Background information

The concept of Cost of Quality (COQ) has been part of the globalised business environment for more than half a century (Rasamanie & Kanapathy 2011). Nonetheless, quality has been part of human existence and has continued to evolve over time (Crandall & Julien 2010). As such, it is apparent that COQ is a vital aspect of running businesses in the highly competitive business environments in the world. For any business venture to attain success and survive competition, quality must be integrated into all its undertakings.

It is prudent, therefore, for business stakeholders to ensure that quality is part of business. In the course of attaining quality, nonetheless, costs are incurred. On the other hand, if the correct procedures are not adhered to and compromise product quality, the probability of incurring losses are extremely high.

Some quality experts argue that quality is free (Sower et al. 2007). The proponents of this view suggest that money and resources are lost because of not doing things in the right manner for the first time (Sower et al. 2007). Cost of quality, therefore, is the loss incurred or the expenses accrued due to non-conformance and doing and not adhering to proper guidelines. Joseph Juran, a quality expert, suggested that all costs that would be avoided if there were no quality issues that sum up to what is termed as cost of poor quality (Sower et al. 2007).

Quality costs can be classified according to their sources and nature. It is worth noting, however, that there is no a single agreement on classification of costs. A common classification technique groups quality cost into prevention, appraisal, internal failure, and external failure. The typology is commonly known as PAF (prevention, appraisal, and failure) and is adopted by experts in cost of quality in different countries, including the US and the Great Britain (Sower et al. 2007).

The PAF model provides relatively comprehensive but precise definitions, which are commonly adopted by experts in COQ and business stakeholders.

Definition of costs

Prevention costs are endeavours and efforts put in place to avert poor quality in products and services (Fons 2012).

Appraisal costs are linked to efforts geared at measuring/evaluating/auditing products and services to guarantee conformance to quality criterions and performance principles (Fons 2012).

Internal failure costs are the consequences of products and services having compromised/poor quality before their delivery to the consumer/customer.

External failure cost result from product/services failing to meet the set quality prerequisites after delivery/shipment to the end user (Fons 2012).

Other typological techniques used in COQ include the model of possibilities costs; process cost model; and the Activity Based Cost model (Snieska et al. 2013).

Literature review

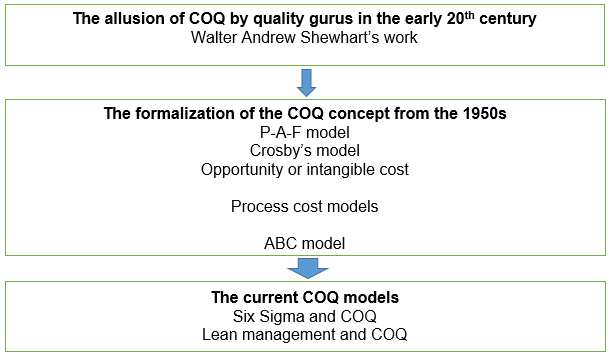

The inception of COQ can be attributed to various quality gurus. Several philosophers/researchers have made significant contributions since the 1930s (Giakatis et al. 2010). The pioneers either came up with new ideas or made vital modifications to the COQ concept.

Allusion to COQ from the 1920s

In his work, Walter Andrew Shewhart, alluded to what can be termed as quality control, which is a vital element of the COQ concept. Shewhart provided a diagram that paved the way for quality control in the manufacturing field (Giakatis et al. 2010).

Shewhart categorised problem into assignable-cause and chance-cause variation while using control chart as a differentiating mechanism. In addition, Shewhart pioneered the use of scientific formula, principles of probability and statistics. The Shewhart’s model was useful in differentiating between acceptable and unacceptable variation and defining the issue of managing quality.

The Shewhart’s models of quality control in different fields, including the business world and defence industry. He authored many quality control books such as Economic Control of Quality of Manufactured Product among others.

Another key contributor to quality control is concept is Deming who developed sampling techniques borrowing a lot from Shewhart. Deming quality control techniques were highly accepted due to augmented quality, especially in large-scale production. The techniques by Deming are based on augmenting production by minimizing uncertainty and variability during decision-making processes.

According to Deming, variations, and poor management contribute immensely to poor quality in production (Aole & Gorantiwar 2013). As such, he made suggestions to the effect that worker/management relationship and interaction should be improved for optimal quality production. Further, Deming linked augmented quality production to business competitiveness. He came up with 14 points, which became a basis for quality management techniques (Aole & Gorantiwar 2013).

Deming’s proposal to a new thinking that emphasized the improving of quality in manufacturing highly adopted statistical quality control methods. He taught many manufacturers in different countries, especially in Japan. The Deming’s quality control techniques revolutionised production in Japan prompting the Japanese government to introduce an award with his name to recognize business entities that adhered to quality production and quality improvement (Aole & Gorantiwar 2013).

Moreover, Deming propagated the use of Shewart’s Learning and Improvement Cycle.

Other COQ pioneers of the 1930s include Miner and Crocket whose contributions were minor but crucial in quality management (Sower et al. 2007).

The Deming’s work influenced some Japanese and, consequently, some quality experts emerged in Japan. Some of the prominent Japanese that made key developments on the COQ concept include Ishikawa, Taguchi, and Shigeo Shingo (Aole & Gorantiwar 2013). Shigeo Shingo’s contributions are vital even in the current manufacturing sector. Shingo’s techniques are directed to reducing costs while improving quality. A majority of modern manufacturing firms that have adopted Shingo’s model have realised substantial profits due to minimizing of costs (Aole & Gorantiwar 2013).

Formalization of the COQ concept from the 1950s

Quality experts such as Joseph Juran first formalised the COQ concept from the 1950s (Fons 2012). In addition, the formalization of the Prevention-Appraisal-Failure concept from Armand Feigenbaum model was first published.

Juran made vital contributions to the COQ concept. He defined the quality cost as the cost incurred by a firm in its endeavors to improve quality, especially in meeting customers’ quality requirements (Fons 2012). He founded a quality consultancy business, whose principles had global recognition. In addition, Juran authored many books that outlined detailed mechanism pertinent to the COQ concept. Some of the most outstanding provisions by Juran include providing the need for improvement, specificity, organization, problem cause diagnosis, and providing the most appropriate remedies to problems. Juran had three approaches to the COQ concept, including quality planning, quality control and quality improvement (Snieska et al. 2013).

Juran had significant contribution in the PAF model. The model is vital in the COQ concept, especially in the classification of costs. PAF model is used globally due to its relatively comprehensive and precise nature. Feigenbaum and Juran propagated the PAF model in their works from the early 1950s. Nonetheless, the PAF model of classification by some modern quality gurus for some of its shortcoming, including the incapacity to incorporate all types of costs in COQ (Snieska et al. 2013). The original model, for instance, did not incorporate hidden failure costs. In addition, the original PAF model of costs classification did not comprehensively evaluate all elements of poor quality costs (Snieska et al. 2013).

Juran espoused the Pareto Principle and was of the view that quality in not free and, therefore, firms have to incur costs in attaining quality. His work was recognised globally with Japan awarding him for his role in quality control management and in rekindling the US-Japanese cooperation. His work emphasized the concept of quality circles due to their ability to improve interdepartmental communication, especially management and labour.

Moreover, the Juran’s approaches to the COQ concept endorsed the use of statistical and scientific process control. The law of diminishing returns, according to Juran, affects COQ and, as such, quality will optimize at a certain level beyond which conformance will be more costly relative to the returns.

Other key developments in the COQ concepts can be attributed to Feigenbaum who devised the concept of Total Quality Management. Many consider his books as the basis of quality management. He published books in 1957 and 1961 that elaborated the concept of COQ and the importance of quality management. He emphasized the technical aspect of quality management highlighting the role of HR and administration in quality management and COQ. Further, Feigenbaum pointed out that quality and cost are a sum, not a difference and, therefore, he made it clear that COQ concept should be considered in all stages of production. His focus was put on three business elements, including the customer, teamwork, and progressive quality improvement.

Another important expert in the COQ concept is Crosby, who came up with a model that necessitates the doing of things right in the first time (Vaxevanidis et al. 2009). The Crosby’s work, therefore, portrays COQ as costs of correcting reworking to cater for failures (Vaxevanidis et al. 2009).

In the 1970s, Ross came up with an alternative approach to COQ when he developed the Process Cost Model. The Process Cost Model stresses the processes of production as opposed to products/services.

In the 1980s and the 1990s, COQ approaches were slight adjustments to the 1950s model. Some of the models in this era include a method based on a team approach, and the collecting quality cost (Schiffauerova & Thomson 2006).

The ISO and the COQ concept

The international Organizational for Standardization has played vital roles in quality management processes. The ISO has quality requirements that highly inform quality management decisions and approaches to the COQ concepts. The agency emphasizes quality elements such as customer focus, leadership, stakeholder involvement among others.

The Six Sigma and the COQ concept

The Six Sigma philosophy has revolutionised management and quality control from the traditional COQ concepts approaches (Jourabchi et al. 2015). The traditional COQ approaches cannot comprehensively deal with elements in the modern competitive market. Businesses, therefore, invest adopt the six sigma model to augment output quality while retaining competitive pricing. The Six Sigma approaches are vital in contributing to quality improvement, especially in waste minimization, reducing time-related costs, reducing defects and variation while working at the least COQ possible (Jourabchi et al. 2015). The Six Sigma philosophy incorporates doing things right for the first time, augmenting quality in production, and reducing defects to zero.

Businesses that adopt proper sigma significantly reduce prevention and appraisal costs. Some costs such as appraisal and prevention costs can never be eliminated from business operations and, therefore, COQ are part of businesses. With the Six Sigma philosophy, however, some costs such as failure costs can be eliminated or reduced to zero.

The lean philosophy is another key approach in the modern perspectives on the COQ concept. The lean philosophy emphasizes the elimination of waste, which incorporates waste emanating from COQ elements such as product/services failures (Crandall & Julien 2010).

The Cost of Quality is as relevant today as it has ever been

Currently, the business world is highly competitive (Snieska et al. 2013). In addition, globalization has drastically changed markets making it more possible for customers to get products/services from wider ranges of suppliers. Subsequently, customers’ expectations have drastically improved with customers expecting high-quality products/services at the lowest prices. This leaves businesses with the option of producing high-quality products and services at the lowest cost to sell at competitive prices.

As discussed in the literature review, numerous costs come with quality. Doing things the wrong way and, consequently, compromising the quality of products and services can have adverse effects on a business. On the other hand, the course of doing things the right way is associated with extra cost. Therefore, the relevance of COQ in all types of businesses is apparent.

The relevance of COQ in the past years is as evident as it is today. In order to improve quality, some organizations adopted COQ models. As such, organizations have, throughout history, taken into account cost emanating from achieving quality at lowest cost.

Knowing the quality of cost in today world of business is critical in, especially in informing decision-making processes (Bangert 2012). The number of organizations adopting COQ is steadily increasing with about 33% of business firms systematically tracking their quality-related costs (Bangert 2012). This is an indication that more businesses are appreciating the relevance of the COQ concept.

A key element of COQ that has gained relevance in the current business world is the COQ reporting. According to studies, COQ reporting is relevant and beneficial in today’s competitive, quality oriented, and market-focused business environment. The reporting is critical at corporate and operational levels.

Studies have inexorably linked quality to profitability and success of business. Over the last five or so decades, since the formalization of the COQ concept, augmented and improved quality methods have made many businesses realize great success and improved quality of products and services.

The relevance of COQ, however, was limited to certain industries. Currently, the relevance of the COQ concepts has gained popularity among different types of business including but not limited to manufacturing and services. Companies that strictly adhere to marketability/quality techniques and prerequisites are more likely to be successful. It is, therefore, prudent for businesses to embrace the COQ concept. Successful businesses today strive to strike balances between COQ and competitiveness/profitability.

Although the significance of quality in success and achieving competitive advantages of any business is apparent and critical, the cost of quality concept is insufficiently appreciated by many organizations, especially due to organizations’ inability to track their COQs. Many firms, especially small-scale firms, do not have the capacity to track their COQs and, therefore, they incur more losses (Crandall & Julien 2010). As such, the relevance of the COQ can be said to be imprecise since it is difficult to establish how pertinent COQ in some businesses today. The impreciseness of the significance of the COQ concept makes it difficult to compute its pertinence, especially when majorities of modern organizations do not adopt formalised quality costing techniques (Schiffauerova & Thomson 2006).

Research has revealed that the traditional COQ and COPQ models adopted by some organizations do not comprehensively address the impact of quality improvement endeavors. Therefore, the relevance of the COQ concept may not be fully appreciated due to their inadequacies in dealing with costs associated with quality. Consequently, more comprehensive and robust model for describing the COQ implications in quality-based structures should be adopted (Vaxevanidis et al. 2009).

Decisively the COQ concept has strong relevance from its inception to the current global business environments. The high levels of competition, small profit margins, and high expectations from customers and other stakeholders have made business management to put the return on quality investment under high scrutiny. More and more businesses are adopting COQ techniques in the current business world. On the other hand, the relevance of the COQ today is less as ostensibly apparent as in the past. Some experts argue that the modern emphasis on COQ is not as sufficient as it should be and, therefore, improvement should be made on the current models to improve their relevance.

References

Aole, R… & Gorantiwar, V. S., 2013. Quality Gurus: Philosophy and Teachings. International Journal of Research in Aeronautical and Mechanical Engineering, 1(8), pp. 46-52.

Bangert, M., 2012. The Cost of Quality. Quality, pp. 34-37.

Crandall, R. E. & Julien, O., 2010. Measuring the Cost of Quality. Industrial Management, 52(4), p. 14.

Fons, L. A. S., 2012. Integration of Quality Cost and Accounting Practices. The TQM Journal, 24(4), pp. 338-351.

Giakatis, G., Enkawa, T. & Washitani, K., 2010. Hidden Quality Costs and the Distinction between Quality Cost and Quality Loss. Total Quality Management, 12(2), pp. 179-190.

Jourabchi, S. M., Arabian, T., Leman, Z. & Ismail, Y. B., 2015. Contribution of Lean and Six Sigma to Effective Cost of Quality Management. International Journal of Productivity and Quality Management , 14(2).

Rasamanie, M. & Kanapathy, K., 2011. The Implementation of Cost of Quality (COQ) Reporting System in Malaysian Manufacturing Companies : Difficulties Encountered and Benefits Acquired. International Journal of Business and Social Science, 2(6), pp. 243-247.

Schiffauerova, A. & Thomson, V., 2006. Managing Cost of Quality: Insight into Industry Practice. The TQM Magazine, pp. 1-10.

Snieska, V., Daunoriene, A. & Zekeviciene, A., 2013. Hidden Costs in the Evaluation of Quality Failure Costs. Engineering Economics, 24(3), pp. 176-186.

Sower, V. E., Quarles, R. & Broussard, E., 2007. Cost of Quality Usage and its Relationship to Quality System Maturity. International Journal of Quality & Reliability Management, 24(2), pp. 121-140.

Vaxevanidis, N., Petropoulos, G., Avakumovic, J. & Mourlas, A., 2009. Cost Of Quality Models And Their Implementation. International Journal of Quality Research, 3(1), pp. 27-36.