, 2002).

Designing the product so that variations can be incorporated to meet local needs is one of the keys to transnational functioning. The use of modules or platforms from which product variety can be launched to satisfy local needs epitomizes the product flexibility/resource efficiency that is the hallmark of transnational firms. They are added on. While value communication is best left to local discretion, the transfer of design and development information will typically be accompanied by information that can be passed on to customers or, equally important, received from them. Caterpillar’s ability to acquire a transnational coloring has been an essential feature of its strategy to take back market share from Komatsu (Dobson and Starkey, 2004).

Types of R&D

There are three types of R&D activities: basic research, applied research and experimental development. Basic research is often used in healthcare and computer technology industries. Applied research is popular in medicine and manufacturing. Experimental development is used by all industries as a continuous process of knowledge acquisition and product development. The need to speed up introduction of the new product and to increase promotional efforts to counter the unforeseen challenge might be some of the concerns that would involve most, if not all, the members of the team (Gardiner, 2005).

The transfer of resources (primarily information in this instance) takes place in an essentially unpredictable fashion. Activities could be sources and recipients of resources depending on the stage of the project and the nature of external developments. Products gradually come to represent the results of the firm’s activities and not the essence of customer need satisfaction. Elevating the concept of efficiency-through isolation to the level of a doctrine hurts the firm’s integrity and prevents adoption of a coordinated program of action. In general, therefore, inventory strongly hinders the achievement of customer value both by reducing product worth and raising its cost. At the same time, it works toward destroying the unity of an organization that seeks to deliver value.

The overriding purpose in targeting inventories for reduction is symbolic-the realization that interdependencies have to be accepted and managed rather than eliminated. While “action plans” for banishing inventory from the shop floor may meet with early success, the success is likely to be short-lived unless it is preceded, accompanied or followed by a change of heart. Others in manufacturing, as well as in those other departments, must be viewed as essential partners in fulfilling the firm’s mission of value to its customers (Dobson and Starkey, 2004).

In functional innovations, the product or service remains essentially the same, but the method of performing the function is new. Examples are power brakes, electric knives, and gas and electric dryers. Such innovations may require considerable adjustment on the part of consumers. Adaptive innovations are the least complex and refer to such minor alterations in an existing product as package, color, design, shape, trim, and size variations. The adoptive innovation does not perform new functions for the user and does not require changes in consumer-use skills or behavior patterns (Gardiner, 2005).

Make or Buy Analysis

Cost analysis is one of the most important processes in product development. It consists of the following steps: cost identification, availability identification, quality, communication with employees and community, Various concepts of cost analysis are useful in attempting to evaluate market opportunity. Demand analysis, as we have seen in the discussion of sales forecasts, is particularly relevant.

Demand refers to the volume of sales that would occur under various conditions for a product during a period of time (Gardiner, 2005). It has several dimensions, such as the demand for a product, the demand for a brand, or the demand of a specific market segment. Market demand, which refers to the demand for a group of products that represent an industry, is distinguishable from company demand and the demand of a control unit.

Company demand refers to the demand for a company’s products and relates to market opportunity. Although it is affected by the industry demand level, it is also affected by the use of marketing tools and techniques by a firm to gain a market share. Let us note that corporate effort may also shape the industry demand. Control-unit demand refers to demand at the level of the particular unit utilized for control purposes. The unit may be a product line, specific product, brand, group of consumers or wholesale, or retail outlet. Here, demand refers to purchasing actions of a significant unit (Mintzberg et al l2004).

Assessment of marketing opportunity, the first of the systemic functions of marketing (those functions necessary to manage the marketing system), is also the most critical. It deals with both the identification and the means of attaining marketing and corporate goals. It furnishes a perspective for current and future operations. Opportunity assessment requires a good intelligence system, a sense of corporate mission, and management sensitivity to changing environments (Gardiner, 2005).

The assessment of cost may be viewed essentially as a balancing operation in the firm. It balances marketing and company resources to bring them into line with potential profit. For performing this balancing activity, economic analysis has provided us with the useful tool of marginal analysis. The marginal approach relates production schedules, investment planning, new plant and equipment, and personnel needs to market opportunity (Gardiner, 2005).

The marginal-cost principle is a guiding criterion. Marginal costs refer to changes in total costs resulting from producing an additional unit in either the physical or marketing sense. Similarly, for marginal revenue, economics explains that the most profitable position for a company is at the level of output where marginal revenue is equal to marginal costs, for it is there that profits are maximized. Profits are expressed in terms of long-run rather than short-run profits. While this is a good guiding principle for the marketing manager, the difficulty is one of obtaining marginal cost and marginal revenue data for the various options (Dobson and Starkey, 2004).

Influencing factors: Proprietariness, Timing, Risk, and Cost

Product proprietariness allows companies to achieve competitive position and deliver unique value to customers. The innovation time scale is collapsing. The time interval from perception of dysfunctioning to acceptance of innovation has been decreasing (Gardiner, 2005). This places additional pressure on management to understand more fully the process of managing change and programming innovation through manipulation of knowledge. Innovation approaches manageability when participation in the process becomes part of the continuing responsibility of all levels of management. Management must develop the appropriate environment and set of attitudes to encourage innovation. Only then can a firm hope to deploy its resources most profitably in order to meet the challenge of change (Mintzberg et al l2004).

Risks are associated with demand and purchasing power, market fluctuations and competition. The innovation interval has three phases:

- the period before the innovator’s gains are felt by his competitors;

- the time before the competitor makes an effective response; and

- the interval before the competitive response wipes out the aftermath of the innovator’s gains.

There is a difference in each interval span for different innovation categories. Fundamental innovations tend to have substantially longer intervals than adaptive innovations. For example, a competitor’s response to a price or advertising innovation can be made directly and quickly. Innovating firms face a range of possible marketing policies. At one extreme, they can choose policies to make the maximum short-run profit and then decide to meet competition as it arises as with a pricing policy of skimming markets (Gardiner, 2005).

At the other extreme, they can build a solid market position by accepting modest immediate returns and taking a longer period of time to cover their outlays, thus making it more difficult for new entries, as with a pricing policy of market penetration. Between these extremes, they may choose to be reimbursed for their original outlays while still holding a competitive advantage, and then use the advantage to increase volume and build a stronger market position (Dobson and Starkey, 2004).

The benefits of new products are often challenged. Fundamental innovations that create something new in the physical sense are hailed as beneficial. Adaptive innovations, particularly those that generate psychological values and are based on style or design obsolescence, are often criticized. Yet even the latter are beneficial in a highly industrialized economy (Mintzberg et al l2004).

Which Project to Select

For every company, the question of project selection is a crucial one because it determines its future growth and profitability. The company should select a project which accelerates progress. The space frontier will expand the risk-taking and thinking of businessmen into vast investments, with greater potential long-time commitments in global and interplanetary space (Mintzberg et al l2004). Similarly, concern with the pollution of environments will result in further development of “the ecological industries” — industries focused on the maintenance and improvement of environments and the quality.

The assessment of project opportunity is closely linked to the innovative process. Project opportunity encourages innovation and stimulates and extends markets. In fact, the assessment of market opportunity may be considered one of the early phases of the total innovative process (Gardiner, 2005). Yet innovation is not equated with market opportunity. Innovation requires the supportive system of marketing resources to cultivate opportunity. Both the stimulation of a continuing flow of ideas and products that can better satisfy wants and needs, and the supply of a marketing system to support them, are requisites of opportunity realization (Dobson and Starkey, 2004).

Introduction of New Product Line into the Market

The product line refers to the total company or division offering in a related area, and is more than the sum of individual products. Product lines are significant because they reflect the corporate image. They are important for distributor relationships, and have an impact on the consumer’s image and acceptance of a company. Product planning requires considerable lead time for change, for the addition or deletion of products. It is not uncommon to spend two to four years in developing new products, and this requires advanced market intelligence. The reasons for adding new products are

- to counteract competitive activity and assure that loss will not occur because someone else introduces the product first;

- to realize potential profitability;

- to guard against shifts in consumer tastes;

- to gain complementary relationships;

- to gain an additional share of market;

- to complete a product line; and

- to use common raw materials as well as production and marketing facilities (Gardiner, 2005).

Introducing the product line into the market involve careful planning of advertising, promotion, pricing, market position and distribution channels. Before adding a product, however, a company should establish various criteria concerning the size of the available market, the rate of return on investment, the net profit, the patentability of the item, the congruency with current corporate situations, and the impact on the sales organization.

A philosophy that competition will prevail is essential for innovation. For management expects new developments to destroy existing product positions. Assuredly, firms want to secure future opportunities and “capture” markets. New products are developed for this purpose. Innovations result in two groups of forces, competitive and monopolistic. The monopolistic forces, or the delayed action of competition, offer the innovator incentives to innovate.

The competitive features diffuse the benefits of past innovations into the public domain (Grant, 1998). This puts the innovator under pressure to make further innovations if he is to maintain his competitive advantage and the better-than-minimum profits that go with it. Innovation is, then, one of the competitive tools of the business firm. It is a major means of creating a differential advantage, albeit sometimes short-lived. In adjusting to change, and in attempting to meet the demands of the marketplace, it must be managed, and programmed innovation is becoming one of the foundations of business strategy. Programmed innovation is an extremely important process that involves great amounts of resources and effort in promoting and accelerating economic change (Dobson and Starkey, 2004).

Conclusion

In sum, marketing depends and relies on strategic planning and industry analysis. It is possible to say that marketing planning, a critical management activity, cannot logically be separated from assessment of opportunity. It brings a coordinated effort to the enterprise, adjusting and balancing its resources, and producing programs of logical action. Since marketing executives are faced with the necessity of utilizing scarce capabilities and resources in limited periods of time, allocation is a major problem. Effective allocation can only be achieved, however, through planned behavior.

Marketing planning requires sales projections for such periods as one, three, five, and ten years ahead. These projections predict customer and competitor reactions; attempt to gauge acceptance for new products; and highlight economic, social, demographic, technological, psychological, and political changes, all of which are difficult tasks to perform -nor can they be performed with the degree of precision available in other more concrete situations.

References

Dobson, P., Starkey, K. (2004). The Strategic Management: Issues and Cases. Blackwell Publishing.

Drejer, A. (2002). Strategic Management and Core Competencies: Theory and Application. Quorum Books.

Gardiner, P. (2005), Project Management: A Strategic Planning Approach. Palgrave Macmillan.

Grant, R. M. (1998). Contemporary Strategy Analysis, (3rd edn.). Oxford: Blackwell.

Mintzberg, H., Lampel, J. B., Quinn, J. B., Ghoshal, S. (2004). The Strategy Process. Pearson Education.

Moore, J. L. (2001). Writers on Strategy and Strategic Management: Theory and Practice at Enterprise, Corporate, Business and Functional Levels. Penguin Books Ltd.

Thompson, J. L., Martin, F. (2005). Strategic Management: Awareness, Analysis and Change. Thomson Learning.

Appendix