Background

Artificial intelligence (AI) encompasses a diverse set of technologies that, in a broad sense, can be collectively described as “self-learning adaptive systems” (Jackson, 2019). AI is optimally viewed as a set of technologies and methods to complement traditional human qualities, such as intelligence, analytical abilities, and other skills. AI, machine learning (ML), and modern data processing methods have become largely possible thanks to recent advances in computer information processing, the power and speed of computers, and advancements in AI, which rely on data processing methods (Jackson, 2019).

A modern literature review shows a practical connection between science and finance, specifically accounting (Gordon, 2021). AI can generate forecasts and scenarios for the development of events, convert unorganized data sets into meaningful insights, and modify its behavior when business conditions shift. There is no denying that AI can become an invaluable tool for enhancing business in important professions, such as accounting, where training is necessary for professions that require technical accuracy and sound judgment. Additionally, AI offers significant opportunities for application (Parashar, 2021).

The daily duties of an accountant usually include compliance with archaic data analysis and reporting methodologies. Although many specialized software tools help automate data-oriented accounting, taxation, and audit tasks, accountants are still needed to verify and analyze this data using traditional methods. The Association of Chartered Accountants claims in one of its reports that AI-based automation will soon eliminate almost all tedious and cumbersome data-related tasks, such as accounting and transaction coding.

Logically, this should create a situation in which the business value of accountants and their consulting services increases significantly (Moll, 2019). As this technology develops and becomes more powerful, professional white-collar workers, including accountants, begin to worry about what the future holds for their careers and whether AI will render their work obsolete. Technological innovations have enhanced data availability, improving the efficiency and effectiveness of financial information provided to accountants.

According to Stancheva-Todorova (2018) and Chukwuani & Egiyi (2020), intelligent machines with AI can ensure compliance with numerous rules, regulations, and organizational policies. Consequently, providing more accurate and detailed data will improve the decision-making process. Moll & Yigitbasioglu (2019) and Munoko et al. (2020) have studied expert systems in large accounting firms.

Firms use expert systems primarily to reduce time and costs, allowing auditors to devote more time to making important decisions. The study also showed that accountants are skeptical about the reliability of financial information provided by automation. A lack of sufficient knowledge about big data and data analysis can lead to inappropriate results, and accountants may not be able to analyze and interpret the results correctly.

AI is relevant in modern realities, and its active implementation in all spheres of life, including accounting, raises many questions. One of the main issues is: how does process automation affect the work of accountants? Additionally, it is worth noting that, since the field is still in development, there is no consensus in the literature. Earlier studies contradict new ones. Therefore, this work will also aim to address the knowledge gap between AI and the accounting profession.

Research Objectives

- The primary purpose of this study is to study the impact of AI on the accountancy profession.

- Determine the impact of AI on the accounting industry.

- Evaluate the process of automation of the accounting system in the industry.

Research Aims

- This study will attempt to answer the following questions:

- What are the negative consequences of AI on the accounting industry?

- Does automation of the accounting process improve the accounting industry?

Literature Review

Artificial intelligence is a broad term that refers to technologies that enable machines to become “smart”. Accountants should be prepared to fully participate in organizational AI initiatives. The history of using AI in accounting dates back to the 1980s (Jackson, 2019). Using statistical methods and econometric models, AI can generate forecasts and scenarios of events, transform a series of unstructured data into useful information, and adjust its actions in response to changes in business conditions. McCarthy gave the complete definition of AI in 1956 (Mir et al., 2020). According to the so-called father of AI, John McCarthy, it is a science for creating intelligent machines and brilliant computer programs.

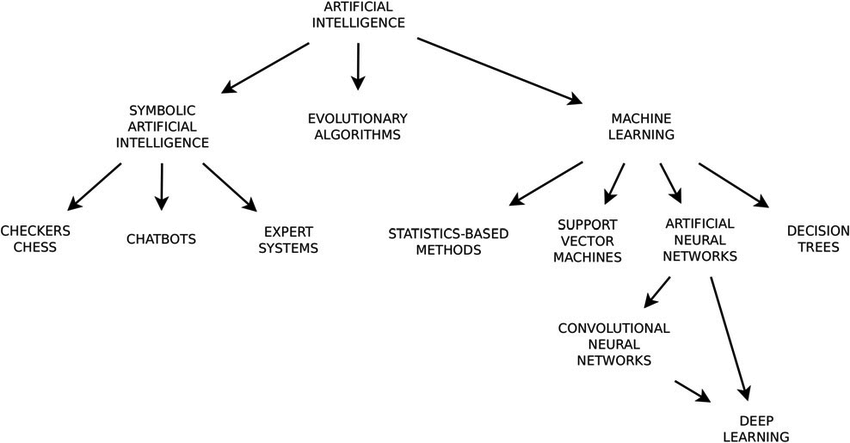

Scientists and practitioners have extensively researched the use of AI in auditing, taxation, financial accounting, management accounting, and personal financial planning. The development and use of Expert Systems (ESs) in the accounting discipline is probably the most studied area. Kuzior et al. (2019) and Jędrzejka (2019) were viewed as programmers attempting to replicate the behavior and experience of human experts, preserve their knowledge and experience, and transform it into rules, thereby aiming to solve accounting problems and perform specific accounting tasks. The schematic overview below illustrates the main branches of AI (Galbusera et al., 2019).

Next to these early, even rather primitive attempts at automation, is the accountants’ constant willingness to improve the efficiency of their work and bring more benefits to the business. Recent technological breakthroughs in AI are now turning a new page in the accounting discipline, refocusing research from ES applications to new perspectives for practicing accountants:

- How can accountants benefit from the use of AI capabilities?

- What is the long-term vision of AI and accounting?

- How will AI change the roles of accounting in the organization?

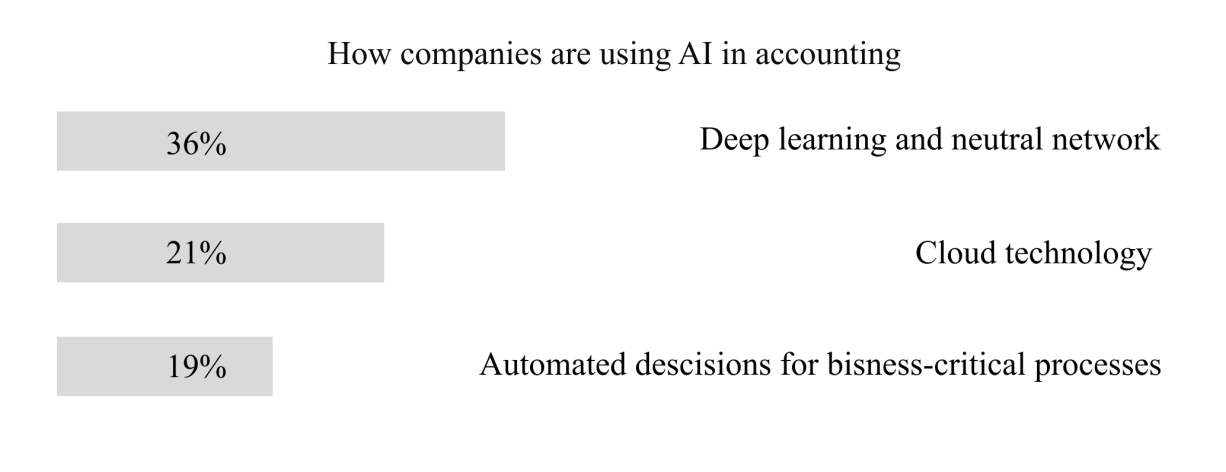

The graph below illustrates the distribution of how companies utilize AI most frequently (Cho et al., 2020).

These new generations of machine learning systems have a significant impact on the economy and business, and they also bring new lifestyle and sociological side effects (Caldwell et al., 2020). Stephen Hawking warned in early 2014 that the development of a full-fledged AI could mean the end of the human race. He said that once humans develop AI, it can take off on its own and redesign itself at an ever-increasing rate.

Humans, limited by slow biological evolution, would be unable to compete and would be pushed out(Tai, 2020). These assumptions resonate in many subsequent debates and discussions. Some of their supporters argue that the existential threat is accurate and that robots may replace humans in the near future. They will make better decisions faster and without bias. It appears that the “singularity,” the moment when AI surpasses human intelligence, marks the beginning of a dark era for humanity (Yakimova, 2020; Güngör, 2020).

The research conducted by the consulting company BrightEdge focuses on analyzing the structure of AI technologies and their impact on the development of various economic sectors (Predicts the Future and Impacts of AI Beyond, 2021). The results are listed below. The experts who processed the data also noted that the number of respondents using AI technologies in their daily activities often exceeds the number of respondents who answered affirmatively to questions about their experience of interacting with AI.

As the main advantages and capabilities of AI technologies, users note the possibilities of saving time on operations, the possibility of accelerating the achievement of goals in solving management problems and tasks, the opportunity for faster and deeper data analysis, higher accuracy in reaching target audiences, and organizing segmentation of the client group market, the possibility of accurate long-term forecasting, the possibility of freeing up staff time for due to the restructuring of the solution of routine and repetitive tasks to algorithms and AI technologies.

Despite the considerable attention paid by state and international organizations to the development of AI technologies, it is worth noting that AI is a relatively new phenomenon in the accounting system (Jackson, 2019). The usage of the traditional accounting system has significantly come to naught. Automating the accounting process has led to many changes, but are these changes beneficial for the accounting profession?

The above empirical literature review highlights that research has primarily focused on new advances in AI and the accounting profession, particularly in large and developed companies. Still, there have been no studies on medium and small-sized enterprises. There are some studies whose results contradict each other (Moll, 2019; Gordon, 2021; Parashar, 2021). Also, these studies only suggest a possible future positive or negative impact. Therefore, the research will aim to address the knowledge gap between AI and the accounting profession.

Method and Design

Research Philosophy

In the social sciences and humanities, a distinct type of explanation should be employed, which differs from the descriptions used in the natural sciences. Since social and humanitarian knowledge describes a unique object — people who have consciousness and endow their actions with meaning, which is unusual for physical objects and events. The research process, by the interpretivism paradigm, is based on the “methodology of understanding” — the researcher and the subject must find the correct language for interpreting the meaning of what is happening, through which they come to a common understanding of the meaning of what is happening to them (Kelly, 2018).

At the same time, interpretivism philosophy can create a rich understanding and interpretation of social worlds and contexts. Interpretivism uses smaller data samples. Therefore, accountants will be considered social subjects in this study. Thus, the interpretive paradigm is the most appropriate for this work. The positivist approach is unsuitable because it requires an observable social reality, which is not the case in this instance, where introducing future technologies is not yet observable.

Critical realism is essential for advancing historical knowledge because it emphasizes an individual point of view. Since we are studying only the initial stages of change, this approach is unsuitable. Postmodern philosophy asserts that nothing is objective and that our perception always distorts our view of the unvarnished truth, rendering it impossible to draw general conclusions (Kelly, 2018).

Approach of the Study

The inductive method characterizes the path of cognition from the fixation of empirical data and their analysis to their systematization, generalization, and the drawing of general conclusions based on this basis. This method also involves transitioning from initial ideas about certain phenomena and processes to more widespread and often more profound ones (Woiceshyn, 2018). In this case, the deductive method is unsuitable because it requires moving from data to conclusions. An inductive approach will be used since it can lead to general conclusions from the obtained private data.

Type of the Study

This study will employ a descriptive survey to examine the impact of AI on the accounting profession. The target audience will consist of accountants of medium and small financial and accounting organizations. The rational choice of the descriptive design for the study was to examine the current opportunities and threats of AI for accounting functions in small and medium-sized enterprises. An explanatory study is not suitable since, to date, we have not been able to effectively link theory and practice. However, this may be a further stage of the study.

Strategy

The grounded theory will be used to explain what can happen due to technology-related changes in a social environment where no existing hypothesis exists. Data for this study will be collected mainly through questionnaires. It will be compiled on a 5-point Likert scale, using closed-ended questions. As a result of completing the questionnaires, primary data will be collected. Since the main research questions concern the primary negative and positive consequences of AI for the accounting industry, it is necessary to select as a sample precisely those companies that have already begun to implement automation in their workflows.

During the survey, accountants will be asked to assess how their workflow has changed before and after the introduction of AI. The survey will also collect information about the distribution of working time between accounting tasks before and after the automation of processes. This will enable the collection of standardized and economically justified data from the actual population. This strategy was more appropriate than an experiment or a case study. In the case of the experiment, it is not yet possible to establish a cause-and-effect relationship accurately. In the case study, there are examples of studies where AI affects other professions. Still, they do not relate to the specific activities of accountants.

Data and Analysis

The primary source will be the survey results. The existing literature on AI and its impact on accounting, as well as various online resources, will be used as secondary sources. The research method will follow the quantitative approach proposed for studying business and management to understand the complex dynamics of the industry (Busetto, 2020). The combination of quantitative survey results and primary and secondary sources will ensure the reliability and generalizability of the research data.

To evaluate the ordinal characteristics of the answers (the most likely and least possible solutions), nonparametric analysis will be used, specifically the Chi-squared test in Excel, along with additional demographic analysis. Median and modal approaches will be used to analyze data on the Likert scale. In this case, a parametric analysis could be applied. Still, it would not be effective because the distribution of responses is abnormal.

A questionnaire with closed questions will be developed, indicating the main areas of tasks that are now automated. These tasks will be compiled based on initial interviews with accountants of the companies under study. For each of these tasks, assessing the impact of introducing AI in the Likert school will be necessary. This will be presented in simple and understandable language to minimize ambiguity and misunderstanding among respondents.

Reference demographic information, such as age, experience, position, income, and gender, will also be collected. The table below shows an approximate list of questions for the questionnaire.

- The automation of departmental budgeting has affected your work.

- The automation of the financial model has affected your work.

- The automation of financial data interpretation has impacted your work.

- The usage of AI has led to a reduction in jobs in your company.

- Automation of financial processes caused difficulties associated with consumer preferences.

To access the data, it is necessary to analyze small and medium-sized enterprises in the accounting field in the city. After that, it is essential to send an introductory letter to the selected companies, provide an annotation for the study, and determine if any AI systems have been implemented in the work process. Furthermore, arranging initial interviews with suitable companies is necessary to clarify which processes have become automated.

The number of employees who worked on these tasks before and after implementation will be chosen. A specially designed questionnaire will be used to ensure efficient use of participants’ time. Moreover, it is essential to address the ethical aspects of the study, including creating a confidential and sensitive environment.

Ethical Issues

Since confidential commercial information may be used during the survey, social groups may have particular consequences. Thus, the issues of consent, confidentiality, sensitivity, and privacy will be used to solve ethical problems. Before conducting the survey, written permission and an abstract of the study will be obtained, clearly stating the goals, methods, potential results, and ethical standards. All data will be securely stored to ensure the confidentiality and anonymity of participants. It will remain the property of the researcher and will not be transferred or disclosed to any third party.

Reference List

Busetto, L., Wick, W., & Gumbinger, C. (2020) ‘How to use and assess qualitative research methods’, Neurological Research and Practice, 2(1), pp. 1-10.

Caldwell, M., Andrews, J. T. A., Tanay, T., & Griffin, L. D. (2020) ‘AI-enabled future crime’, Crime Science, 9(1), pp. 1-13.

Cho, S., et al. (2020) ‘Learning from machine learning in accounting and assurance’, Journal of Emerging Technologies in Accounting, 17(1), pp. 1-10.

Chukwuani, V. N., & Egiyi, M. A. (2020). ‘Automation of Accounting Processes: Impact of Artificial Intelligence’, International Journal of Research and Innovation in Social Science (IJRISS), 4(8), pp. 444-449.

Predicts the Future and Impacts of AI Beyond (2021) Web.

Galbusera, F., Casaroli, G., & Bassani, T. (2019) ‘Artificial intelligence and machine learning in spine research’, JOR spine, 2(1), e1044.

Gordon, J. S. (2021) ‘Artificial moral and legal personhood’, AI & society, 36(2), pp. 457-471.

Güngör, H. (2020) ‘Creating value with artificial intelligence: A multi-stakeholder perspective’, Journal of Creating Value, 6(1), pp. 72-85.

Jackson, P. C. (2019) Introduction to artificial intelligence. Courier Dover Publications.

Jędrzejka, D. (2019) ‘Robotic process automation and its impact on accounting’, Zeszyty Teoretyczne Rachunkowości, (105 (161)), pp. 137-166.

Kelly, M., Dowling, M., & Millar, M. (2018) ‘The search for understanding: The role of paradigms’, Nurse researcher, 25(4), pp. 9-13.

Kuzior, A., Kwilinski, A., & Tkachenko, V. (2019) ‘Sustainable development of organizations based on the combinatorial model of artificial intelligence’, Entrepreneurship and Sustainability Issues, 7(2), p. 1353.

Mir, U. B., et al. (2020) Critical success factors for integrating artificial intelligence and robotics. Digital Policy, Regulation and Governance.

Moll, J., & Yigitbasioglu, O. (2019) ‘The role of internet-related technologies in shaping the work of accountants: New directions for accounting research’, The British Accounting Review, 51(6), 100833.

Munoko, I., Brown-Liburd, H. L., & Vasarhelyi, M. (2020) ‘The ethical implications of using artificial intelligence in auditing’, Journal of Business Ethics, 167(2), pp. 209-234.

Parashar, B., & Rana, G. (2021). The Impact of Artificial Intelligence on Global Business Practices. In Reinventing Manufacturing and Business Processes Through Artificial Intelligence (pp. 95-113). CRC Press.

Stancheva-Todorova, E. P. (2018) ‘How artificial intelligence is challenging accounting profession’, Journal of International Scientific Publications” Economy & Business, 12, pp. 126-141.

Tai M. C. (2020) ‘The impact of artificial intelligence on human society and bioethics’, Tzu chi medical journal, 32(4), pp. 339–343.

Woiceshyn, J., & Daellenbach, U. (2018) ‘Evaluating inductive vs deductive research in management studies: Implications for authors, editors, and reviewers’, Qualitative research in organizations and management: An International Journal.

Yakimova, V. A. (2020) ‘Opportunities and prospects for using digital technologies in auditing’, Bulletin of St. Petersburg University. Econom, 36(2). pp. 287–318.