A Brief Company Background

WHSmith is a British retailing company operating a chain of shops in the UK. However, the company also has operations in India, the Middle East, Australia, and South-East Asia (MarketLine 2014). WHSmith operations are divided into two business segments. The two are travel and high street. The company’s high street stores are located throughout the UK, situated in significant cities streets. The stores sell entertainment products, and news and impulse products such as confectionery, newspapers and magazines. Books and stationery such as greeting cards are also offered (MarketLine 2014). As of 31 August 2013, the company operated 15 high street stores, totalling to three million square feet (MarketLine 2014).

The travel business segment on the other hand focuses operating stores on railway stations, airports, workplaces and hospitals (MarketLine 2014). The stores are also operated in bus stations, and motorway service areas. The travel business segment stores are also mainly in the UK, coupled with the other foreign markets mentioned. As of 31 August 203, travel stores total area of selling space equalled 0.5 million square feet (MarketLine 2014).

The company is headquartered at Swindon Wiltshire, and is listed in the London Stock Exchange under FTSE 250 Index (WHSmith Plc 2013). WHSmith is credited with being the first to operate a chain store, as well as for the development of the ISBN catalogue system. According to MarketLine (2014), the company revenues for the financial year ended August 2013 were £118.6 million. The revenues had recorded a decline of 4.6%, in comparison to the previous year 2012. The company’s operating profit was £107 million for the financial year ended August 2013 (MarketLine 2014). The operating profits had recorded an increase of 8.8%, as compared to the previous year 2012.

WHSmith’s Capital Structure

WHSmith is a publicly traded company. It is financed through debt and equity. Its capital structure is made clear in the comprehensive balance sheet. The firm’s complete balance sheet as of August 2013 is shown in appendix 1. The group’s comprehensive balance sheet indicates that the primary source of financing is derived from common shares. In addition, WHSmith has ten corporations acting as shareholders. The individual corporations hold more than 3% of the issued share capital (Equities 2014). Together, these organisations own approximately 60% of the total shares in this company. The biggest shareholder controls 9.86% of the company. The figure is within the disclosure range specified by the government in the UK. The company’s debt to total capital ratio is 28.26% (WHSmith Plc 2013).

Industry Overview

The company operates in the stationery industry. WHSmith is one of the firms leading in this sector. It concentrates primarily on impulse products. Such products include books, magazines, and newspapers. The local and international industry is becoming very competitive. However, WHSmith has an edge over its competitors. The situation is made apparent by the awards won by the business. For instance, in 2009, the company won General Retailer of the Year and the Bookselling Company of the Year awards (WHSmith Plc 2013).

The growth of internet is a force to reckon with in the industry. EBooks and online shopping are becoming the norm. To counter these forces, WHSmith has launched eBooks and an online transaction platform. However, these channels are not performing well compared to the physical stores (WHSmith Plc 2013). As a result, the firm is prompted to change its sales strategy. The aim is to come up with an effective internet marketing model. The management has noted that Amazon.co.uk and other organisations have successfully doubled their market share through online sales of books in the recent past (MarketLine 2014).

WHSmith is also threatened to some extent by dedicated stationery stores. In addition, specialist card shops are competing with the company in this sector. However, in overall, the company is doing well as evidenced by its consistent expansion into international markets.

WHSmith: Company Valuation

Methodologies used in Business Valuation: Overview

Basically, there are four fundamental methods of valuing business or any other professional practice. The strategies include assets approach, market approach, discounted cash flows, and income approach (West & Jones1999). Each of these approaches utilises a variation of available methods in the valuation of the business enterprise. In addition, each of them makes use of specific procedures in the calculation of business value. Some of the commonly used techniques include discounted cash flow analysis (DCF) and multiples method. Other techniques include market valuation and comparable transactions method (West & Jones 1999).

Comparable worth methods

It is another approach used in valuing a business. Under these methods, a comparative analysis is carried out between the organisation and other similar entities. In most cases, public organisations that are found within the same sector are reviewed. The companies offer similar products to the same clients.

An assumption is made with regards to potential buyers. The method assumes that potential buyers would not pay a greater amount for the business, than they would pay for a similar company trading publicly (Ross, Westerfield & Jaffee 2005).

Greater caution is encouraged while selecting for the publicly held company chosen for comparison. The company chosen for comparison should be similar to the business under review. For instance, the organisations may be dealing with the same supplier. In addition, they may be found within the same locality.

Asset valuation method

The approach is also popular. The worth of most conventional business organisations is tied to the fixed assets held by the firm. In light of this, valuation can take into consideration these assets (West & Jones 1999). Again, an assumption here is made in relation to the buyer. It is assumed that the buyer will compare the organisation with a similar one before making their decision to purchase. They will go for the assets that are worth their money.

With the assumption in mind, substitute assets are then valued based on cost of reproduction [cost of constructing substitute assets, using same material as original, under current prices] (Fernandez 2002). Valuation of assets can also be tied to the expenses incurred during replacement. The expenses involve those associated with the replacement of the original assets at current prices.

The financial performance methods

Financial performance methods are commonly used to value a business for the purposes of succession planning. The methods entail sets of procedures, for measuring a company’s financial performance. The methods usually attempt to measure the historical and future performances (West & Jones 1999). The methods are also essential the exit strategy with higher probability is sale of the business. Long term gifting programs however do not usually prefer these methods.

Net present value analysis (NPV)

NPV is the most commonly used method of financial performance, especially in pre-acquisition valuation (Reddy et al. 2013). NPV in general constitutes a capital-budgeting model. The model compares the present value of proposed transaction’s benefits, with the present value of related costs (Reddy, Agrawal & Nangia 2013).

According to West and Jones (1999), if NPV is positive, then it follows that costs of the deal are exceeded by the benefits. Consequently in case of buying, decision to go forward would result to increased value for the buyer. In addition, the shareholder’s wealth would be increased in the process.

Net asset valuation

Bryan (2003) provides a conceptual definition of net asset value. Bryan (2003) refers to it as the total amount by which the total assets exceed the total liabilities. The valuation model is usually used to assess the profitability, solvency, and creditworthiness of an enterprise. In situations where the liabilities exceed the assets, the net asset value is negative. Consequently, the firm should be regarded as insolvent. On the other hand, net asset value is positive if the assets exceed liabilities.

According to Copeland, Koller and Murrin (2000), the net asset value represents the value of assets available to the ordinary shareholders. The value is determined after debts of concern, preference capital, and loan capital are deducted. Possible rights and obligations in relation to preference shareholders or loan stock are also deducted or accounted for. Net asset value per share is arrived at by dividing the value of net assets with total number of ordinary shares in an issue.

Valuing WHSmith Based on the Discounted Cash Flows Method

Discounted cash flows analysis valuation method is very accurate in estimating the value of a business based on the earning potential. According to Kaplan and Ruback (1995), the method determines the value of a business through discounting future business earnings. The discount rate is important to the business. It is used to highlight the risks faced by the entity. Three inputs are very critical in valuing a business using the discounted cash flows method (Fernandez 2002). The inputs include business net cash flow forecast, covering a pre-determined future period.

According to Ross, Westerfield & Jaffee (2005), the discounted cash flow method tries to establish the value of a company today on the basis of projections of expected returns. Basically, the approach assumes that entity is worth the cash it is capable of availing to investors in times to come. Several approaches of valuing a company using DFC are available including the cash flow to firm approach, and dividend discount model and free cash flow to equity (Damodaran 1994). Valuation of WHSmith in this case is based on the free cash flow to equity approach.

The Forecast Period and Forecasting Revenue Growth

Forecast period

The first step in valuing a business using DFC entails determination of the duration, upon which the cash flows are projected into the future (Fernandez 2002). The cash flows for WH Smith Plc will be reviewed over a period of 60 months. WH Smith is apparently a solid company, operating with several market advantages. For instance, the company enjoys strong market channels (Fernandez 2004).

It is also assumed that the company will endeavour to address the demands of its customers. What this means is that the entity will be occupied for the entire period. However, we should also assume that WH Smith plc will face stiffer competition after the five years. The market can be further expected to have more competitors after the five years. Some of the figures used in the study are derived from WH Smith plc financial statements year ended September 2013. See Appendix I for WHSmith’s financial statements.

Revenue growth rate determination

According to Ross et al. (2005), arriving at the revenue growth rate figure is based on a procedure for forecasting revenue growth over the projected duration (5 years). The figure is determined by breaking down three different functions. The first involves projected capital expenditure. The second is the operating profits after tax. The last is the capital required to support the operations of the business. The company’s revenues for 2012 and 2013 were £1243 and £1186 million respectively (WHSmith Plc 2013). The figures represent a 5% change in those two years. It is expected that the demand for the company’s products will remain constant and the revenues will grow at a rate of 5% in subsequent years.

Despite the assumption, it is essential to downplay the revenue growth expectations of WHSmith plc. The company may record a strong growth in revenue in the next number of years. However, other market conditions may affect this growth negatively as the company proceeds through the 60 months period. Market environment factors might include increased competition, or even higher costs of production. Considering this factor we should be more conservative in valuing WHSmith plc. We thus assume that the company’s revenues will continue to grow by 5% for the first two years. The percentage will drop to 4% for the next 2 years, and then 3% for the final year.

The latest annual reports of WHSmith plc indicate revenues worth £1186 million. The revenues can be forecasted as shown below:

Table: 1 Optimistic and realistic revenue growth rates for WHSmith Plc.

Forecasting WHSmith Plc Free Cash Flows

The next step in valuing WHSmith Plc using DFC is estimating the free cash flows of the organisation, for the forecast period. Free cash flows refer to the cash flowing within an organisation, in the course of a year or less, after deduction of all expenses (Ross et al. 2005). Hence free cash flow should be the actual amount left from operations. Free cash flows are calculated from analysing the remainder of revenues, following deduction of operating costs and working capital requirements. In addition, net investments, and taxes are also deducted in order to determine free cash flows (Fernandez 2004). Fernandez (2004), further postulates that amortisation and fall in value are not deducted. The reason is that the two are non-cash expenses.

Future operating costs are an essential element in the determination of free cash flows for any one given company. However, the function should be tied to current operating expenditure. Forecasting of operating costs, on the other hand, relies on the operating costs margin of the company, in this case WHSmith Plc (Damodaran 1994). WHSmith plc operating costs for 2013 are £ 1099 (WHSmith 2013).

According to Damodaran (1994),

Operating Costs= Total revenues-Earnings before Interest and Taxation/Net

Operating Profits.

Analysing the operating costs as part of the income generated gives the operating margin, essential in forecasting of operating costs. Consequently, the operating margin of WHSmith plc for the year 2013 is 93%;

(1099/1186)*100=92.6%= 93%

What this implies is that for every unit of revenues, WHSmith Plc uses 0.93 units of operating expenses. However, in order to arrive at a more realistic value of the company, possibility of more companies in the same industry being built must be considered.

It is assumed that operating costs are increasing. The reason is that the company is made to lower prices in order to beat competition. The competitiveness is for the long term. As such, it is assumed that the operating costs remain at the 85% mark over the first two years. However, the operating margins increase to 93% by the fourth and fifth years. See table 2 for more results. Public limited companies usually pay taxes on their operating profits. However, the amount paid may not reflect the official rate. Consequently, the assumption in this case is that the company has been paying tax at a rate of 30% in the last two years. It is also assumed that the organisation will continue to remit similar payments over the envisaged period.

Forecasting of the free cash flows also considers net investment of a company (Kaplan & Ruback 1995). Businesses usually invest in capital items in order to facilitate their growth. According to Kaplan & Ruback (1995), net investment value is calculated by subtracting non-cash depreciation charges from capital expenditure. WHSmith incurred £230m in the last year as capital expenditures. It reported a depreciation of £73m (WHSmith Plc 2013). Hence, the company had net investment of £157 million, translating to 13% of the total revenues. Let’s make an assumption that the net investment for the last 24 months was 15% of the income generated.

Another assumption can also be made that since competition can be expected to increase in the industry, capital investment will have to be boosted to remain competitive. It is taken that the net investment will return to the 15% mark by end of the 60 months. The rate can be distributed over the five years as 13%, 13%, 14 %, 14%, and 15 % consecutively over the projected duration.

Table 2: Forecasting WHSmith Plc operating functions.

Working capital is defined as the cash a business needs in the running of the day to day operations (Kaplan & Ruback 1995). The working capital can thus be also referred to as the short-term financing, necessary for the maintenance of the current assets for instance inventory. According to Bryan (2003), working capital is calculated by deducting the current liabilities from the current assets. In its annual report, WHSmith Plc (2013) indicates current assets £233 million, while the current liabilities were £212 million. The net working capital for the entity is expected to be £21 million (WHSmith Plc 2013).

According to Bryan (2003), sales revenues grow simultaneously with the working capital. What this means is that more inventories and receivables are needed to complement growth. In WHSmith plc case, let’s assume the changes in the working capital occur proportionally to revenue growth. For instance, if the revenue grows by 10%, then the working capital grows as the same rate.

Table 3: Free cash flows forecast calculation for WHSmith.

The computations above have provided the free cash flows for the projected five years. A discount rate is required to determine the net present value of cash flow. According to Copeland, Koller, and Murrin (2000), an essential strategy in this case is the weighted average cost of capital (WACC). The function involves the after tax cost of debt. The debt is analysed together with the cost of equity. The two elements are brought together in analysing WACC.

Cost of equity refers to the expenses incurred by the company in maintaining a share price satisfactory to the investors (Copeland et al. 2000). Cost of equity is usually calculated using the Capital Asset Pricing Model (CAPM).

Using CAPM, cost of equity formula is as follows:

Cost of equity (Re) = Rf + Beta (Rm-Rf), where

Rf refers to Risk free rate, which the amount obtained from investments In securities regarded as credit risk free.

(Rm-Rf) equals the equity market risk premium (EMRP). EMRP represents investors expected returns, due to their taking the risk of investing in the stock market (Ross, Westerfield & Jaffee 2005).

Miles and Ezzell (1980) provide a working definition of WACC. Miles and Ezzell (1980) refer to it as the weighted mean of the cost of equity. It is also related to the cost of debt. D/V is another important function. It highlights the amount of debt. It compares the debt held by the company to total value (Miles & Ezzell1980). E/V is also taken into consideration. It indicates the equity of the company. The equity is reviewed against the total value of the entity (Miles & Ezzell 1980).

The formula for WACC is given below.

WACC= Re x E/V + Rd x (1 – corporate tax rate) x D/V (Miles & Ezzell 1980).

The formula for computing WACC for WHSmith is given below.

One may assume that the ratio of the firm’s debt to equity is 4:6 as far as capital formation is concerned. In addition, the tax rate stands at thirty percent. Borrowing rate (Rd) on the debt of the company can be assumed to be 8%. The risk free rate (Rf) can also be 6%, while beta is 1.2. Risk premium adds up to 9%. WACC of WHSmith plc can be calculated as follows:

Cost of debt 0.40[Rd*(1-0.3)]+

0.40*[3.0*0.8]+0.40[3.5]+1.20=3.6 + Cost of Equity. 0.60[Rf+ b(RP)]

0.60 [0.8+1.2(9)]=6.96

WACC=11% rounded

Using a Gordon growth model, the terminal value of WHSmith plc cash flows can be established:

Terminal Values = Final Projected Year Cash Flow* (1+Long term cash flow growth rate)

(Discount rate-long term cash flow growth rate)

(Bryan 2003).

Assuming the WHSmith plc free cash flows grow by 3% annually, then:

Terminal value of WHSmith plc= £57m*1.03/ (11%-3%) = £734 Million.

The value of WHSmith plc can thus be regarded as worth £734 Million.

Valuing WHSmith Using the Dividend Discount Model

According to West and Jones (1999), DDM is a procedure of valuing the stock price of a given business through usage of predicted dividends. The predicted dividends are then discounted back to their present value. DDM method of valuing a business does have several approaches since it does not apply to businesses that do not pay dividends. The major idea behind the model is getting a growth number. A common option involves taking the return on equity (ROE) and then multiplying it with the retention ratio (West & Jones 1999). The retention ratio is equal to 1-payout ratio (West & Jones 1999).

WHSmith is apparently a publicly traded company, exhibiting a steady growth of dividends rates (WHSmith 2013). WHSmith average growth rate of the shares has been 2.0% over the last five years. In determination of share value, investors need to ascertain the present value of the future returns of the same known as intrinsic share value (West & Jones 1999).

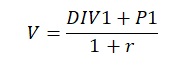

Intrinsic share value is calculated as follows:

Where:

DIV1=Expected dividend in 1 year

P1=Expected share price in 1 year

r=expected rate of return

(Reddy et al. 2013)

Since the average growth rate of WHSmith shares has been 2% for the last few years, the dividends for the next year can be estimated at: £3.

Expected rate of return is based on cost of equity, which is 15%.

Expected share price value in one year can be based on average of previous share price performance which is £294.

Intrinsic share value can be determined as:

The intrinsic share value is regarded a fair value since it compensates the investors with regard to the opportunity cost. In addition, similar companies share prices are in the same range. For instance Tesco Plc, a major competitor with WHSmith has shares valued at £278. Based on the intrinsic share value, WHSmith market capitalisation can be determined through the shares the company has on offer. WH Smith had 602 054 shares on offer as of the year ended August 2013 (WHSmith Plc 2013).Hence WHSmith is worth

(£258*602 054 Shares)=£155.3 million

Future Value Maximisation Opportunities

One of the ways through which WHSmith can maximise future value is by splitting travel and high street business segments into individual enterprises. Considering the prevailing trends in the industry, the separation will help the management to focus on profit maximisation of individual entities. To strengthen its position in the market, WHSmith can merge with similar companies or adopt an acquisition strategy in the overseas markets. Such measures would facilitate rapid market penetration.

WHSmith Plc should also implement an effective internet business model. The model should complement the operations of the physical stores. The physical establishments constitute a core aspect of the business. The business conducted by WHSmith Plc cannot entirely rely on an internet model.

Conclusion

The discounted cash flows method is regarded as one of the most accurate approaches in determining the value of business organisations. The method is rigorous and focuses on the critical issues. However, it is noted that the strategy does not eliminate uncertainties with regards to the actual value of the business. In addition, it is very difficult for tow people to get a similar value from the formula.

The dividend discount model on the other hand is relatively simpler. However, the model cannot be regarded as giving the actual value of a business since numerous aspects are left out. Determination of the value of a business should thus be based on numerous methods as possible. Consequently, the average value of the business can be determined.

References

Bryan, K 2003, Handbook of financial modelling for business decisions, Crest Publishing, New Delhi.

Copeland, T, Koller, T & Murrin, L 2000, Valuation: measuring and managing the value of companies, 3rd edn, Wiley, New York.

Damodaran, A 1994, Damodaran on valuation, John Wiley and Sons, New York.

Equities 2014, WH Smith Plc, Web.

Fernandez, P 2002, Valuation methods and shareholder value creation, Academic Press, New York.

Fernandez, P 2004, ‘The value of tax shields is not equal to the present value of tax shields’, Journal of Financial Economics, vol. 73 no. 1, pp. 145-165.

Kaplan, S & Ruback, R 1995, ‘The valuation of cash flow forecasts: an empirical analysis’, Journal of Finance, vol. 50 no. 4, pp. 16-38.

MarketLine 2014, Company profile: WHSmith Plc, Web.

Miles, J & Ezzell, J 1980, ‘The weighted average cost of capital, perfect capital markets and project life: a clarification’, Journal of Financial and Quantitative Analysis, vol. 2, no. 7, pp.19-31.

Reddy, S, Agrawal, R & Nangia, V 2013, ‘Reengineering, crafting and comparing business valuation models – the advisory exemplar’, International Journal of Commerce and Management, vol. 23 no. 3, pp. 216-241.

Ross, S, Westerfield, R & Jaffee, J 2005, Corporate finance, 7th edn, Tata McGraw-Hill, New Delhi.

West, T & Jones, J 1999, Handbook of business valuation, 2nd edn, Wiley, New York, NY.

WHSmith Plc 2013, Annual report and accounts 2013, Web.

Appendix

Appendix 1: WHSmith’s complete balance sheet as of August 2013

Source: Equities (2014).