Introduction

Crude oil is a critical commodity in the modern industrial world. It is one of the most actively traded resources in the global market. The extent and volume of such commerce have their impacts on the international community, forming a reciprocal connection that both regulates and can be affected by economic affairs. The price of oil is sensitive to external influences, rapidly reacting in response. The real price of crude oil is determined through a variety of factors, such as market sentiments, supply and demand, and inflation which is utilized for analytical models to predict further cost fluctuations and a trading strategy.

Oil Trade

Crude oil is one of the most critical commodities for the industry, national development, and economic growth. It impacts the production and price of valuable petroleum products such as gasoline. In the last 25 years, oil trade has been transformed into market structures which allows to better form commercial agreements and provides flexibility for buyers and sellers to achieve their needs. Two types of markets exist, the “spot” market is for near-term delivery. Meanwhile, the “futures” market is a contract regarding the future purchase of crude oil within a specific quantity at a predicted price. The futures market serves two functions, as a financial exchange for major players on the global market, but also a guarantor for any parties interested in protecting their contracts from volatile price fluctuations. The “futures” market helps to determine expectations in terms of supply and demand. The predictions become a physical “real” price at the time that the delivery is made, or the futures contract ends.

The import and export of trade influence the distribution of energy within the international markets, as the social and economic stability of countries, is strongly affected by these patterns. The uneven nature of crude oil production and consumption essentially forms global trade networks. By the 21st century, it has evolved into a complex and integrated system of exchange. Member-states within the oil trade system attempt to ensure the stability and reliability of their import and export networks. Governments are forced to consider the factors of imbalance in crude oil trade such as prices and supply. These may influence production costs, stock prices of businesses, and the welfare of citizens. Therefore, governments seek to predict and understand oil prices and trade patterns before introducing macroeconomic interventions.

Significance of Price Variation

As a critical energy source, oil impacts energy markets and the performance of national economies. According to the research of 1999, a new specific political economy of oil began to develop after the 1970s while making fluctuations in oil prices politicized and actively influencing economics. Since 2002, oil prices have risen exponentially, and then rapidly crashed. Research shows that oil price fluctuation negatively impacts nations. For example, rising prices lead to costlier production, thus causing its reduction as well as decreasing competitiveness. As a consequence, there may be a shortage of certain product output or higher unemployment due to production downturns.

The real economic activity of industrialized OECD countries is most often dependent on oil price fluctuations. It is generally accepted that GDP, CPI, employment rates, stock markets, and economic activity are all statistically impacted by and dynamically intertwined with the real price of crude oil. Furthermore, oil prices also influence the specifics of international trade, and these tendencies were studied in detail in 2000. This is particularly relevant for countries with economies based on raw materials, such as crude oil, in both cases of import and export.

Inflation

The real price of crude oil and inflation has a cause and effect impact on each other. Most commonly, inflation follows the movements of oil prices. A central measurement of inflation, the consumer price index (CPI) varies based on oil price fluctuations. It creates challenges for a monetary and fiscal policy which then must react appropriately to prevent hyperinflation that can further destabilize global oil prices. Research shows that an average increase of 10% in global oil price, can increase domestic inflation by approximate 0.4 percentage points with the impact stabilized after two years. Using monthly CPI values for developed and emerging economies, a 1% increase in oil price leads to a 0.01 percentage point inflation hike. The effect is asymmetric, as positive price shocks produce a bigger impact than negative shocks. Also, much attention should be paid to the role of energy derivatives in influencing the crude oil market in the context of increased inflation rates.

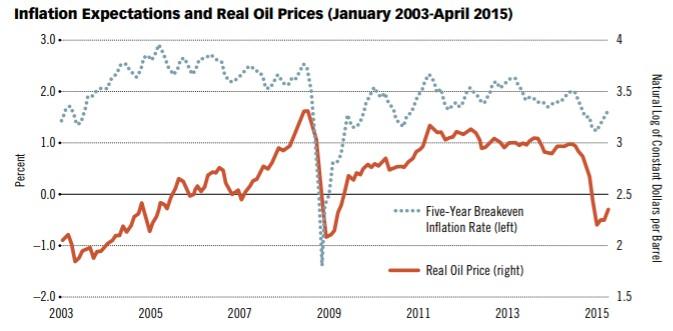

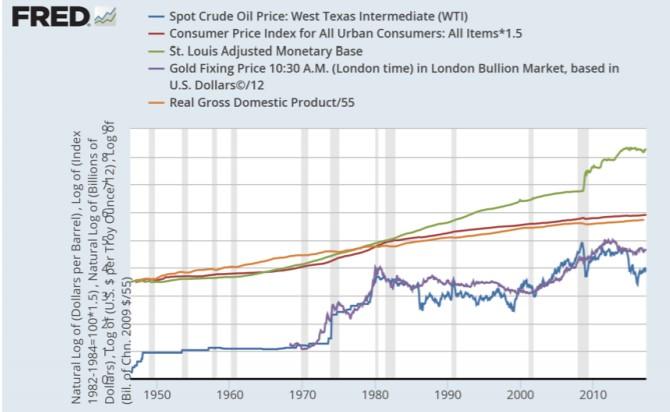

Before the 2008 financial crisis, the direct relationship between oil prices and natural gas prices was observed. Furthermore, inflation rates were not viewed as extremely affecting fluctuations in oil prices. The correlation between inflation and oil price has been more significant in recent years, rather than before 2008. Due to enacted monetary policy and careful financial behavior, inflation expectations are practically synchronized with oil price movements and predictions. In Figure 1, inflation expectations are compared against the log of the real price of crude oil. While before the crisis, increases in prices did not cause a significant change in inflation. Afterward, the movements are in tandem, upwards of a 0.75 similarity as inflation measurements fell from 2.28% to 1.79%.

Supply and Demand

Oil is an extremely elastic commodity, highly dependent on its production and consumption. This forms the supply and demand aspect of the market. The oil demand is almost always high, ranging from collective consumer needs such as gasoline to powering manufacturing processes. Meanwhile, supply is dependent on the production of oil as well as its availability in international reserves. In combination, these factors and economic processes control the real price of oil. Shocks in oil prices indicate sudden changes in the real price of crude oil per barrel. Commonly due to a specific stimulant, the shock can either be demand or supply-based. For example, a major country experiencing decreased economic activity and therefore production capabilities may cause decreased demand which would lower the price of oil. Still, if a major oil supplier experiences a 1% disruption, it may lead to the hike of the oil price by 5 to 10%. However, the size and strength of the economy of the countries in the proposed scenarios matters, as elasticity may vary greatly between emerging and developed economies.

Oil supply is elastic in the medium to long-term impacts since it can easily be constrained in the short run. Supply is determined through production which is driven by exploration and extraction dependent on technology and policy. One of the most critical aspects of supply is the production of oil by countries. Economic unions and intergovernmental organizations often engage in agreements on the production of oil. One of the largest of such oil cartels is known as the Organization of the Petroleum Exporting Countries (OPEC) which consists of 15 nations that control 73% of the global oil reserves.

OPEC can efficiently manipulate oil prices by collectively managing quotas of production and output targets, affecting international supplies. Although other major oil producers such as the United States and Russia are not in OPEC, they often collaborate or compete to manipulate real-time prices and profits. It is important to note that the supply cannot always be controlled. Geopolitical events such as war or natural disasters can lead to disruptions in production or shipping. As investors foresee future supply shortages, the volatility of oil heightens, and prices increase.

Demand conditions are constantly changing due to production capabilities or consumer trends. These can be dependent on economic growth or experience erratic shifts as well. When calculating demand, the primary parameters are global GDP growth, as well as short and long-term elasticity of demand. Demand shocks are sudden, and supply requires time before catching up. Therefore, oil prices may rise by as much as 8%. However, in the long run, the global GDP is depressed by 0.3%.

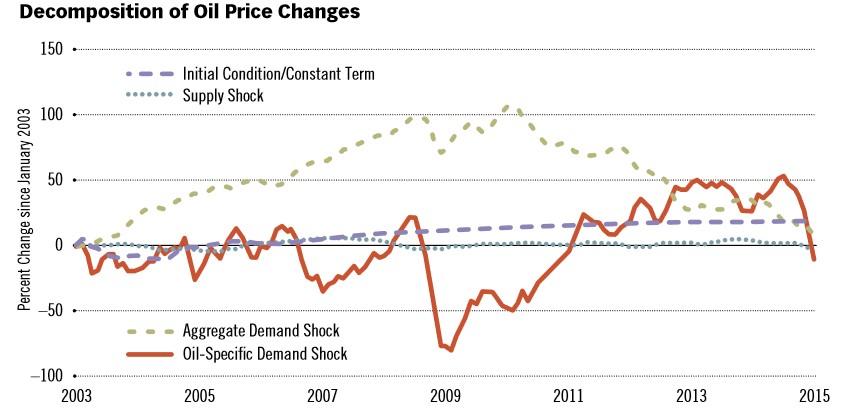

However, changes in oil prices can also be impacted by demand shocks. There are aggregate demand shocks that are interconnected with overall real economic activity without a connection to supplies of crude oil. Sometimes, oil-specific shocks occur which changes in the price of oil without an explanation, often due to precautionary motives. Figure 2 demonstrates the effect of both supply and demand aggregate shocks on the log of global oil prices. While supply remains relatively stable, there is an evident correlation between aggregate demand shocks and oil-specific demand shocks which effectively mimic real oil prices at the time.

Analytical Models

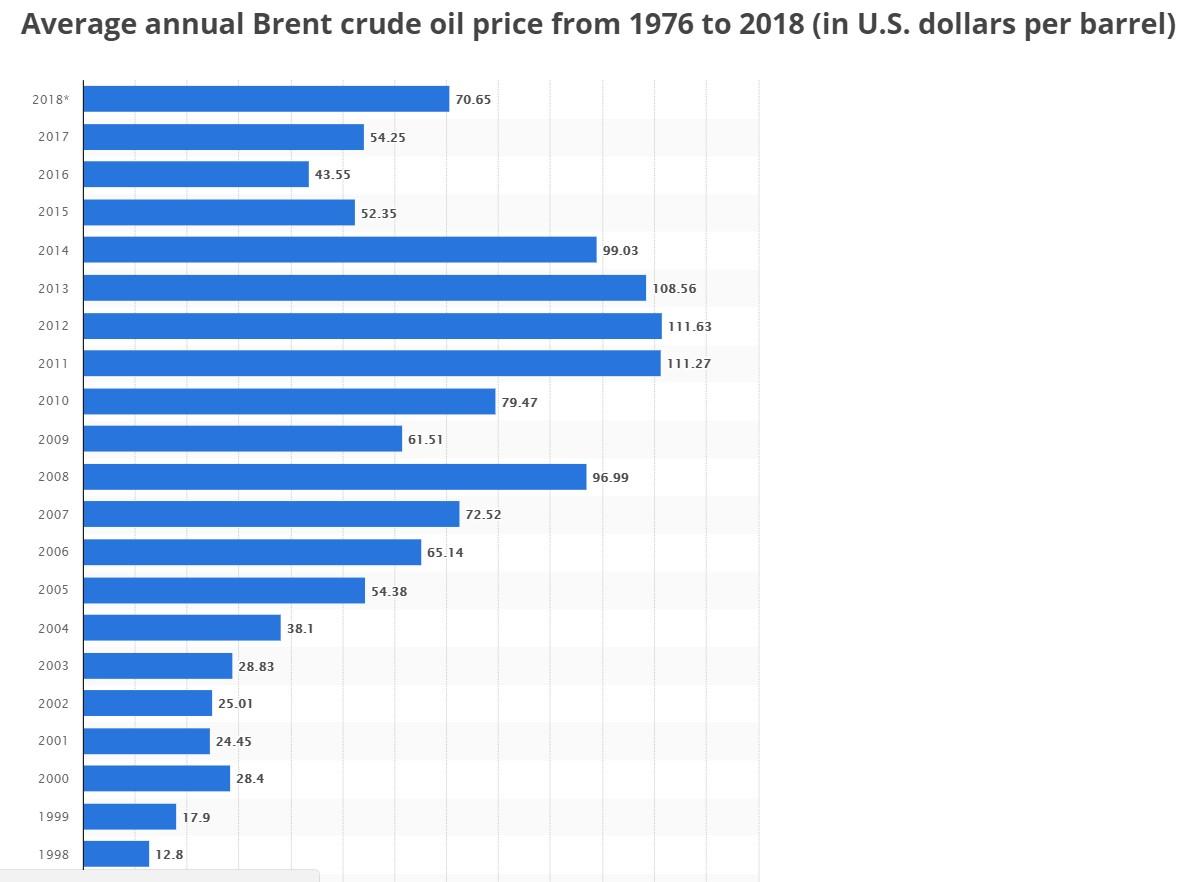

The evident impact and correlation of crude oil prices to the health of a global economy have led to experts attempting to track patterns and predict future fluctuations. Complex analytical models consider statistical and quantitative data as well as some of the qualitative factors discussed. Models vary in accuracy, performance stability, and bias which may provide differing forecasts. This section will attempt to outline the basic principles of the analytical models. As a background before the discussion of forecast models, below is a chart displaying average crude oil prices globally from 1999 to currently (Table 1).

As seen in the graph, the price of crude oil tripled from the early 2000s to 2008, only to undergo rapid fluctuations in both directions of as much as $50 per barrel in 1-2 years. The movements were largely unexpected and created macroeconomic pressures for both oil exporters and importers. The prominent nature of price fluctuations and the notorious difficulty of these predictions call for the development of accurate forecasting models.

VAR

One of the most popular analytical methods for crude oil prices is the reduced-form vector autoregressive (VAR) model. It implements critical variables that impact the real price of oil such as global production, inventories, and economic activity. The VAR model is traditionally considered the safest and more directionally accurate with a low real-time mean-squared prediction error. While VAR provides excellent real-time forecast accuracy, it is ultimately limited to stakeholders and policymakers. Reduced-form regression models fail to provide the driving factors for the forecast or explore alternative scenarios with an unconditional baseline.

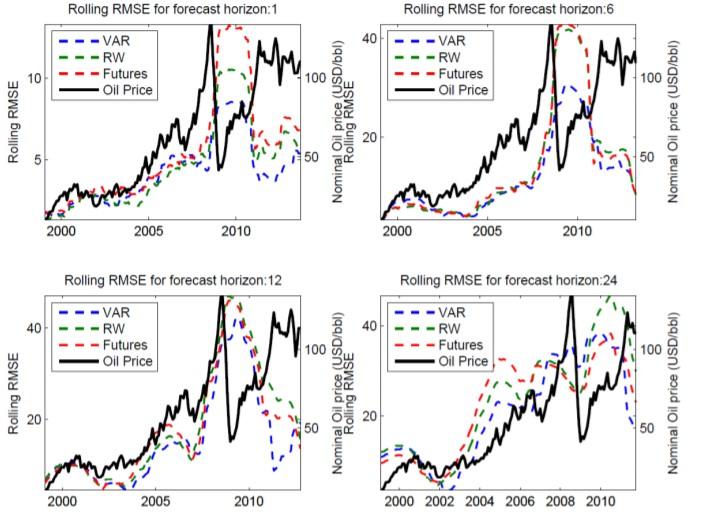

The VAR model is utilized for short to medium-term forecasts with models based on 12 and 24-month predictions. The standard reduced-form VAR formula consists of constants, vectors observables, and monthly parameters. Endogenous variables such as the global industrial production index, global oil production, and level changes on OECD inventories are considered. VAR has better predictability for medium-range forecasts, particularly during spikes in oil prices after 2006. The VAR model also excels during longer periods of 24 months, performing better than other models, especially in situations of gradually rising oil prices (Figure 3).

Granger Causality Model

Through the Granger causality model, it is evident that currency and inflation influence oil price fluctuations. However, this is not an effect unique to oil but is also evident in other global commodities such as gold. Since commerce is conducted primarily in US dollars, the monetary aspects cause particular nominal factors that influence oil trade processes. The price ratios impacted by the behavior of major actors such as the US Federal Reserve has led to the redistribution of debt, the rise in excess reserves, and higher liquidity in the economy which were an expected response to a financial crisis. Price stability had to be maintained through the increase of interest rates which served as a preventive measure from overwhelming demand or uncontrollable inflation. Therefore, the oil shock of the post-crisis years 2009-2014 was expected due to inflation being incorporated into the crude oil prices. Meanwhile, past 2014 when the reserves stopped rising, and there was a lesser concern about future inflation, the oil prices began to drop (Figure 4). The Granger causality model supports that oil prices are inherently tied to monetary factors and policy which may influence reserve and inflation levels.

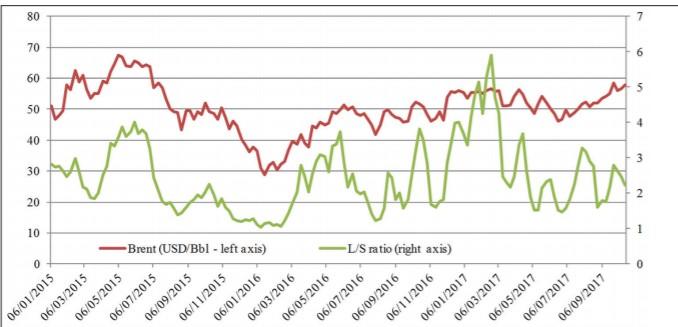

This interconnection with monetary aspects creates an opportunity for speculative trading which may also impact real oil prices. For example, the U.S. dollar exchange rate and oil prices have a complex but causal relationship. The Granger causality model through the use of wavelet analysis shows that within a short time scale of three months when there is speculative high-frequency trading, the causality runs from “real oil price returns to real effective US dollar exchange returns”. The chart below demonstrates that the relationship between the price of Brent oil and long to short ratio conversion is bidirectional. The price is indirectly manipulated through speculation by large-scale investors via crude oil stocks by as much as 10% (Figure 5). A Granger causality analysis demonstrates that money managers follow as well as create trends on the international market, thus forming positions for investment and speculation.

Conclusion

In conclusion, the global market of oil trading is defined by a wide variety of factors, events, and stakeholders. The real price of crude oil is dependent on concepts of market sentiments, inflation, and supply and demand. Governments and commercial traders seek to investigate trends and predict patterns of oil price movements through the use of analytical models which take into account quantitative aspects as well as qualitative causations. Using this information, they bid on oil futures contracts on commodity markets, thus affecting real oil prices at a future date and speculating on the price fluctuations which vary daily. It is critical to consider and study the price of oil as it continues to remain a primary commodity with a significant influence on macroeconomic risks and policies of many countries.

References

Aastveit, K. A., Bjørnland, H. C., & Thorsrud, L. A. (2014). What drives oil prices? Emerging versus developed economies. Journal of Applied Econometrics, 30(7), 1013-1028. Web.

American Petroleum Institute. (2014). Understanding crude oil and product markets. Web.

An, H., Zhong, W., Chen, Y., Li, H., & Gao, X. (2014). Features and evolution of international crude oil trade relationships: A trading-based network analysis. Energy, 74, 254-259. Web.

Arezki, R., Jakab, Z., Laxton, D., Matsumoto, A., Nurbekyan, A., Wang, H., & Yao, J. (2017). IMF working paper: Oil prices and the global economy. Web.

Backus, D. K., & Crucini, M. J. (2000). Oil prices and the terms of trade. Journal of International Economics, 50(1), 185-213.

Badel, A., & McGillicuddy, J. (2015). Oil prices and inflation expectations: Is there a link? Web.

Baffes, J., Kose, M. A., Ohnsorge, F., & Stocker, M. (2015). The great plunge in oil prices: Causes, consequences, and policy responses. Web.

Baumeister, C., & Kilian, L. (2012). Real-time analysis of oil price risks using forecast scenarios. Web.

Beckers, B., & Beidas-Strom, S. (2015). IMF working paper: Forecasting the nominal brent oil price with VARs—One model fits all?

Benhmad, F. (2012). Modeling nonlinear Granger causality between the oil price and U.S. dollar: A wavelet based approach. Economic Modelling, 29(4), 1505-1514. Web.

Benk, S., & Gillman, M. (2017). Granger-causality of real oil prices after the Great Recession. Web.

Choi, S., Furceri, D., Loungani, P., Mishra, S., & Poplawski-Ribeiro, M. (2017). IMF working paper: Oil Prices and inflation dynamics: Evidence from advanced and developing economies. Web.

Fleming, J., & Ostdiek, B. (1999). The impact of energy derivatives on the crude oil market. Energy Economics, 21(2), 135-167.

Hamilton, J. D. (2008). Understanding crude oil prices. Web.

Katircioglu, S. T., Sertoglu, K., Candemir, M., & Mercan, M. (2015). Oil price movements and macroeconomic performance: Evidence from twenty-six OECD countries. Renewable and Sustainable Energy Reviews, 44, 257-270. Web.

Morse, E. L. (1999). A new political economy of oil? Journal of International Affairs, 1, 1-29.

Obadi, S. M., & Korcek, M. (2018). The crude oil price and speculations: Investigation using Granger Causality Test. International Journal of Energy Economics and Policy, 8(3), 275-282.

US Energy Information Administration. (2018). Oil imports and exports. Web.

Villar, J. A., & Joutz, F. L. (2006). The relationship between crude oil and natural gas prices. Energy Information Administration, Office of Oil and Gas, 1, 1-43.

Zhong, W., An, H., Gao, X., & Sun, X. (2014). The evolution of communities in the international oil trade network. Physica A: Statistical Mechanics and Its Applications, 413, 42-52. Web.