Introduction

This essay will look at the financial aspects of running a speciality cookie business. We will look at how product costing methodologies and supply variations affect business decisions. In addition, we will conduct a cost analysis and evaluate the data to identify the effectiveness and performance of manufacturing.

Establishing BeeDoughs Cookies

BeeDoughs Cookies will be a two-person enterprise in Tampa, Florida’s Seminole Heights neighbourhood. Seminole Heights is a burgeoning area recognized for its diverse business options and food-centric culture. Therefore, it will concentrate on sugar cookies with fruit and herb-infused frostings, such as lemon or thyme, and orange or rosemary, concentrating on sweet and savoury goods. While we only create one type of cookie, sugar cookies, we know how to make them perfectly. We also provide a selection of flavours for our fantastic sugar cookies. Beedoughs caters to the weird, experimental food that throngs to the Seminole Heights neighbourhood, as the name implies. We shall endeavour to create delectable yet unexpected flavour combinations under the tagline “Unconventional delicacies for the quirky” (Agarwal, 2022). We welcome everyone, especially those passionate about food and wish to treat their taste buds to unique delicacies rarely seen on supermarket shelves.

We also feel that success is sweetest when shared with others, so we will provide our consumers with the chance to join in our “doughnut” pay-it-forward initiative. This initiative allows customers to choose to buy a cookie for someone else such as a teacher, first responder, or homeless person. In addition, we will contribute 100 cookies to a local non-profit shelter for every 1,000 cookies sold. The manufacturing and distribution of a product, like any other business, involves various monetary variables. While we cannot control raw material prices, we can browse around for the best deal and alter vendors to keep our manufacturing costs as low as feasible. Keeping our costs low allows us to continue in business, pay our employees, and provide the best possible service to the community.

Costing and Sales Data

Job Order Costing

Running a business and keeping successful while staying faithful to the company’s objective requires a lot of thought. One thing we have control over is the money we pay our employees. We recognize that happy employees are more productive employees. As a result, we will take all necessary steps to ensure that the workplace is as stress-free and pleasurable as possible. In addition, we will pay our staff a reasonable $15 per hour wage based on a 20-hour workweek. We think that the investments we make in our people will pay off handsomely.

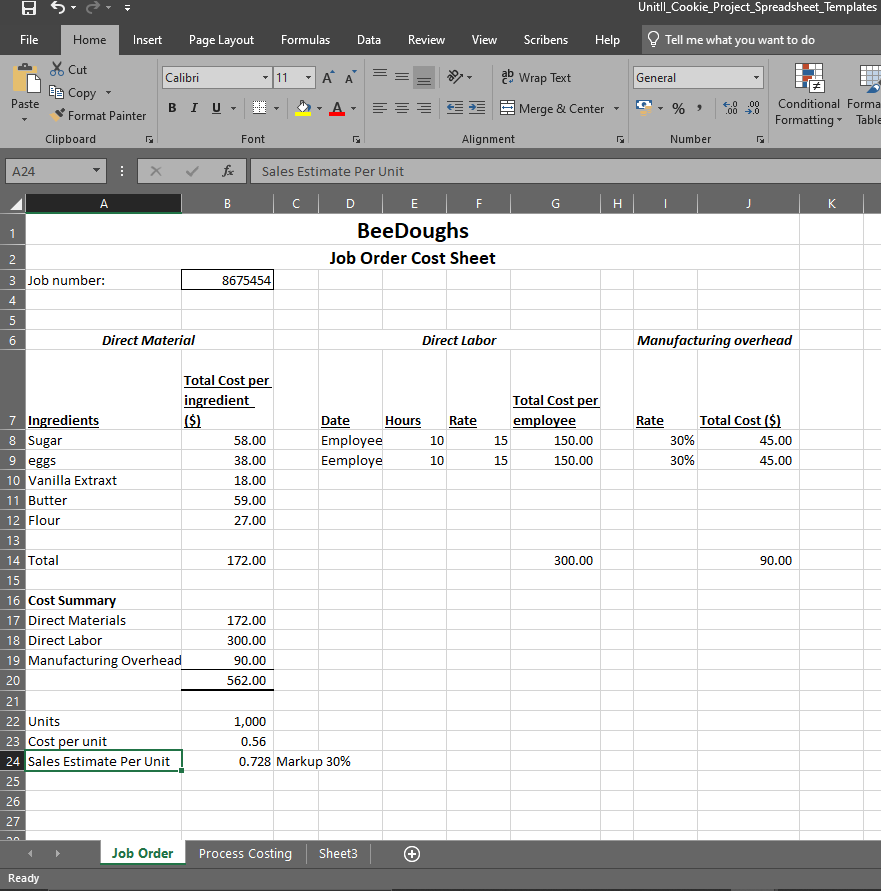

There is a lot more to price than just labour. Making 1,000 cookies involves multiple processes, but we’ll focus on the three most important ones. The first phase is to gather all of the components, which determines the cost of raw materials; the second step is to bake the cookies, which takes into consideration labour hours and the consumption of utilities; and the third step, of course, is to sell the cookies. We constructed a basic job order costing evaluation by adapting a dish from globe chef Alton Brown, changing it to reflect a much larger quantity of 1,000 cookies, and investigating the typical bulk pricing for each essential component (Martin, 2021). As a result, we have calculated that each cookie will cost around $0.56 to make. We propose to sell our cookie for $2.00 each piece, a profit of $0.73 per unit.

Process Costing

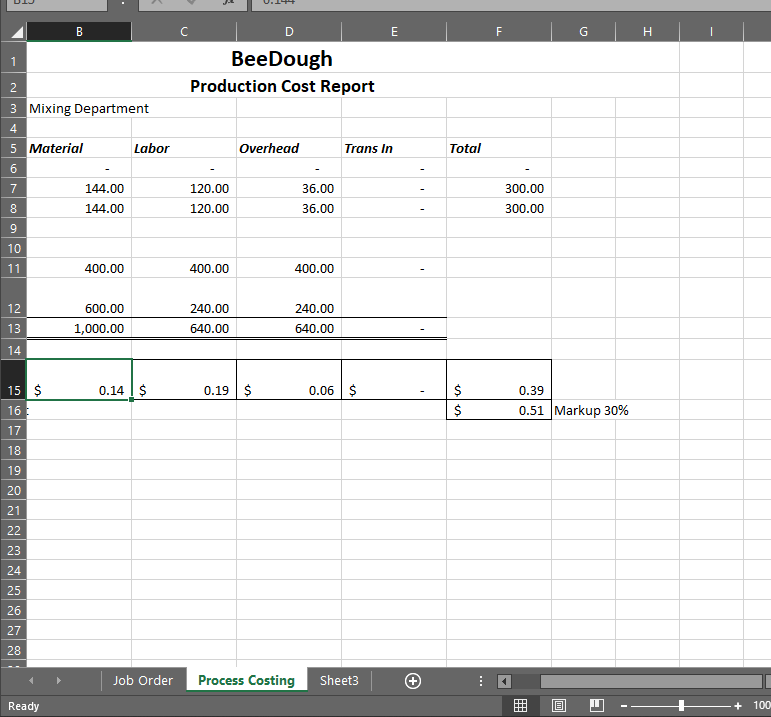

Assume that this is merely the first part of the manufacturing process. As a result, there is no “transfer in” (no items in stock), and the two days considered are the first days of the mixing department. Two teams are focused on completing 1000 blueberry cookie units. They completed 40% of the work of the entire process in two days (the mixing phase occupied 40% of the overall process in two days, which included mixing, add-in, and packaging), and 40% of the final project of the mixing section would be transferred to the add-in department. In the mixing process, just three components are used: flour, eggs, sugar, and milk. The result of the mixing step is shown in the process costing table below:

The cost per cookie computed by job order costing is her than that obtained by process costing, based on the estimations of two costing approaches above. The cost and selling price, based on 30% markup, per cookie by job order costing technique are approximately$0.56 and $0.73, respectively, whereas the cost and selling price per cookie by process costing are around $0.39 and $0.51. As a result, job order costing is more expensive than process costing, making the customer’s choice to purchase the product more difficult.

Compare and Contrast Costing Methods

Job Order Costing

Job order costing considers all components that make a product, including raw materials and labour. A price point can be determined by estimating the exact monetary spending required to create a particular item. Because the cost of production for each item or service might vary depending on the required materials and labour, job order costing works effectively for organizations that custom build goods such as landscapers or painters.

Process Costing

In process costing, direct material costs are often included at the beginning of the process, while all other expenses, both direct labor and overhead, are gradually added throughout the duration of the manufacturing process. In a food processing procedure, for example, the direct material, such as a cow, is introduced first, and then subsequent rendering activities gradually turn the direct material into final goods such as steaks.

On the other hand, process costing determines the spending in creating a set of things rather than an individual item. When things are mass-produced, determining each unit’s actual production cost can be challenging. The total quantity of materials and labour required to make an entire batch of something is calculated using a process costing. Take, for example, the BeeDoughs job order cost sheet from earlier. We can establish the cost of each cookie by calculating the total cost of the supplies and labour required to bake 1,000 cookies, irrespective of how much the ingredients for the first batch of 250 cookies cost more or less than the remaining 750.

Impact of Increase and Decrease in Sales

Sales will naturally fluctuate on a daily, weekly, monthly, and even annual basis. These changes in sales, whether positive or negative, will have an impact on the profit margin and may demand end-product pricing modifications. For example, if the price of butter rises dramatically, our cookie production expenses will rise as well. If there is a significant rise, we may need to raise the price of our cookies to make a profit.

This new pricing scheme might lead to fewer sales and, as a result, a loss of earnings. If this is the case, steps must be made to safeguard the business’s long-term viability. Finding lower-quality components to keep production costs down might be a good idea. However, decreasing the ingredient criteria might result in a less acceptable product, resulting in fewer sales.

Increased sales, on the other hand, will need the purchase of extra ingredients. Increasing our purchasing volume may provide us with additional negotiating power with our vendors. This would result in a twofold enrichment, with decreased manufacturing costs but no increase in sales price. This rise in revenues would be quite beneficial.

Conclusions and Recommendations

Even with such a simple example of costing and possible sales situations, it is clear that BeeDoughs has enormous potential for success. Still, it is also a hazardous business strategy. While the price of ingredients for cooking can fluctuate, it rarely does so dramatically. This scenario makes estimating long-term expenditures and budgeting more straightforward. BeeDoughs must give a high-quality product to every consumer, every transaction, for this business to succeed. As a result, sacrificing superior ingredients for a small revenue gain is not recommended. BeeDoughs should focus on creating a great, one-of-a-kind epicurean experience to secure return customers and success.

References

Agarwal, A. K. (2022). Establishing a Business in India. In Doing Business in India (pp. 167-183). Springer, Singapore.

Martin, L. (2021). Establishing Local Business Units. In International Business Development (pp. 155-175). Springer Gabler, Wiesbaden.