Introduction

Changes in prices of goods and services are triggered by shifts in demand and supply. In other words, prices of goods are determined by the interaction between supply and demand. Market equilibrium occurs when buyers purchase exact amounts of goods sellers are willing to sell (Welch & Welch 2009). Additionally, change in demand is brought about by non-price factors while change in quantity demanded is as a result of alterations in prices of goods. This paper explains market equilibrium and the difference between change in demand and change in quantity demanded.

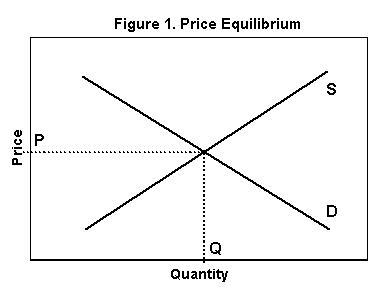

Market equilibrium

Graphically, market equilibrium is arrived at when the supply and demand curves are combined. The point at which the two curves intersect is referred to as market equilibrium (Welch & Welch 2009). Therefore, quantity demanded matches quantity supplied at market equilibrium. Furthermore, the agreed price of a good between buyer and sellers is known as equilibrium price and corresponding quantity is equilibrium quantity. Points of disequilibrium occur when supply and demand are out of balance (Berry, Levinsohn & Pakes 2005). In the figure below, P and Q denote equilibrium price and equilibrium quantity respectively.

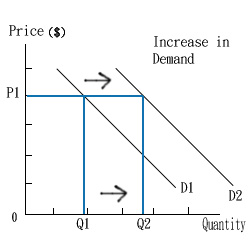

Change in Demand

When the entire purchase plan is adjusted, a change in demand occurs (Welch & Welch 2009). These are the changes resulting from non-price factors. A demand curve either shifts to the right or left when there is a change in demand as shown by the figure below.

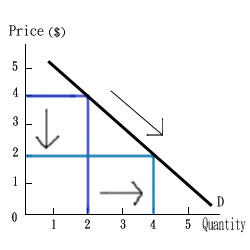

Change in the quantity demanded

Change in quantity demanded is said to take place when shifts in demand are dictated by alterations in the price of a good (Welch & Welch 2009). The demand curve does not shift, but movements are observed along it. The figure below illustrates these movements.

Conclusion

Welch and Welch (2009, p. 91) state that plans of sellers and buyers are satisfied at an equilibrium price. A surplus occurs when the price of a product is above equilibrium. On the other hand, a shortage occurs when the price is below equilibrium (Welch & Welch 2009). Nonetheless, forces of demand and supply bring the prices back to the equilibrium point. Therefore, for obvious reasons, market equilibrium and changes in demand and quantity demanded shape the prices of goods and services.

Reference List

Beranek, M 2001, How demand and supply determine market price, image, Web.

Berry, S, Levinsohn, J & Pakes, L 1995, ‘Automobile prices in market equilibrium’, Econometrica, vol. 63, no. 4, pp. 841-89, Web.

Tripod, n.d., A graph illustrating increase and decrease in demand, image, Web.

Tripod, n.d., Change in the quantity demanded, image, Web.

Welch, P J & Welch, G F 2009, Economics: Theory and practice, John Wiley & Sons, New York.