Introduction

One of the most significant factors when deciding whether to invest in a certain country is the volatility of its currency. It has been argued that currency volatility is correlated with the volume of international trade. It is an intuitive conclusion since volatility raises risk. High volatility creates uncertainty and can lead to massive losses to a company that is especially doing a lot of importation. This paper will look at the feasibility of investing between two countries. The two countries that will be analyzed are the United States and Turkey. In this case, it will be assumed that the US is the source of the investment, while Turkey is the investment destination.

Why the United States and Turkey?

The US is the largest economy in the world, with its GDP accounting for about 16% percent of the world. The US is an economic and military powerhouse with a lot of influence around the world. The US possesses a special seat among the league of nations with veto power over international decisions (Siripurapu, 2020). Countries that have received sanctions from the US have ended up in ruin, unable to conduct business around the world. The US dollar is the most important currency in the world. The US Federal Reserve Bank was created in 1913 because of the unreliability of the currency system that existed at that time (Karmin, 2009). Moreover, the US economy had surpassed Britain as the world’s largest, but the British pound was still the world’s most important currency, with most transactions being carried out in it. Most countries still continue to peg their currencies to gold for stability.

Many countries quitted the gold standard after the World War I to pay their military expenses with paper money, this maneuver devalued their currencies. During three years of the the war, the British still used the Gold standard holding its position as the leading currency in the world (Karmin, 2009). The US would later become the lender of choice to lots of countries that wanted the dollar-dominated US bonds; this was the moment the dollar replaced the pound as the world’s leading currency. Just as in the World War I, the US started the World War II much later, serving as the proprietor of the Allies in supplies, weapons, and other goods getting paid in gold (Karmin, 2009). By the time the war was ending, the US had owned much of the world’s gold. The countries that had abandoned the gold standard wanted to return to the gold standard, and in 1944, after meeting in New Hampshire, the Allied countries chose to be linked with the US dollar which was linked to gold (Karmin, 2009). This is known as the Bretton Woods Agreement, where the countries agreed to maintain a fixed exchange rate among their currencies and the US dollar. In the present day, the USD dominates more than 61% of all foreign reserves. The reserves are usually in cash or US bonds. The USD also dominates an estimated 40% of the world’s debt (Karmin, 2009). This illustrates the might of the dollar and how it came to be the titan it is today.

Very few countries have captured the headlines over the past five years the way Turkey has concerning currency performance. In 2018, the country went through an economic crisis characterized by the country’s currency (Lira) slumping in value, increased inflation, high borrowing costs, and accompanying loan defaults. The situation had many angles first one being the country’s extreme current account deficit. The other angle was the vast amounts of private debt dominated in foreign currency. There was also a political and geopolitical angle with the president of Turkey, Recep Tayyip Erdogan, increasingly becoming more authoritarian and the US President Donald Trump’s administration becoming more hostile towards Turkey.

The US Dollar over the past 5 years

The past five years in the US have predominantly been Trump years. Following Trump’s victory in 2016, the dollar gained due to the expectation of increased interest rates and fiscal stimulus. In the year 2017, after immigration, the Trump Administration focused on immigration which slowed down the strengthening of the dollar (Fox, 2021). The Trump administration had also proposed adjustments to border taxes that had the impact of increasing the cost of imports. For Mexico, Trump had proposed a 20% tax on exports to the US to fund his proposed “border wall” with the country (Fox, 2021). Trump also engaged in the infamous trade war with China. His administration imposed tariffs and taxes on Chinese products for what he had termed as unfair trading practices, including the devaluation of their currency (Fox, 2021). In summary, Trump’s trade policies involved fiscal stimulus, higher inflation, high interest rates, and a strong dollar.

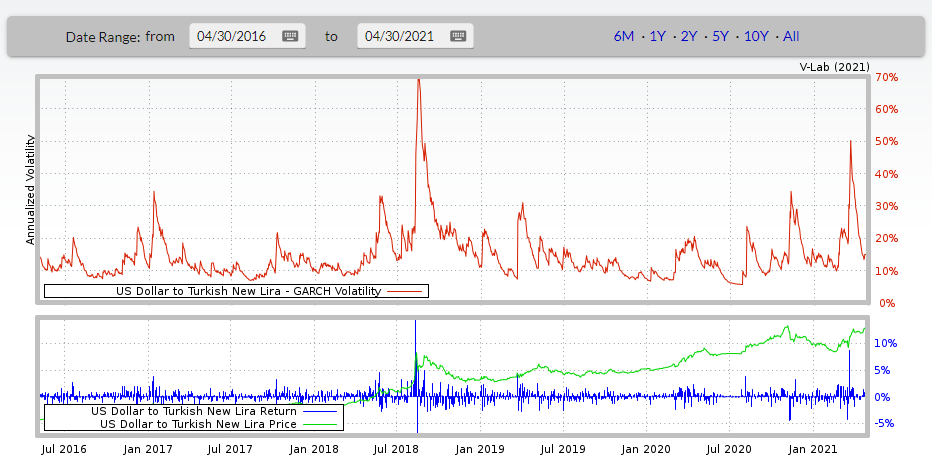

The above chart shows a 5-year USD/TRY chart from April 2016 to April 2020. From the chart, it is evident that the pair has been very volatile over the period. The most volatile season was in 2018 August, when the currency plunged by as much as 20% in a single day to a record low. This is just one snapshot of the downward spiral pattern that saw the currency drop to unimaginable lows. 3 Turkish lira could buy 1 USD in 2016, which has parabolically diminished to a 2021 value of about 8.3.

The above charts indicate a dramatic loss in the value of the Turkish lira. The volatility in the currency raises several potential problems, especially in the current context of globalization. The freefall could affect the operations and profitability of companies. The decline in the lira did not just pose a risk to multinationals operating in Turkey but also SMEs’ economic exposure. Transaction exposure would have affected companies that were making or receiving payments in USD, which would have made them receive lesser payment due to a devalued lira. The other type of risk is translation exposure which arises from companies that have subsidiaries in Turkey and has to make consolidated financial currencies.

Economics may not be as significant as the other two risks but is essential nonetheless. This type of risk would have resulted from the effect of currency fluctuations on a company’s cash flow; this risk is typically long-term in nature and can potentially compromise an organization’s competitive position substantially. An example of economic exposure is if a company is importing its goods and has to compete with local manufacturers; since they still need to be paid in lira, they would incur losses or get lesser stock when they convert back to USD.

Currency Risks Faced by the Multinational Company

Translation Exposure

One major risk faced by the multinational firm is translation exposure. Translation exposure is also referred to as accounting exposure. This risk measures the degree to which a company’s financial reports will be affected by fluctuating exchange rates. Since the company intends to invest the money in Turkey, it will establish a subsidiary in Turkey. It will need to translate all the financial accounts of all their subsidiaries in different countries into one report in one currency. These reports are called consolidated financial statements; all assets and liabilities in foreign countries must be converted to the parent company’s currency. In this scenario, the parent company is assumed to be American, and the subsidiary is being established in Turkey. In 2018, the lira dropped from 3.772 against the dollar to 6.52 by July. That is a huge decline in a span of 7 months; if the subsidiary had been established at the beginning of the year with £100 million being converted to the lira, by the time they would be reporting half-year results, the value of the subsidiary would have dropped to (3.772/6.52 x 100) = £57.8 million.

Transaction Exposure

Transaction exposure is an indicator of the change in the value of an outstanding financial obligation incurred prior to a change in the exchange rate but only due after the change. The transaction exposure will result from changes in cash flows that will stem from the outstanding financial obligation. For the multinational, the transactional exposure will be due to its contractual cash flows, i.e., receivables and payables whose values could be affected by unforeseen exchange rate changes resulting from a foreign currency-dominated contract. The multinational will be forced to exchange its dollars to lira to realize domestic its dollar-dominated cash flow value.

Operating Exposure

Operating exposure is also called economic exposure/ strategic exposure / competitive exposure. This is the measure in which a company’s value is affected by unanticipated fluctuations in the exchange rate. In this case, a subsidiary has been established in Turkey by American investors, but after a volatile session of the lira, the company’s value is greatly hit by the exchange rate. The adjustments in the exchange rate will have severe consequences on the company’s position with regard to its competitors, the future cash flows of the company, and ultimately, the value of the organization. Therefore, economic exposure can impact the current value of future cash flows. If a transaction is exposing the company to foreign exchange risk, it also exposes it economically. However, economic exposure can emanate from other business activities untreated to international transactions such as fixed asset cash flows. A change in the exchange rate in Turkey that impacts the demand for goods in the country would also expose the country economically.

Recommendations for Addressing Currency Risks

The best technique for managing translation risk is called balance sheet hedge. It involves multinational corporations participating in the forward market; this would help them gain some cash that would help offset some of the loss from exchange rate risk. The success of the process hinges on successful prediction in the prediction market, which is not easy to achieve. In balance sheet hedging, a company will place an equal amount of assets and liabilities in its balance sheet. If the strike rate is 100%, then there will be zero loss due to translation exposure (Butler, 2016). One of the limitations of this technique is an inaccurate forecast of earnings. The other limitation is inadequate forward contracts for some currencies, especially for small countries. It is unlikely that USD and lira would have shortages in this regard given the sizes of Turkey and USA economies. The other limitation is accounting distortions and increased transaction exposure.

On the other hand, transaction exposure results from contractual transactions affecting the receivables and payables of the multinational corporation. The dollar value can increase in the period causing the firm’s profit to be hit. The firm can consider hedging to offset these transaction risk exposures. There are various hedging techniques, such as forward market hedge, futures, money market hedging, and options market hedging. These methods will help the firm reduce the uncertainty from cash flows.

Currency risks are a great pitfall for multinationals and countries that must be checked to maintain stability in international markets. One way of addressing this issue is through risk-sharing agreements. These are contractual agreements in which the seller and the buyer agree to split the currency risk between each other (Butler, 2016). An example is if a Turkish importer imports American products every month, the buyer and the seller can agree that the payment will be based on the spot market value of the lira if it is between 8-8.5, but if it falls below that, both firms will split the loss. Another solution is cross-hedging which is used to reduce transaction exposure risk. It is used when a company’s receivables cannot be hedged. It is also referred to as proxy-hedge since the company has hedged a position in another currency serving as the proxy for which the multinational is exposed.

Another solution against currency risk is reinvoicing centers; a reinvoicing center is a department of the multinational corporation where centralization of a company’s transactions occurs and where the netting of foreign-currency receivables is done (Butler, 2016). Mechanisms of heeding the multinational company’s exposures are decided at the reinvoicing center. The station serves as the middleman between a parent company and its foreign subsidiaries. Another solution to currency risk exposure is government exchange risk guarantees which are arrangements for governments to absorb some of the risks. This is done through government agencies that provide businesses with insurance against export risks and particular financing schemes (Butler, 2016). These agencies will typically offer exchange risk insurance to exported n top of export credit guarantees. The exporter is expected to pay a small premium, and in turn, the agency absorbs the exchange rate risks.

Another recommendation for multinational investing in these countries is long-term forward contracts. These contracts specify the exchange rate at which a particular currency will be exchanged in the future. Most international banks routinely provide forward rates for up to five-year terms for some hard currencies (Butler, 2016). The lira may not be a hard currency, but the dollar is, and the company can hedge in the dollar. The long-term forward rate is typically a non-standardized over-the-counter contractor where a party agrees to purchase a particular currency from the other party at a specific rate in the future.

Testing the International Portfolio Diversification Theory

A portfolio’s risk is measured by the variance of its return compared to the market return’s variance. This ratio is referred to as the beta f the portfolio. If an investor raises the number of investments in their portfolio, the portfolio’s risk falls rapidly at first but asymptotically approaches the systematic risk level of the market. If a portfolio is fully diversified, it would have a portfolio of 1.0. A portfolio, therefore, has two components of risk: market risk(systematic) and individual security risk(unsystematic) (Butler, 2016). Diversification only reduces the individual risk but leaves the market risk.

Any portfolio’s foreign exchange risks can be reduced through international diversification, whether they be general or securities portfolios. Internationally diversified portfolios are created in a similar way domestically diversified portfolios are created. Internationally diversified portfolios are not any different because an investor will be attempting to combine assets not perfectly correlated in a bid to reduce the risk of the portfolio. Additionally, when the investor adds assets outside their home market (in this case, Turkey), assets that previously were unavailable to be included in the portfolio’s averages can then be combined into a bigger pool of potential investments.

In this scenario, the multinational corporation will be acquiring assets and securities in a different market than their home country; these assets and securities are likely to be lira-dominated. If the multinational company bought lira bonds in the secondary market, they would not be risky to the US-based multinational, since they are dominated in the parent company’s home currency (Butler, 2016). In this case, the parent company has acquired two types of assets: the denomination’s currency and the asset bought with the currency.

As an example, the company can invest $10 million in the Borsa Stock Exchange, Istanbul at the beginning of the year. The spot exchange rate of the lira in January is 8 lira per dollar. The ten million yields 80 million lira, which the company uses to acquire shares at the Borsa at the rate of 5 lira per share, which yields 16 million shares they intend to hold for a year. At the end of the year, they decide to sell the shares they have been holding, which have now appreciated to 6.25 lira per share. The shares have increased by 1.25 lira per share. The 16 million shares now have a gross value of 100 million lira. The Turkish lira are then converted back to USD at a spot rate of 8.2, amounting to 12.195 million dollars. The total proceeds of the deal amount to:

(12195121-10000000)/ 10000000 = 22%

Evidently, currency risk associated with international investment is a lot more complex than domestic risk because currency risk has to be factored in.

Conclusion

This paper focused on the risks associated with currency fluctuations and other FOREX risks. Two countries were chosen, namely the US and Turkey. The US was chosen because of its importance in the global market since most reserves are dollar-dominated, and most of the world’s debt is also dollar-dominated. Turkey was chosen because it is a vital country geopolitically because of its NATO membership and also being part of the Islamic world. Turkey’s currency has declined rapidly over the past five years because of various reasons such as domestic politics and geopolitics. The paper also looked at the risks in both countries over the past five years; for the US, an unorthodox event was happening with the Trump administration, while in Turkey, its currency was tumbling and hitting all-time lows, causing risks for businesses. The paper has also looked at the different types of currency risks and ways of mitigating them. In conclusion, it was also established that the international portfolio diversification theory could also be applied to this scenario.

References

Butler, K. C. (2016). Multinational finance: Evaluating opportunities, costs, and risks of multinational operations (Sixth edition). John Wiley & Sons, Inc.

Fox, M. (2021). Here’s how the stock market performed under President Donald Trump, and how it compares to previous administrations. Business Insider Africa. Web.

Karmin, C. (2009). Biography of the Dollar: How the mighty buck conquered the world and why it’s under siege (First edition). Three River Press.

Siripurapu, A. (2020). The dollar: The world’s currency. Council on Foreign Relations. Web.

US dollar to Turkish new lira garch volatility analysis. (n.d.). V-Lab. Web.

US Dollar Turkish Lira. (n.d.). Investing.Com. Web.