Introduction

The phrase ‘subprime mortgage crisis’ became common in 2007. It describes the decline in the performance of the United States of America mortgage market (Tong & Wei, 2008, p. 3). The 2007 subprime mortgage crisis is described as the most terrible financial crisis to have occurred since the previous Great Depression. The financial crisis has adversely affected other economic sectors such as the real sector. One of the factors associated with the financial crisis is an increase in the number of subprime loans advanced (Sanders, 2008, p.254). After the end of the 2nd world war, a large number of people could own homes due to the development of mortgage credit which was affordable to middle-class households. However, individuals with low credit ratings could not own homes (Fratantoni & Schuh, 2003, p.558). This arose from the fact they could not access the mortgage from financial institutions. One of the factors which contributed to this was the high-interest rate associated with the mortgages and the requirement to pay monthly installments (Gramlich, 2007, p. 2). This was worsened by the occurrence of the financial crisis.

The core objective of this chapter is to conduct a review of the subprime mortgage crisis in the US and compare it with the UK. The chapter is organized into a number of sections. The first part entails a definition of what the subprime mortgage crisis entails. Subprime mortgage crisis causal factors are analyzed in the second part. This is undertaken by considering elements such as the rate of interest, increased financial product innovation, imbalances in the global market in relation to investment and deposits, expectations of house prices, increased bank credit and information asymmetry.

Subprime Mortgage Crisis

In the recent past, the US has witnessed an increment in the number of homeownership. For example, in 1994, the overall homeownership averaged 64% (Gramlich, 2007, p.7). However, there was a boom in ownership by 2005 with homeownership increasing to 69 % (Demyanyk & Hemert, 2008, p. 5). As a result, approximately 12 million Americans were able to own homes (Gramlich, 2007, p.3). The increment in homeownership is associated with the emergence of subprime loans which provided an alternative source of money for these individuals.

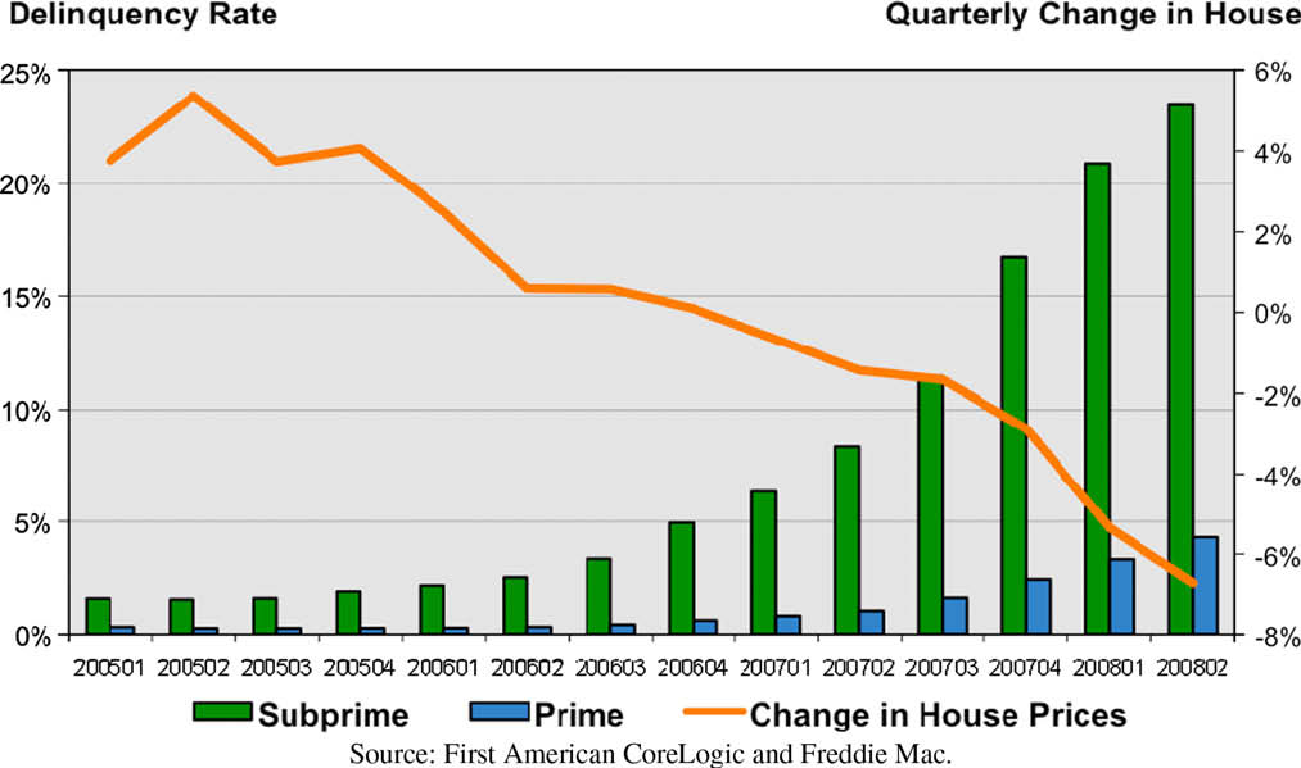

The core objective of subprime loans was to aid individuals to strengthen the borrowers’ financial capacity (Demyanyk & Hemert, 2008, p. 5). According to Reed (p.136), approximately 25% of individuals made use of subprime loans in their mortgages. From the graph below, it is evident that there was a steady increment in subprime loans for the period ranging from 2005 to 2008. On the other hand, there was a steady decline in housing prices during the same period as illustrated in the graph below.

Graph showing growth in subprime loans for the period ranging from 2005 to 2008.

As a result, a significant proportion of financial institutions considered integrating subprime mortgages in their lending practices. In the introductory phase, the interest rate subprime rate is relatively low. In most cases, the interest rate for the subprime loan is set at 2/28. This means that the loan holder is subjected to a fixed interest rate for the first 2 years (Gramlich, 2007, p.3). However, the interest rate for the other years becomes an ARM (Adjustable Rate Mortgages). This means that the rate of interest applicable on the loan increases. This can result in an increment in the number of foreclosures since homeowners cannot be able to meet their mortgage payments.

According to Gramlich (2007, p.4), most of the subprime loan borrowers are low-income individuals who are prone to loss of income hence affecting their payment ability. The occurrence of the 2007 financial crisis had a negative effect on the payment of the subprime mortgages loan interest and monthly installment. 2007 witnessed an increment in the number of foreclosures in relation to subprime mortgages both in the US and the UK. An increment in the rate of interest resulted in a reduction in the demand for homes which culminated into a reduction in the price of homes as illustrated in the graph above.

Subprime Crisis

Low-interest rate

In an effort to attract customers of the lower-income class, financial institutions decrease their threshold in relation to subprime mortgages. The resultant effect is that individuals can easily borrow money. This policy stimulated subprime mortgage market growth (Shijian, 2008, p.1). The resultant effect has been a growth in various economic sectors (Ayuso, Blanco & Restoy, 2006, p. 9). Before the occurrence of the crisis, the US Federal Reserve conducted a massive reduction in the rate of interest. The core objective was to safeguard the occurrence of a recession considering the previous tech bubble.

According to Hoffinger (2009, p.3), the Fed implemented an expansionary monetary policy. This was conducted through an aggressive reduction in the interest rate at the onset of the decade. In an effort to stimulate the country’s economic growth, Fed prolonged its low-interest-rate policy for the duration ranging from 2000 to 2004. The result was an increment in demand for housing as individuals considered investing in the real estate sector as the most appropriate. The rise in demand culminated in an increase in housing prices.

Reduction in the rate of interest stimulated the growth of various economic sectors such as the housing sector. Teaser rates of interest were integrated in both US and the UK housing sector (Whitehead, 2010, p.11). For example, in 2003, the Fed’s rate of interest was 1%. The low rate of interest culminated in an increment in mortgage financing. The low rate of interest coupled with low down payment requirements made adjustable loans to become very attractive to investors.

According to Hoffinger (2009, p.3), a low interest rate stimulates a country’s economic growth culminating in economic expansion. This arises from the fact that liquidity amongst financial institutions is increased. The resultant effect is that financial institutions start to advance credit services to individuals whose creditworthiness was low.

A turning point occurred within the US housing industry in 2006. This resulted from an increment in the rate of interest due to the incorporation of the Adjustable Rate Mortgage concept. By 2006, the rate of interest was adjusted to approximately 5.25% and 6% (Gramlich, 2007, p.14). This represents a significant increment in their interest payment considering the fact that the subprime mortgage holders paid approximately 2% to 3% during the 1st five years (Gramlich, 2007, p.11).

As a result of low-interest rates, financial institutions which were issuing mortgages relaxed their lending standards due to increased demand. Swan (2009, p.126) asserts that the spread between subprime and prime mortgages reduced from 2.8% to approximately 0.6% from 2001 to 2004. This clearly indicates that demand in relation to securitized mortgages. This was further instigated by increased optimism with regard to speculations on housing prices. Non-prime mortgages market which is composed of Alt-A loans a, subprime and near-prime mortgages experienced explosive growth during the period ranging from 2001 to 2006(Swan, 2009, p.126).

Over financial product innovation

Excessive financial product innovation is one of the reasons why the US witnessed subprime mortgage crises. US banks have increasingly realized the importance of product designing in an effort to maximize their profit and attain a high competitive advantage (Ding & Li, 2009, p.8).

The US mortgage market is divided into two (Ding & Li, 2009, p. 114). These include the Fixed Rate Mortgages (FRMs) and Adjustable Rate Mortgages (Adjustable Rate Mortgages (ARMs).FRMs are characterized by a fixed rate of interest for the entire period of the loan. On the other hand, ARMs have a variable interest rate which is based on a predetermined index in addition to a fixed margin (Jansen & Linsmann, 2008, p. 2). The period ranging from 2003 to 2006 witnessed an increment in the number of Alternative Mortgage Products (ARMs). These products were mainly issued to individuals with a high default rate (Kirk, 2007, p.2). Some of these products included the Mortgage-Backed Securities (MBS).

As a result of financial product innovation in the housing industry with regard to mortgages, there was an increment in the rate of mortgage securitization. Mortgage securitization involves pooling a number of mortgages that are used as collateral in issuing a particular asset. Cash flows from these mortgages are used in paying the mortgage. According to Swan (2009, p.126), there was an increment in the volume of subprime loans advanced during the period ranging from 2001 to 2005. The amount of loan advanced increased by approximately 45%. However, the volume of loans reduced in 2006 to settle at 2,646,000 (Kirk, 2007, p.19). Approximately 85% of these loans consisted of securitized subprime mortgages. Swan asserts that these loans are characterized by a relatively high default risk compared to prime loans. This arises from the fact that securitized mortgages are also issued to individuals with a low credit score.

The financial crisis culminated in a decline in personal income which made it hard for individuals to service their mortgages (Kirk, 2007, p.13). The subprime mortgage crisis was further exacerbated by rising in the rate of interest applicable to mortgages. The resultant effect was a decline in the value of mortgages leading to a loss by holders of MBS. The losses led to a lack of confidence by investors in these assets due to the high degree of uncertainty. The complexity of MBS made the process of determining their value challenging. Rating agencies conducted poor ratings on financial products developed by financial institutions such as mortgages. This resulted from the use of backward and inefficient valuation methods which culminated in a gross underestimation of risk (Ding & Li, 2009, p.8).

Information asymmetry

Increased information asymmetry within the financial sector is one of the criticisms that are associated with the 2007 subprime mortgage crisis (Ding & Li, 2009, p. 110). One of the reasons why financial institutions did not disclose the associated risk is the associated complexity. According to Bhat & Jayaraman (2009, p.1), there has been an increased failure in financial institutions’ reporting process. Bhat and Jayaraman asserts that financial institutions have not been effective in providing timely information regarding their performance.

According to Fitzpatrick and McQuinn (2007, p.84), the presence of information asymmetry among financial institutions creates a conducive environment for financial accelerators. Financial accelerators have the effect of reducing an individual’s borrowing capacity whereby borrowers are required to have collateral in order to access finance from the financial institutions (Ding & Li, 2009, p. 104).

Excessive bank credit

Over the past decade, there has been significant growth in the amount of credit advanced by banks. By increasing banks’ liquidity, the bank’s lending capacity is increased. In addition, increased liquidity culminates in a reduction in the rate of interest. One of these forms of credit which were affected by increased bank liquidity includes mortgages. As a result, mortgage credit ranks first in comparison to other forms of credit.

Over the past decade, the UK and US mortgage markets have undergone rampant expansion. The rampant growth is associated with a credit boom that made banks loosen their lending standards.

According to Dell’Ariccia, Igan and Laeven (2008, p. 1), there is a 50% to 75% probability of a banking crisis occurring during credit booms. The current mortgage delinquencies experienced in the subprime mortgage market are linked to past credit growth (Kirk, 2007, p.22). The rapid growth in the subprime mortgage market is linked to the relaxation of credit standards. The subprime mortgage crisis was severe in countries which experienced a high credit boom compared to those with low credit boom. There has been an increment in the number of subprime mortgage lending in relation to the total number of loans issued and loans originated in both markets (Kirk, 2007, p.33).

Mankiw (2006, p. 551) asserts that when the rate of interest is high, the cost of accessing loans from a financial institution is high. During these periods, few investors are motivated to borrow in order to buy a house. The resultant effect of a high-interest rate is a decline in investment within the real estate sector. Availability of credit culminated into house price appreciation. This arose from a general notion that investors were gambling for the housing boom. According to Mankiw (2006, p.551), a rise in house prices culminates in an increment in money demand. This further pushes the interest rate up. The lenders believed that mortgage holders could easily liquidate their collateral in order to repay their loan (Dell’Ariccia, Igan & Laeven, 2008, p. 18). During the housing boom period, consumer spending was high while saving was low. In addition, the investors increased their debt which became difficult to pay upon the occurrence of the financial crisis.

According to Dell’Ariccia, Igan & Laeven (2008, p. 18), the easy initial terms incorporated by banks in advancing mortgages encouraged investors to take more risky mortgages. This arose from the fact that they believed that they could easily refinance the mortgages at much more favorable terms. When the interest rate applicable to mortgages began to rise while house prices decreased, it became difficult for individuals to refinance their mortgages (Dell’Ariccia, Igan & Laeven, 2008, p. 19).

House price expectation

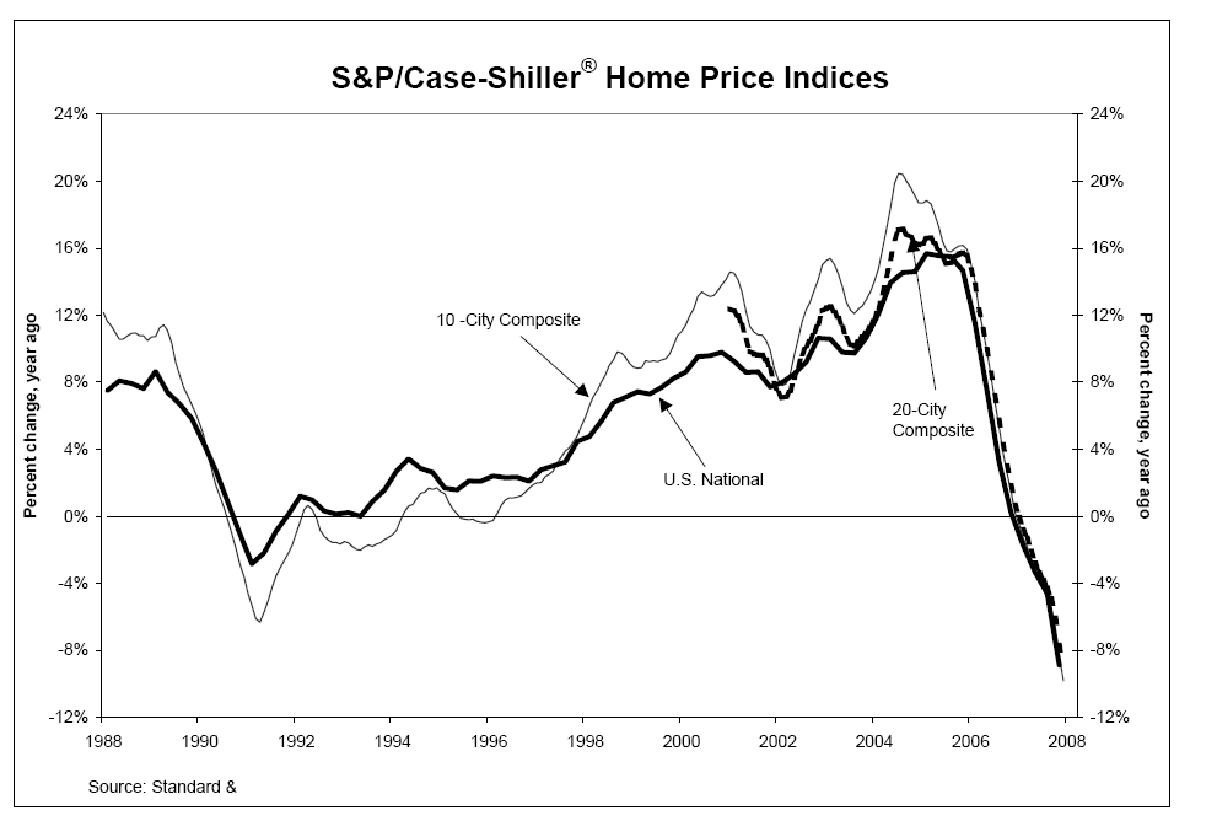

Before the occurrence of the subprime mortgage crisis, there was a shift in perception with regard to housing whereby individuals perceived housing as an investment with high appreciation potential. It is evident that there was an appreciation in housing prices in the US for the period ranging from 2000 to 2006 (Tucker, 2008, p.2). However, this did not persist for a long period. 2006 witnessed a significant reduction in housing prices. The result was a reduction in demand for investors due to a reduction in value. This means that it was difficult for lenders to recoup the advanced amount in terms of mortgages.

Graph showing movement of house prices in the US from 1986 to 2008.

According to Goetzmann and Yen (2009, p. 1), past increments in the price of houses may depict low default risk. This arises from the fact that there is the expectation of the debt-to-value ratio decreasing with future increments in house prices.

Imbalances between investment and deposits

Global macro-economic imbalances played a vital role in stimulating the current subprime mortgage crisis. This arose from the increment in the rate of globalization. Countries such as the UK, United States, Portugal, Greece, Spain, Turkey, East and Central European counties had huge current account deficits. On the other hand, countries such as Taiwan, Korea, China, Japan and Malaysia had current account surpluses. This imbalance in addition to capital flows resulted in a decline in the rate of interest in the UK and United States financial institutions (Martin & Milas, 2008, p. 45).

The rate of consumption was further stimulated (Hongyu & Yue, 2005, p. 335). As a result, financial institutions in the UK and US increased their search for investment destinations where they would achieve higher yields. This means that there was an increment in risk-taking whereby financial institutions relied on opaque and composite financial instruments. The influx in the number of investors who considered the housing industry as an optimal investment destination was instigated by consideration of the sector as a safe investment vehicle due to the low liquidity associated with the sector.

Relationship between monetary policy and house price in the USA

Monetary policy refers to the process that is used by the government through the central bank in regulating the amount of money supply within the economy. This is undertaken by regulating the rate of interest (Gowland, 2007, p. 76). Depending on the economic conditions in the country, the government can either conduct expansionary or contractionary monetary policy (Uhlig, 2005, p. 384).

Over the past decades, US federal bank has been committed to improving the country’s economic performance through the attainment of macroeconomic goals which include price stability, high employment and sustainable economic growth. One of the methods incorporated by the Fed to ensure that this is attained is increasing the money supply. There are various mechanisms that firms can be incorporated by Fed in order to increase the money supply. One of these mechanisms relates to reducing the reserve deposit ratio. According to Leonard (2007, p. 148), a reserve deposit refers to the minimum amount of money that commercial banks should have in their accounts at the central bank at all times. By shrinking the reserve deposit ratio, the central bank of a given country is able to increase the amount of money supply in the economy Leonard (2007, p. 148). Fed reduced the minimum amount of bank deposit reserves applicable to commercial banks. In an effort to stimulate the economy through expansionary monetary policy, Fed increased the number of loans it issues to commercial banks. When there is a high demand for money relative to supply, the market rate of interest tends to increase. This limits the amount of bank credit thus slowing economic growth. Fed increased the amount of bank credit in an effort to enhance adequate economic growth in all sectors (Public Information Officer, 2000, p. 3). The core objective of this expansionary policy was to increase bank lending to both households and businesses. As a result, commercial banks had a sufficient amount of money to lend to potential investors. In an effort to attain a high competitive advantage, commercial banks increased their relaxed their lending standards. However, banks extended their lending practices to individuals with low credit ratings culminating in the subprime mortgage crisis.

In addition, the US Federal Reserve increased the money supply in financial institutions by lowering the rate of interest in early 2000 (Uhlig, 2005, p. 388). This was aimed at preventing the country from experiencing a recession after the 2001 terror attack and the hi-tech meltdown (Uhlig, 2005, p. 382).

The loose monetary policy resulted in an expansion in various economic sectors. Various sectors in the US housing industry witnessed rampant growth during the period ranging from 2000 to 2004 as a result of the loose monetary policy adopted by the Federal Bank (Eickmeier & Hofmann, 2009, p. 19).. Some of these sectors include sale, resale and construction of residential properties. This arises from the fact that investors could be able to access finance from financial institutions and invest in the housing sector. For instance, as a result of loose monetary policy in the US, the commercial banks expanded their businesses.

The economic growth witnessed by the US during this period increased the level of confidence amongst commercial banks in issuing loans. This arose from the fact that the country’s economic growth resulted in an increment in the citizen’s disposable income.

One of the ways through which the loose monetary policy implemented by the Fed resulted in the housing industry crisis was as a result of relaxing the standards applicable to mortgages. In an effort to attain a high market share, commercial banks and other financial institutions issued loans to investors with a low credit rating due to increased investment demand. According to Eicmeier and Hoffman (2010, p.10), monetary policy shocks have an effect on the price of assets in various economic sectors. For example, a loose monetary policy results in a decline in the applicable rate of interest. Low rates of interest contributed to imbalances within the housing industry.

Increased liquidity made homes affordable to individuals of diverse income classes leading to an outward shift in demand (Whalen, 2008, p.9). An increase in demand had the effect of increasing house prices. Before the NASDAQ bubble, financial institutions considered individuals with Fair Isaac Corporation (FICO) scores less than 620 not eligible for a loan. Due to the high risk of default associated with this category of borrowers, the financial institutions set the applicable rate of interest to be relatively high. As a result, most US banks lost. This had an effect on the UK considering the fact that most Briton mortgage lenders depend on revenue resulting from the sale of mortgage debts banks in the United States a process known as securitization. The collapse of US banks made the UK banks cease purchasing the loan books. The resultant effect is that the UK banks could no longer be able to subsidize its low-interest rates (O’Connor, 2010, para. 8).

The decline in house prices culminated in an increment in the rate of delinquencies and foreclosures. These were made worse by increased incorporation of subprime mortgages and the integration of ARMs which culminated in excessive risk-taking.

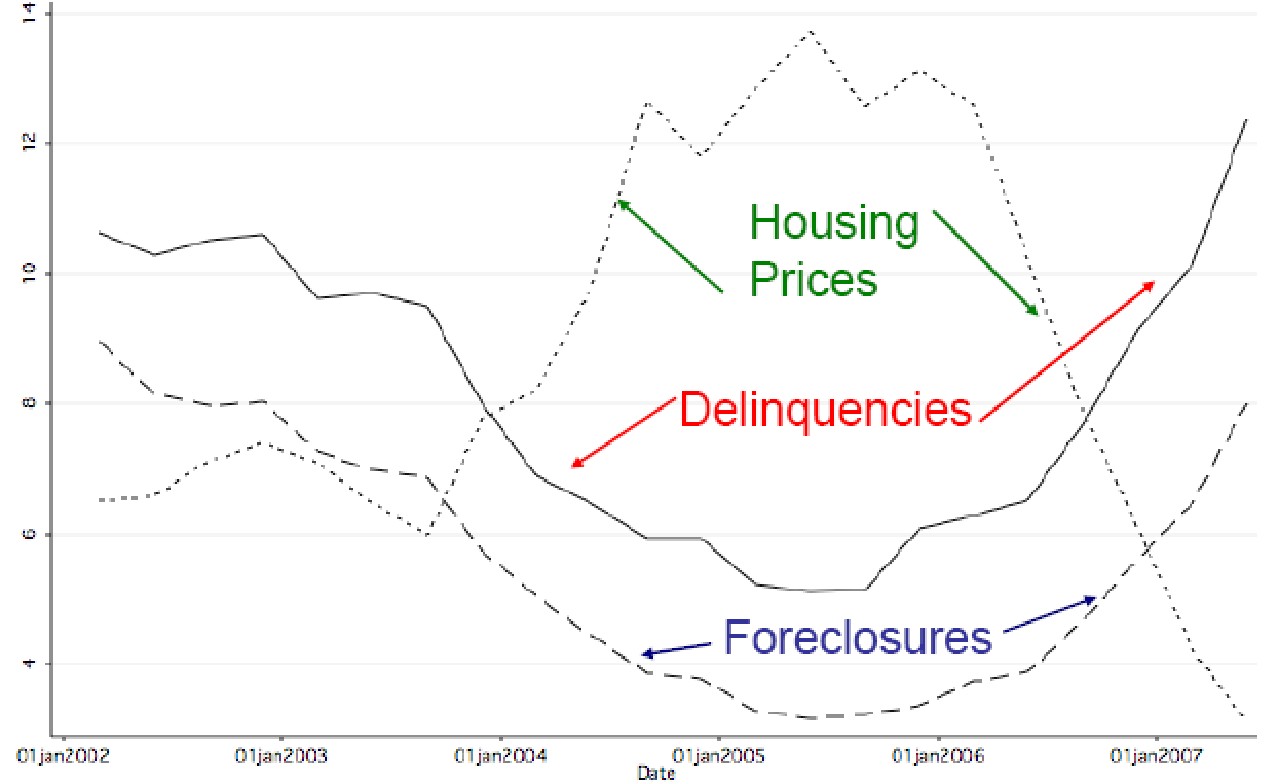

In the United States, the situation in the housing industry was made worse by government programs (expansionary monetary policy) which were aimed at promoting homeownership (Swan, 2009, p. 125). The graph below illustrates a sharp increase in the rate of inflation within the US housing industry from 2003 to 2006. This was followed by a subsequent decline. During this period, foreclosure and delinquency rates were inversely related. Upon the rise in house prices, there was a decline in foreclosure and delinquency rates.

Increased liquidity led to the housing bubble which culminated in the housing industry collapsing. The low rate of interest stimulated demand for investing in the housing sector. This arises from the fact that investors considered it a potential investment destination after a decline in the rate of interest applicable to treasury bills which were considered as a safe investments. In their investment decision, investors integrated the concept of high-risk high return (Swan, 2009, p. 125).

Poor regulation

An effective global financial system is determined by the effectiveness with which the economy is regulated (Uhlig, 2005, p. 282). Inefficient financial regulation played a significant role in the current subprime crisis. Despite the US government’s effort in stimulating economic growth after the dot-com bubble, the monetary policy it implemented was not well regulated (Swan, 2009, p. 122). The government via the Fed undertook a significant reduction in the rate of interest thus increasing the money supply in the economy. Banking is characterized as a highly leveraged sector as it entails public borrowing via deposits or financial instruments such as commercial paper.

The government did not ensure effective information disclosure amongst financial institutions in issuing securities that were backed by subprime mortgages (Ryan, 2008, p. 5). This increased the degree of risk faced by such investors. Numerous individual and institutional investors bought securities that were backed by subprime mortgages based on their rating. This was made worse by the complexity of the mortgages as investment vehicles (Schwarz, 2008, p.1).

Summary

From the analysis above, it is evident that the US and the UK subprime mortgage crisis resulted from a number of factors. In an effort to improve the performance of the economy, the US government via the Fed undertook expansionary monetary policy. This was undertaken by reducing the rate of interest during the early to mid-2000. The result was a significant increase in the demand for finances from the financial institution since the cost of capital was relatively low.

Reduction in the rate of interest stimulated investment demand in various economic sectors. One of the sectors which investors regarded as a viable investment destination was the housing industry. Demand was further stimulated by expectations of future increments in the price of houses. As a result, investors perceived a high probability of increasing their yield from investing in the real estate sector. This means that the housing sector was perceived as an investment rather than for ordinary housing purposes. The occurrence of the subprime crisis posed a challenging task to policymakers (especially monetary policymakers).

Considering the effects of the subprime mortgage crisis, monetary policymakers should make decisions aimed at regulating the amount of liquidity injected within the economy. For example, one of the ways that can be used to curb excessive lending is the implementation of lending laws (Elliot, 2009, p.8).

The US government through Fed failed in conducting its financial institution regulation role. Due to an increment in demand for investing in the housing sector, banks developed investment vehicles that could enable investors with low credit ratings to access finance. This led to the emergence of various types of subprime mortgages. This means that the threat associated with these assets was not given ample consideration. In addition, the government did not ensure optimal disclosure of the risks associated with the subprime mortgage instruments designed. This made a large number of institutional and individual investors consider investing in these instruments.

Prudential regulation within the financial sector in relation to the credit boom can play a significant role in curbing excessive credit growth hence reducing the risks associated with such boom. Due to the contagion effect, the UK housing industry was also affected by the occurrence of the US subprime mortgage crisis.

The subprime mortgage crisis also resulted from the existence of imbalances with regard to deposits and investments. These imbalances were instigated by the high rate of globalization. This led to the emergence of surpluses and deficits in the current account. The United States is one of the countries that had deficits. In order to sustain itself, the country relied on capital inflows from foreign countries. This had the effect of lowering both short and long-term rates of interest. Low rates of interest increased demand for finance among individuals whose credit rating is low.

Reference List

- Ayuso, J. & Robert, B. 2006. House prices and real interest rates in Spain. Journal of economics and statistics. Vol. 3, issue 4, pp. 1-36.

- Bhat, G. & Jayaraman, S. 2009. Information asymmetry around earnings announcements during the financial crisis. Washington: Olin School of Business.

- Dell’Ariccia, G., Igan, D. & Laeven, L. 2008. The US subprime mortgage crisis: a credit boom gone bad. New York: Vox.

- Demyanyk, Y. & Hemert, O. 2008. Understanding the subprime mortgage crisis. New York: New York University.

- Ding, M. & Li, H. 2009. On the market risk prevention of China commercial banks financial product under the financial crisis. International journal of business management. Vol. 4, issue 8, pp. 1-4.Changchun: School of Economics and Management, Changchun University of Science and Technology.

- Eickmeier, S. & Hofmann, B. 2009. Monetary policy, housing booms and financial imbalances. London: European Central Bank.

- Elliot, A. 2009. Fair banking: the road to redemption for the UK banks. London: CSFI.

- Fitzpatrick, T. & McQuinn, K. 2007. House prices and mortgage credit: empirical Evidence from Ireland. London: European Central Bank.

- Fratantoni, M. & Schuh, S. 2003. Monetary policy, housing, and heterogeneous regional markets. Journal of Money, Credit, and Banking. Vol. 35, pp. 557–589.

- Goetzmann, W. & Yen, J. 2009. The subprime crisis and house price appreciation. Colorado: University of Colorado.

- Gowland, D. 2007. Controlling the money supply. London: Billing and Sons Limited.

- Gramlich, E.M. 2007.Subprime mortgages: America’s latest boom and bust. London: Urban Institute.

- Hoffinger, B. 2009. US bank stocks and the subprime crisis: an event study in times of ad-hoc write-off announcement due to the subprime crisis. Norderstedt: Grin Verlag.

- Hongyu, L. & Yue, S. 2005.Housing prices and general economic conditions: an analysis of Chinese new dwelling market. Journal of economics. Vol. 10, issue 3, pp. 334-343. Tsinghua: Tsinghua Science and Technology.

- Jansen, L.H. & Linsmann, K. 2008. US subprime crisis: to what extent can you safeguard financial system risk. Norderstedt, Germany: Grin Verlag

- Kirk, E. 2007. The subprime mortgage crisis: an overview of the crisis and potential exposure. New York: Insurance Practice Group of Sedgwick.

- Leonard, T. M. 2007. Encyclopedia of the developing world. New Jersey: Butterworth-Heinemann.

- Mankiw, N.G. 2006. Essentials of economics. New York: Cengage Learning.

- Martin, C. & Milas, C. 2008. The subprime crisis and the UK monetary policy. Brunel: Brunel University Press.

- Montia, G. 2010. the UK banks are alleged to have mis-sold mortgage-backed securities. [Online].London: Banking Times.

- O’Connor, R.2O10. Subprime mortgages explained. [Online].

- Office of Deputy Prime Minister. 2003. The mortgage-backed securities market in the UK: overview and prospects. London: Office of Deputy Prime Minister.

- Otrok, M.D, & Negro, M. 2007. 99 Lufftballons: monetary policy and the house price boom across U.S states. Atlanta: Federal Reserve Bank.

- Poon, M. 2009. Accounting, organization and society. New York: Elsevier.

- Public Information Officer. 2000. Modern money mechanics: a workbook on bank reserves and deposit expansion. Chicago: Federal Reserve Bank of Chicago.

- Ryan, S. 2008. Accounting in and for the subprime crisis. New York: Stern School of Business.

- Sanders, A. 2008. The subprime crisis and its role in the financial crisis. Journal of housing economics. Vol. 17, pp. 254-261. Arizona: Arizona State University.

- Schwartz, S. 2009. Disclosure’s failure in the subprime mortgage crisis. Utah Law Review. Utah: University School of Law.

- Shijian, Z. 2008. When does Will US Subprime Mortgage Crisis end? Tsinghua: Tsinghua University.

- Swan, L.S.2009. The political economy of the subprime crisis: why subprime was so attractive to its creators. European Journal of political economy. Vol. 25, issue 23, pp. 124-132. New South Wales: Elsevier.

- Tong, H. 2008. Real effects of the subprime mortgage crisis: is it a demand or a finance shock. New York: International Monetary Fund.

- Tucker, M. 2008. The development and evolution of the subprime mortgages crisis. Journal of business and economic issues. Vol. 3, issue 2. pp. 1-10.

- Uhlig, H., 2005. What are the effects of monetary policy? Evidence from an agnostic identification procedure. Journal of Monetary Economics. Vol. 52, pp. 381–419.

- Whalen, R.C. 2008. The subprime crisis causes effects and consequences. Indiana: Networks Financial Institute.

- Whitehead, C. 2010. Competition, innovations and product regulation in the mortgage market: London: LSE.