The exchange rate can be defined as the currency of a given country expressed in terms of another country’s currency. The changes in the exchange rate affect the profits made by international trading partners and multinational corporations. The exchange rate also affects the value of investments as held by a given individual. The relative rate at which the exchange rate or the prices of securities change is referred to as exchange rate volatility. The volatility is high when the prices change faster and low when the prices change slowly over a selected period. Exchange rate volatility affects the price stability, the profitability of a given organization and the financial stability of a given country. There are many factors that affect the volatility of the exchange rate. These exchange rates are mostly expressed in terms of models which define exchange rate as being a function of set macroeconomic conditions. These factors are subject to a lot of research and finding the exact determinants of volatility are subject to numerous researches and debate (Bergsten and Williamson, 2003). These macroeconomic conditions encompass prices, government policies, government debt, productivity differentials and foreign assets. Most of the models in the past have indicated that exchange rate volatility is mostly affected by the movement in the macroeconomic environment as well as other factors (Claudio, 2007). Some of the main factors that control the movement of exchange rate are:

Inflation differentials.

Interest rate differentials.

Public debt.

Current account deficits.

The economic and political climate of a given country.

Import /export rations or balance of payments.

Speculation.

Competitiveness.

Inflation differentials

The inflation levels of a country affect the exchange rate movements. From literature, it has been observed that countries with minimal inflation rates have their currency values rising over time as their purchasing power increases as compared to other currencies. For example, if the rate of inflation in Saudi Arabia is lower as compared to other countries, it will become more competitive and this will increase the demand for their currency. Naturally, countries that have low inflation rates experience a general increase in the value of their currency as compared to countries with high inflation rates. Some countries with low inflation rates include Japan, Germany, Switzerland, the US and Canada. On the other hand, nations that have very high inflation rates tend to experience depreciating current prices and high-interest rates.

Interest rate differentials

Research has shown that interest rates, inflation and the exchange rate are correlated to each other. By controlling the interest rate, the exchange rate can be manipulated. The central bank controls the interest rates. When the central bank raises the interest rate, the country is able to attract foreign investors and the availability of capital and this results in to increase in the exchange rate. Thus, the central bank can control the exchanges rate by raising the interest rate. However, this only works if the impact of the high-interest rate is not mitigated by an increase in the inflation rate which would definitely drive the exchange rate downwards. Conversely, the exchange rates tend to decrease as the interest rate reduces.

Public debt

Public debt results when a country borrows money for the purpose of economic development and public sector projects such as infrastructural development. These projects stimulate the local economy but on the other hand, result in high inflation rates as the debt must be paid through taxes. High inflation results in a reduction in foreign investments and this ultimately drive the exchange rate downwards. When the debt is too high, the government may print money but this will also drive inflation much higher. The government may also sell bonds and other securities but foreigners may opt not to buy these securities because there is an impending risk if the country defaults to pay the loan.

Current account deficit

The current account deficit represents the balance of trade between a nation and its trading partners. It shows all the payments of a countries goods, services, interests and dividends. The current account deficit occurs when a country spends more on imports than exports. This means that the country must borrow from its foreign investors so as to make up for the resulting deficit. The demand for foreign currency lowers the country exchange rate to a level where the countries products are cheap enough to enable the foreigners to buy more so that the deficit is balanced. The current account deficit also results in the lowering of the exchange rate and this makes foreign products more expensive consequently discouraging importation but promoting the domestic market.

Economic and political climate of a given country

Most foreign investors look for countries with strong economic and stable political systems. This means that a country with good economic performance will attract foreign investors and this will subsequently result in a high exchange rate. Also, countries with a stable political system tend to attract foreign investors and this results in to increase in the exchange rate. Conversely, a deteriorating political and economic system attracts less foreign investments and this ultimately results in a reduction in foreign investments.

Balance of payment

When a country has high imports as compared to exports, a deficit on the current account occurs. The current account deficit is balanced by a surplus in the capital or financial accounts or it can be sourced from foreign sources. If it is financed from capital accounts then this affects the exchange rate. When a countries export market increases, favorable terms of trade result and this increases the exchange rate. When a country has less revenue from exports as compared to the amount spent on imports, unfavorable terms of trade exist and this results in a reduction in the exchange rate and fewer trading partners.

Strength of other currencies

The relative strength of other currencies affects the exchange rate movement. A typical scenario is the Japanese Yen and the Swiss franc whose value rose in 2010 and 2012 because the investors worry that the currencies of the European Union and the United States were fluctuating. It can be seen that, even though there was a low-interest rate and growth rate in Japan, the yen appreciated. This is because it was more stable as compared to the strengths of the other currencies.

Competitiveness

Shifts in the competitiveness of products in a given country also affect the volatility of the exchange rate. When products from a given country become competitive, the exchange rate rises as more products are exported. This would definitely result to a favorable balance of payment if the country imports less. Conversely, reduced competitiveness of a country’s product reduces the exchange rate. For example, in the year 2007 to 2009, the sterling pound value fell due to reduced competitiveness, the large UK current account deficit, and the recessions that hit the economy. The UK bank’s intervention was to increase the money supply and this raised speculation of future inflation and subsequently, the UK bonds became unattractive.

Speculative tendencies

Speculation has been shown to cause movement in the exchange rate. If speculators believe that the dollar price will increase, they tend to demand more of the currency and this will definitely drive prices upwards. If speculators believe that a given currency will fall, then, they tend to demand less and its exchange rate falls (Economics help, 2012).

Models Used to Study the Exchange Rate Movement

Forecasting of the exchange rate is done through the development of economic models which study and show the movement of the exchange rate as a function of several independent variables. Various models have been put forward in order to study the movement of the exchange rate. The convectional empirical literature classifies the different exchange theories into different classes. One of the groups of the classification of these models into three different types are the partial equilibriums model, the general equilibrium model and the disequilibrium model. In this classification the first group is the partial equilibrium models which encompass:

Relative PPP and the absolute PPP: these two take into account the goods in the market.

Covered Interest Rate Parity (CIRP) and Uncovered Interest Rate Parity: these two consider the assets in the market.

The external equilibrium model: the balance of payment affects the exchange rate.

The General rate equilibrium model has the following models:

Mundell- fleming model: This model takes into account the micro-economic aspects, money markets and goods market as well as balance of payments.

Balassa-Samuelson model: this model maximizes the profits that a firm gets.

Redux model: Pricing to the market: this model is created so as to emphasize the maximization of the consumer utility.

Simple monetary model.

Dornbusch model: this combines the monetary equilibrium with adjustments in price and output so as to achieve the equilibrium.

The third group is the hybrid models which are a combination of both the two models.

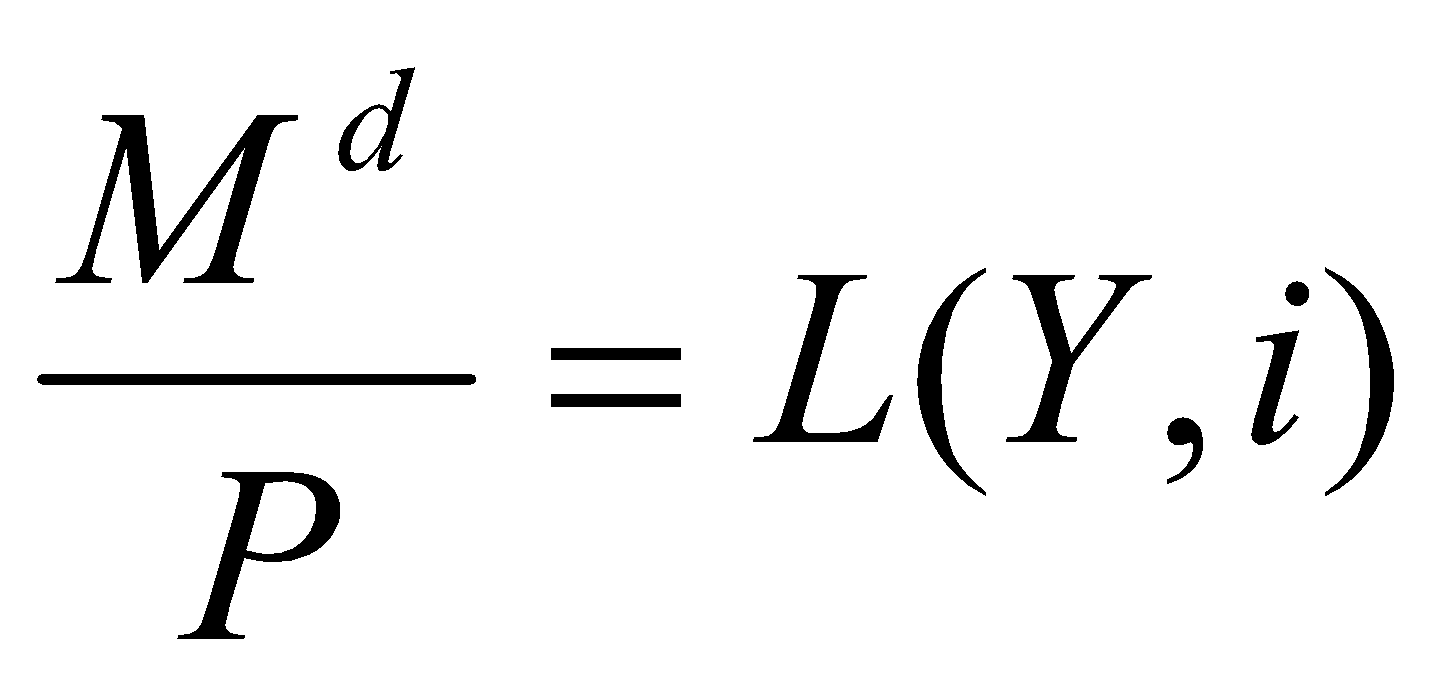

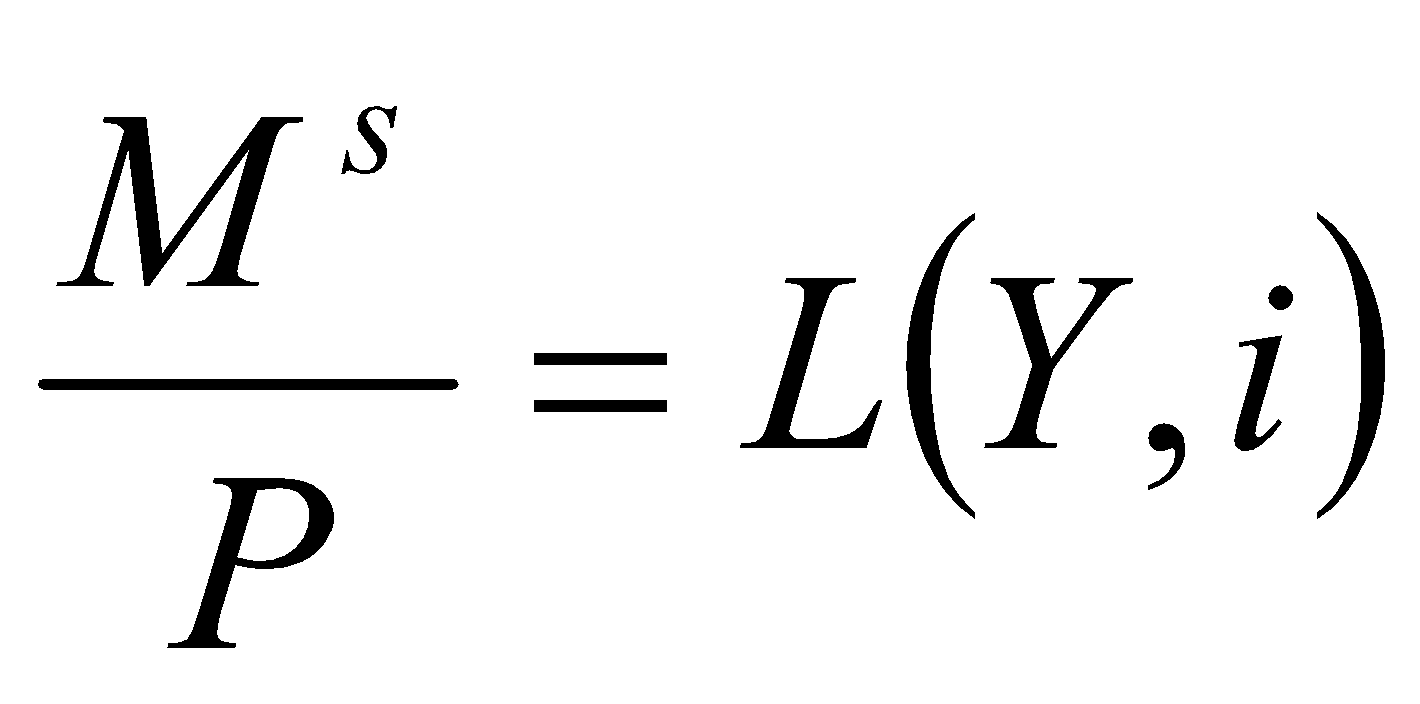

Purchasing Power Parity (PPP)

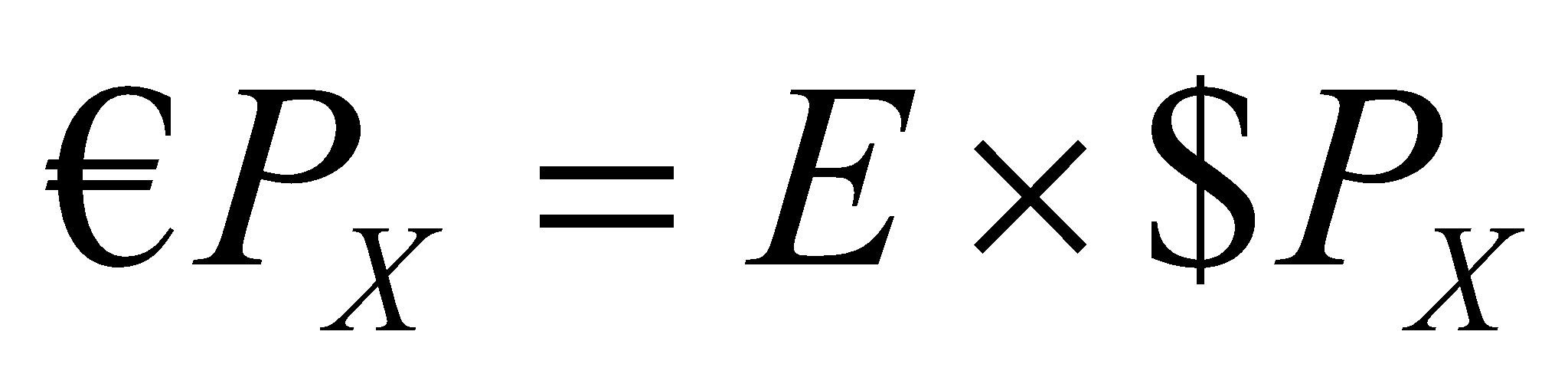

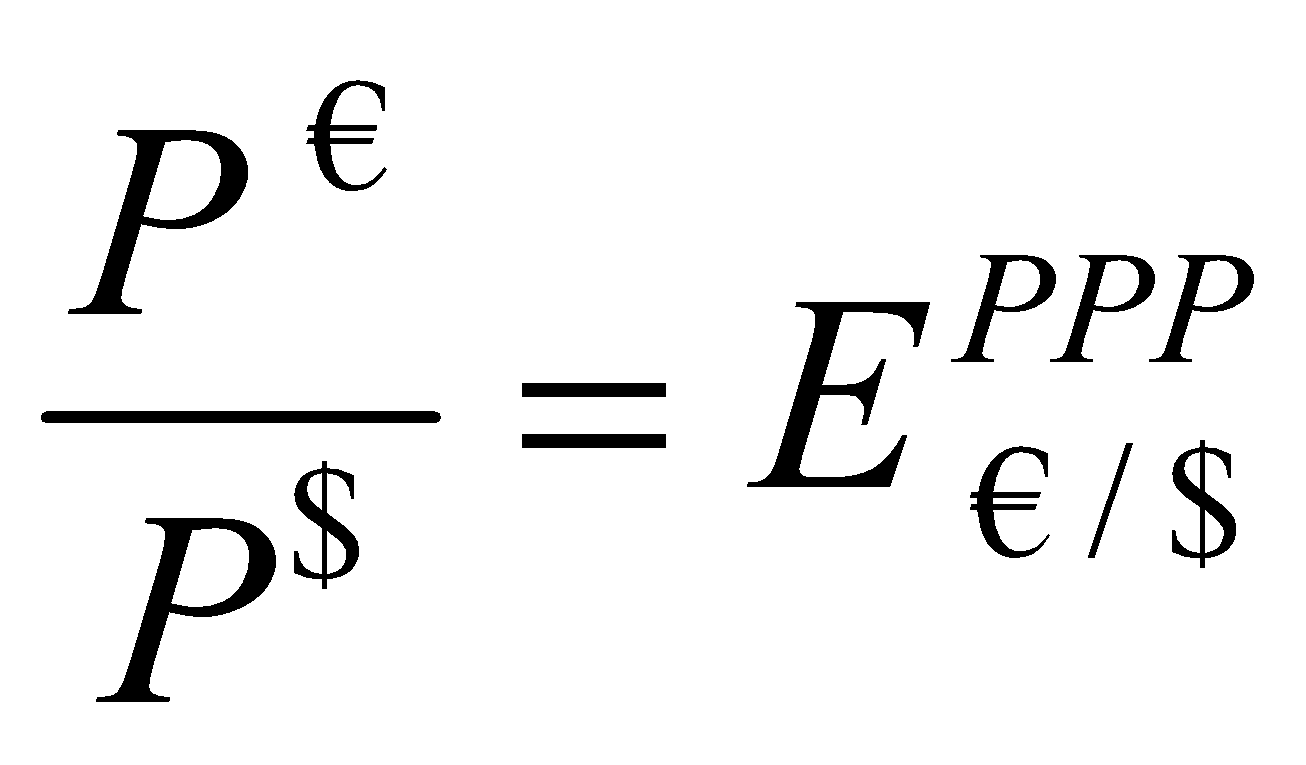

This is a model that allows the determination of the currency value by estimating the number of adjustments required so as to make exchange be equivalent to the purchasing power of the currency (Genberg, 1978). The PPP model is developed such that the price of a given product is the same in two different countries. PPP is a ratio that indicates the comparative prices differs across two countries for a given product or group of products (Nguyen, 2005). In this model, if $ PX is the price of a commodity x in a country like the USA and the price of the same commodity in UK is PX , the law of one prices means

(1)

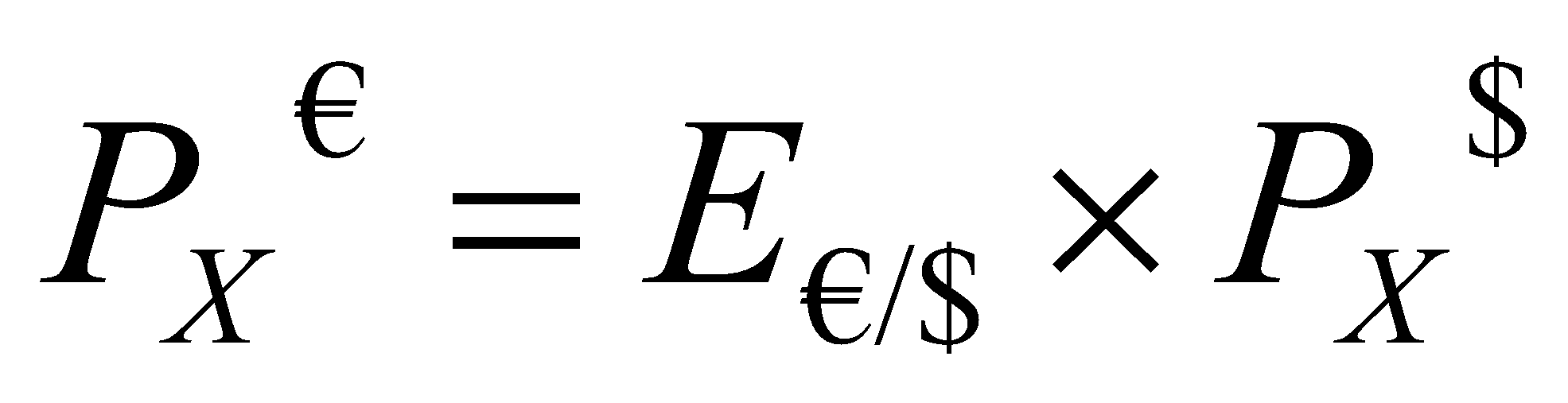

Where, E is the exchange rate between the sterling pound and the dollar. If the prices were expressed in terms of the consumer price index (CPI), the relative prices can be compared as follows

(2)

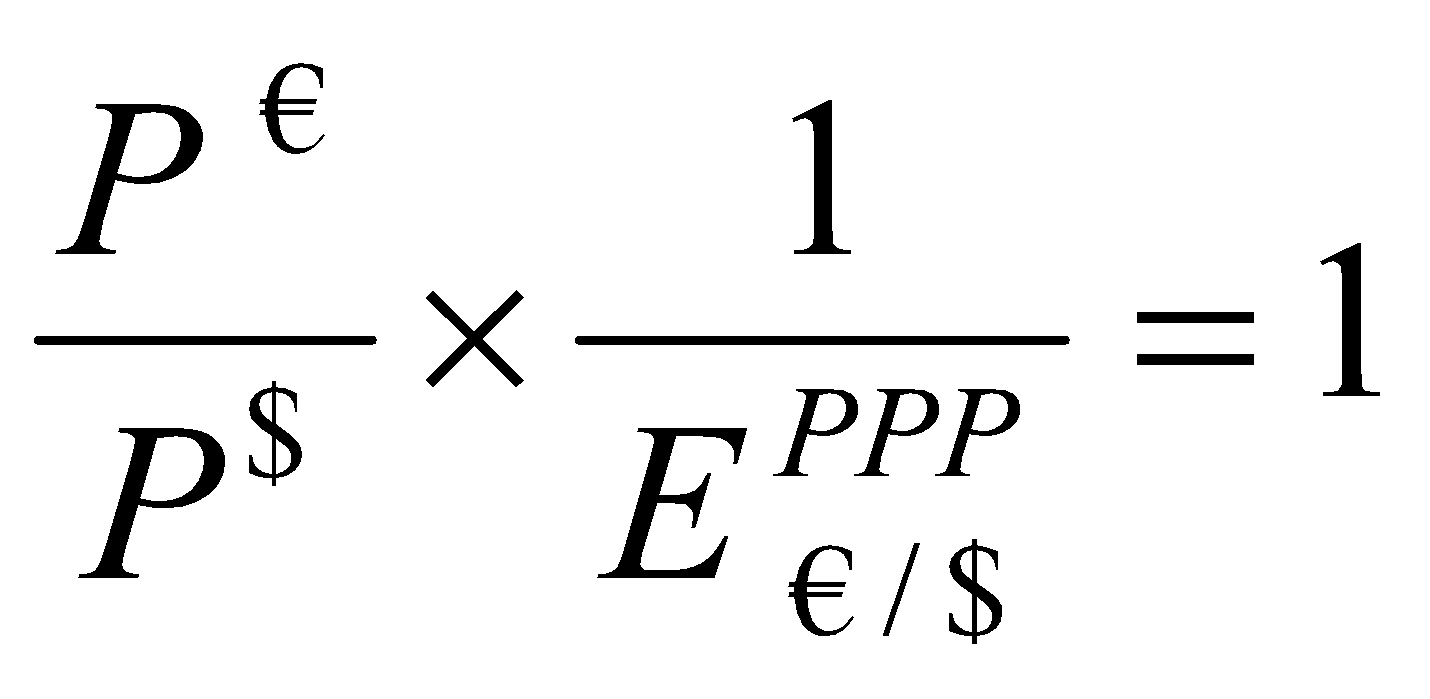

Where E €/S is the exchange rate between the Euro and the Dollar. If this equation is true, then the equation for absolute PPP becomes:

(3)

This equation can be written as

(4)

The left side of the equation 4 represent the real exchange rate that has been adjusted based on the pricing levels. For the absolute PPP to hold very strict definition of the goods must be given but this is not possible as the prices of goods vary with composition and weight. Also, the cost of transportation, insurance, taxes and tariffs, warehousing present some difficulties when using the absolute PPP.

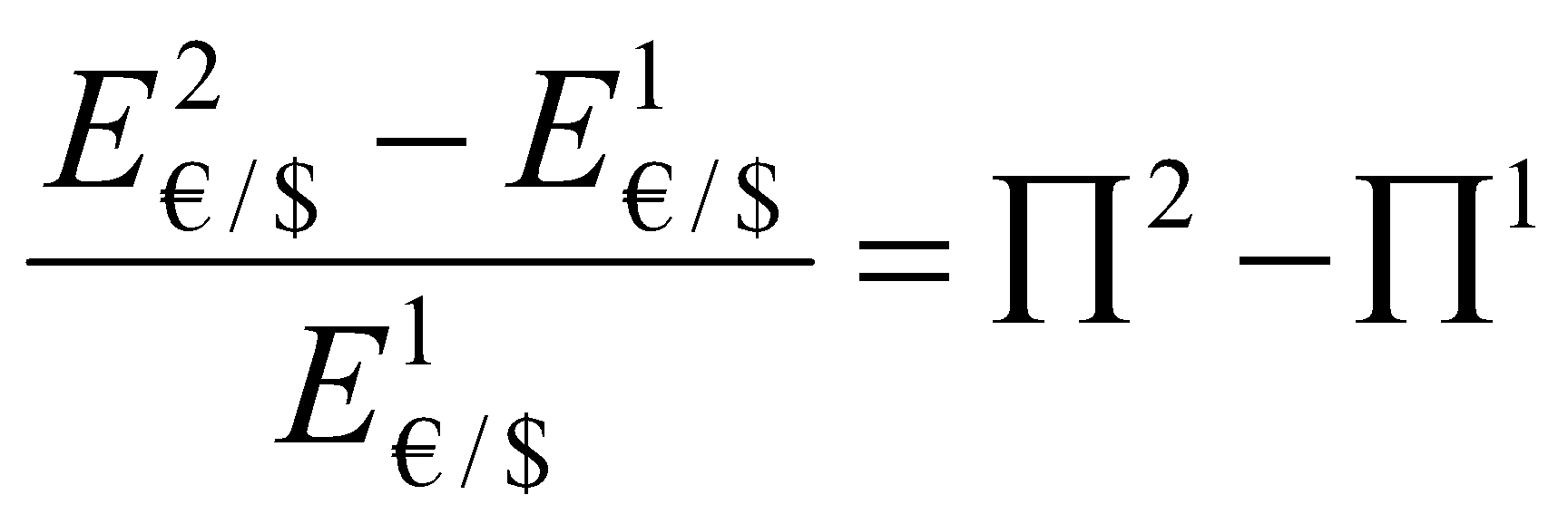

Relative PPP

This offers an alternative to the absolute PPP. Relative PPP takes into account the fluctuating price levels and changes in the exchange rate. The main influence to the relative exchange rate is inflation which has a direct impact on the exchange rate levels. The relative PPP is mathematically expressed as

(5)

Where Π² is the current inflation rate while Π¹ is the previous inflation rate. Thus the relative PPP change is dependent on changes in the inflation. Thus it can be seen that the exchange rate in this model depends on the prices of commodities and the inflation rate.

Covered interest rate parity (CIRP)

The interest rate parity theory is used to analyze the relationship between spot rate and the future rate of a given currency. According to CIRP, the different interest rates of two nations are balanced by the exchange rate forward premiums. This means that the spot or forward currency premiums are used to offset the differentials within two countries.

For example, if China is the home country and the foreign currency is the USA. Suppose the nominal interest rate at a time t in China is it while the same rate is it*. Further, the spot exchange rate is St while the forward exchanges rate at t+1 is St+1. Suppose the investor makes a deposit of 1 Yuan in china, he will get a return of it after a time equal to t+1 and hence the total including the principle is 1+it. Suppose the investor exchanges the Yuan for a dollar which has an interest rate of it* then the sum of the principal and the interest can be given by (1+it*)/St. Because the forward change rate is St+1 the principle in term of Yuan is (1+it*)St+1/St. . In a competitive market, it is expected that the return of depositing the Chinese yuan should be equal to the return for depositing the dollar. This is expressed as

(6)

This can also be expressed as

(7)

Mundell –Fleming method

The Mundell –Fleming method is developed as an extension of the ISLM model. In turn, the IS-LM model considers the market of goods, money and assets. The model can be used to study the monetary and fiscal policy. These two policies impact on the exchange rate. The link between goods and the money market can be described using the IS-LM model. In the Mundell – Fleming model, another component that is considered is the balance of payment. In total the Mundell –Fleming considers the money market, the goods market and the international payments.

By definition the goods market equilibrium is expressed as an IS curve

(8)

Where:

Y is the domestic national income.

C=C(Y) is the consumption. Further, consumption is affected by income and is hence a function of it.

G-is the spending by the government.

X=X(Y*q) represents the exports which depends on the foreign national income and the real exchange rate.

M=M(Y, q) represents the imports which is a function of the domestic income and a decreasing of the real exchange rate.

The money market equilibrium is determined using the LM curve. It is assumed that

The money market equilibrium can be expressed as:

The external equilibrium can therefore be expressed as shown in the equation below:

BP=CA+KA=0 where CA is the current account and KA is the capital account CA=PX-SP * M

And KA=K (i-i*-ΔSs)

The mundell-flemming method assumes that a state of perfect capital mobility, fixed exchange rate and monetary policy independence cannot be achieved at the same time.

Exchange rate and productivity – the Balassa – Samuelson model

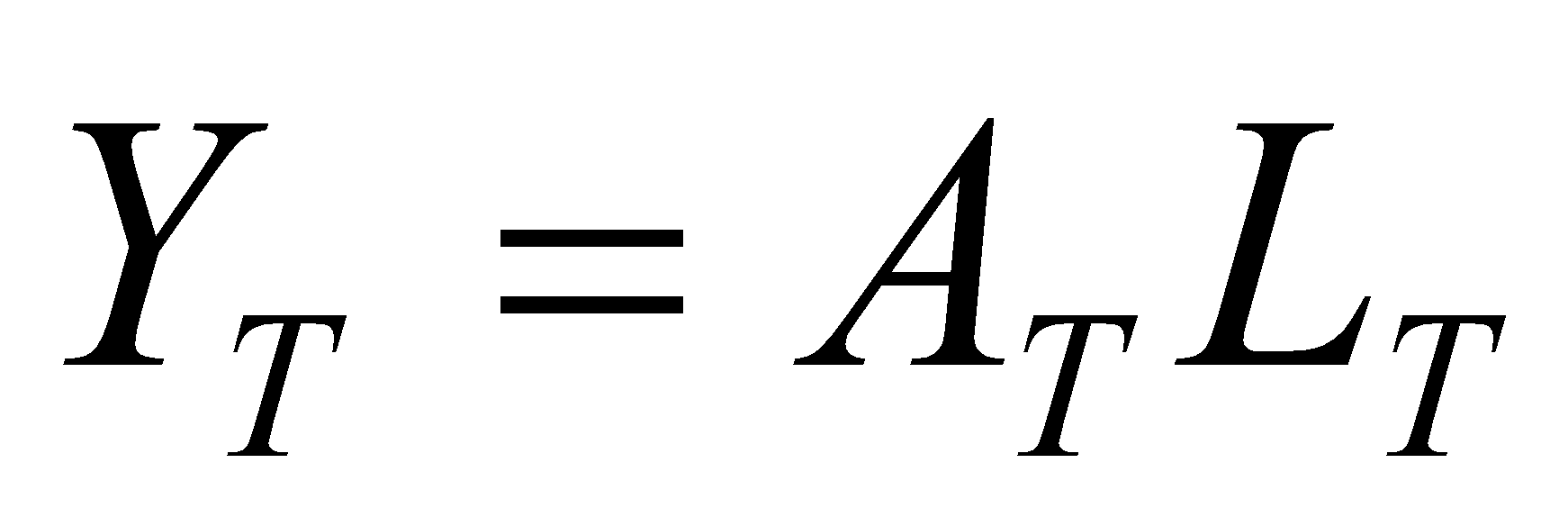

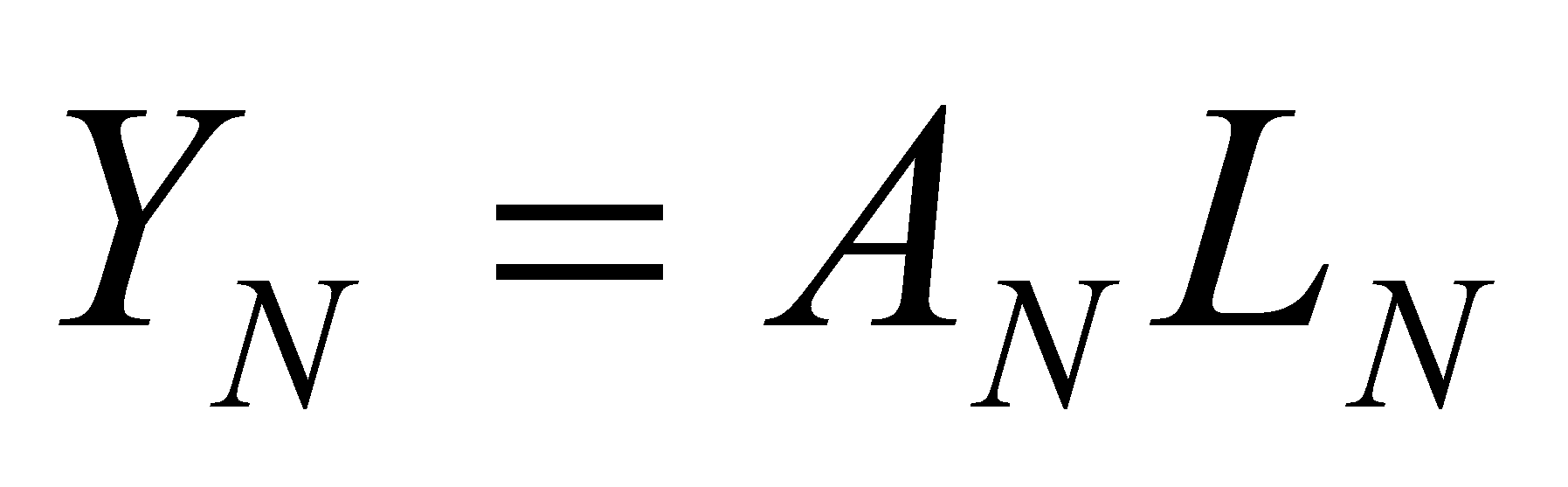

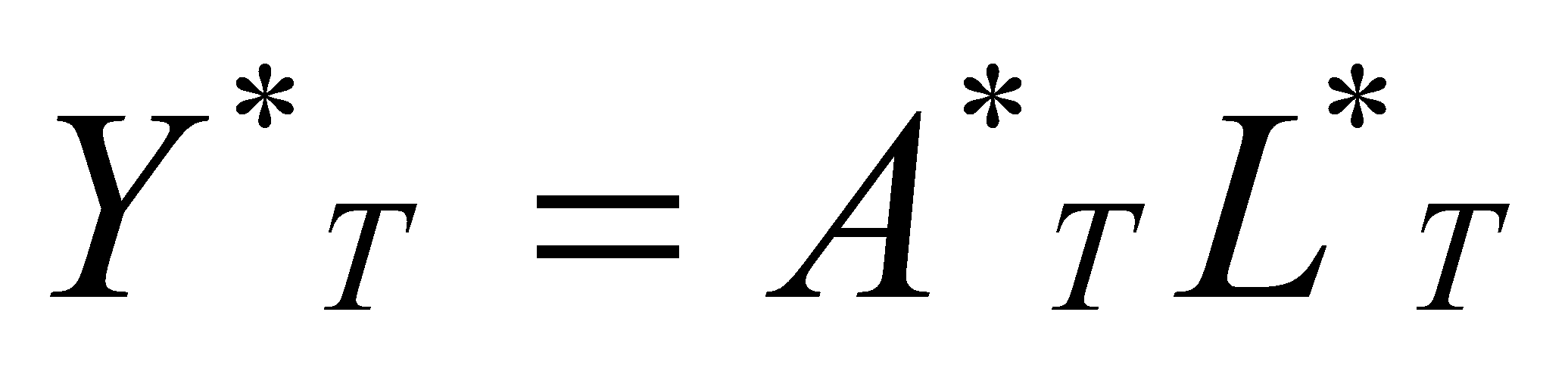

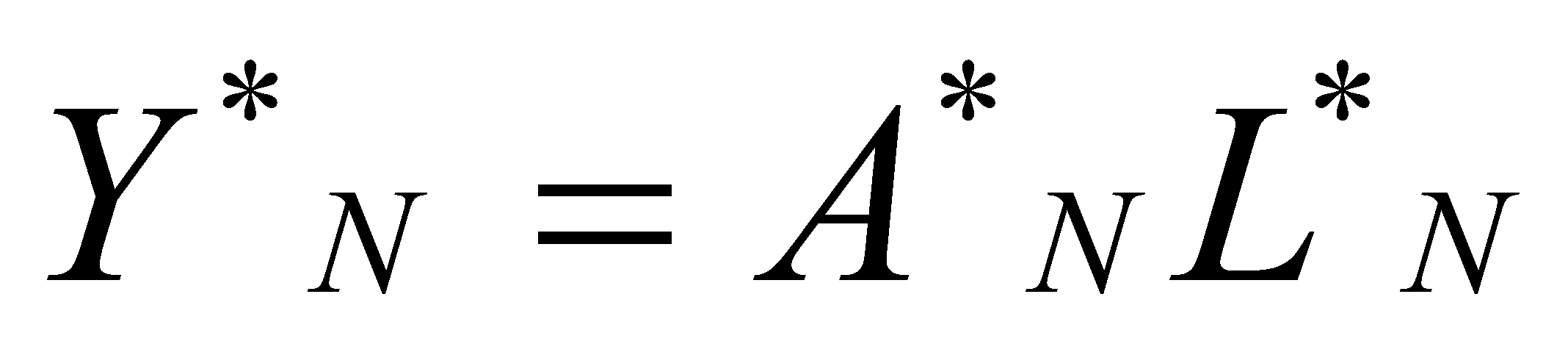

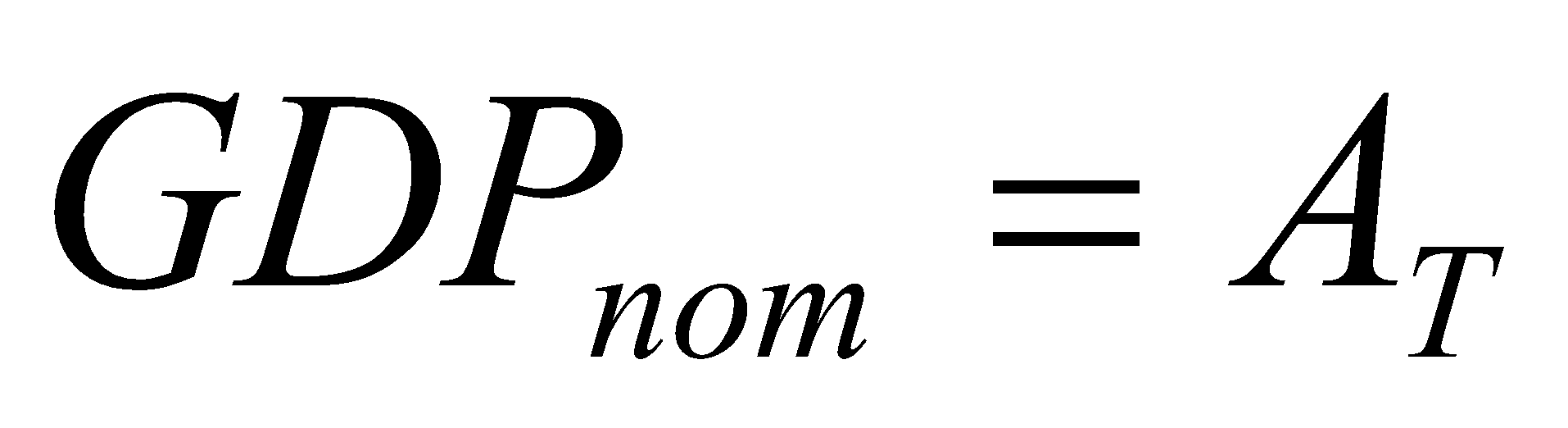

The PPP and the CIRP models only express partial equilibriums. The two models don’t relate the behaviors of the producer and the consumer. It can howver be argued that the price in a perfect market is determined by the forces of supply and demand. It is therefore necessary to determine the behavior of the consumer and the producer during the determination of the exchange rate. However, these are associated with the microeconomic aspects of a business Balassa, 1964; Samuelson, 1964). Using this model, the production function of tradable and non tradable goods can be represented by:

;

;

;

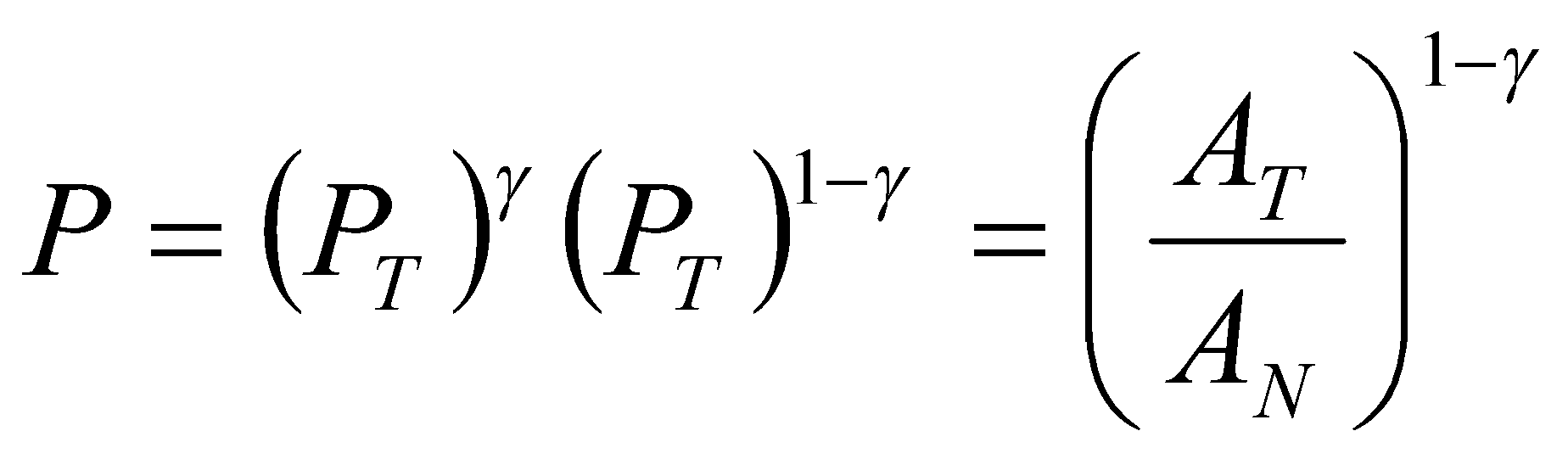

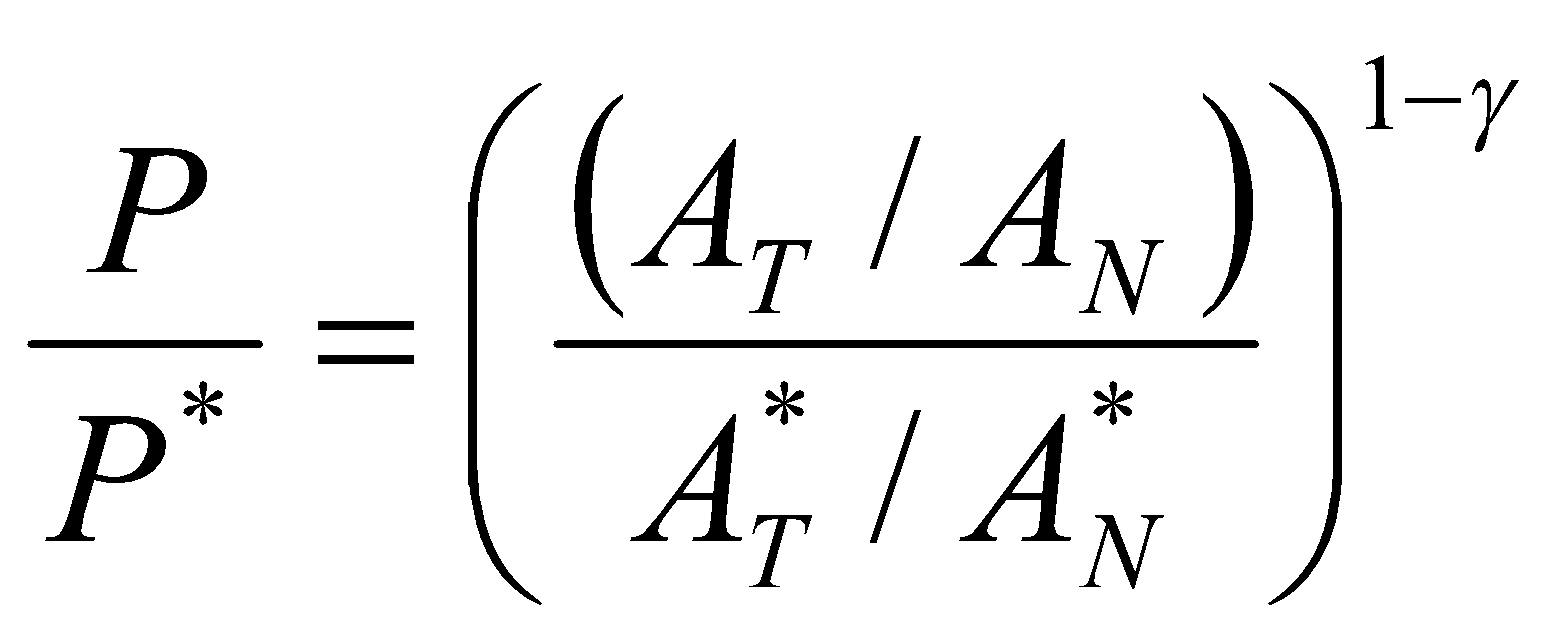

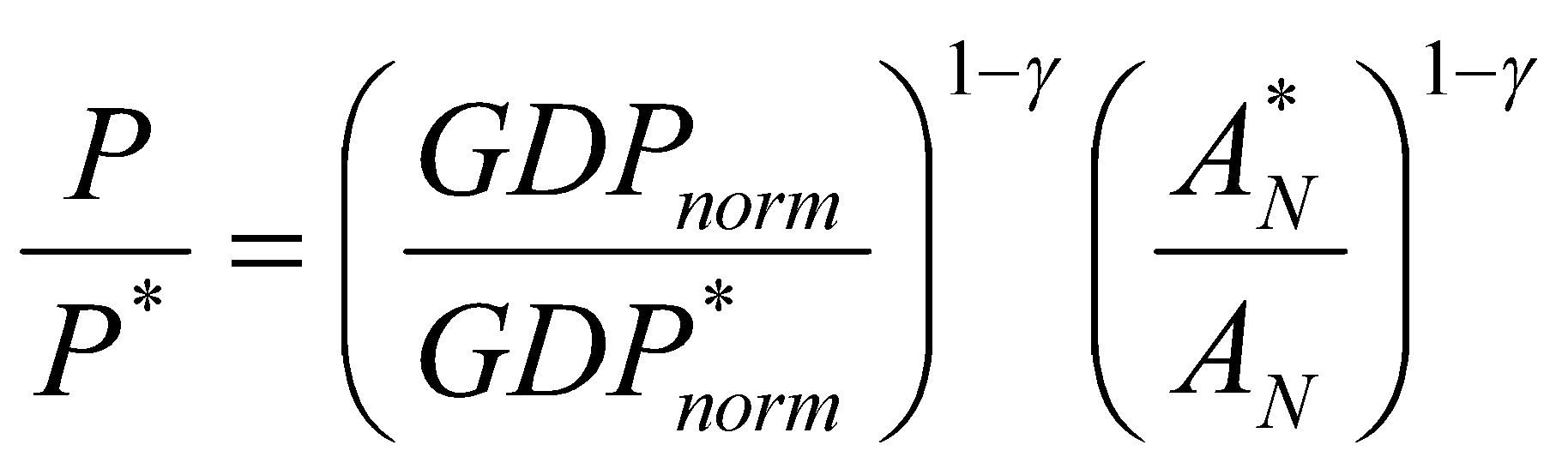

Where Y is the production, A represent technology and L represent labor, N represent non tradable sector, T represents tradable sector. The foreign market has the same representation but differs and is represented by the same parameters with a *. The model assumes that one price hold for different commodities and the labor mobility is zero. The price index can be calculated using:

Where ϒ represents the amount of tradable goods in the output. To determine the price at given country as compared to those of the trading partner, the following equation is used.

The GDP per every employee is given by

The relative prices can then be given as

In this model, the relative prices are affected by the GDP and the productivity level of the two economies. The exchange rate increase when the home country has a high GDP growth rate. Also, an increase in productivity of non tradable in the home country as compared to the foreign country will result to a reduction in the real exchange rate (Obstfeld & Kenneth, 2000). The current model can be improved so as to factor in labor and capital. The resulting equation is shown below:

,

Where K represents the capital.

Based on the B-S model indicates that there will be growth if the productivity –growth of the tradable exceed the productivity of the non- tradable. The model indicates that countries with high productivity in the tradable as compared to the non tradable will attain high price levels. This is because the high productivity gains allow the wages to rise and because the wages relate the tradable and non tradable sectors, it is expected that the economy will attain a given price level. The model has some shortcoming such as the assumption that the price of products at home is the same as those abroad, also the method of determining the prices still remain unknown since the model does not incorporate demand and lastly the model does no how the market prices are determined because it does not factor the demand and consumer behavior. The model does also not include the role of money (Rogoff, 2003). In conclusion the model partly determines the real exchange rate value.

Dornbusch Overshooting Model

A lot of literature show that the law of one price correlates with the normal exchange rate (Giovannini, 1988). It has been shown that the real exchange rate change less when the nominal exchange rates are fixed (Mussa, 1986). This necessities the extension of the exchange rate monetary model (Dornbusch, 1976 and Rogoff, 2002)

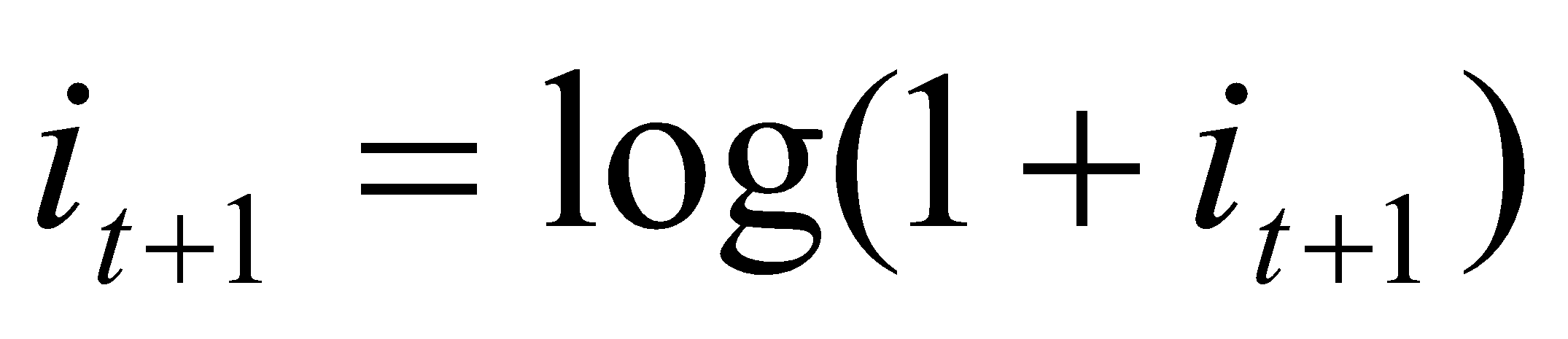

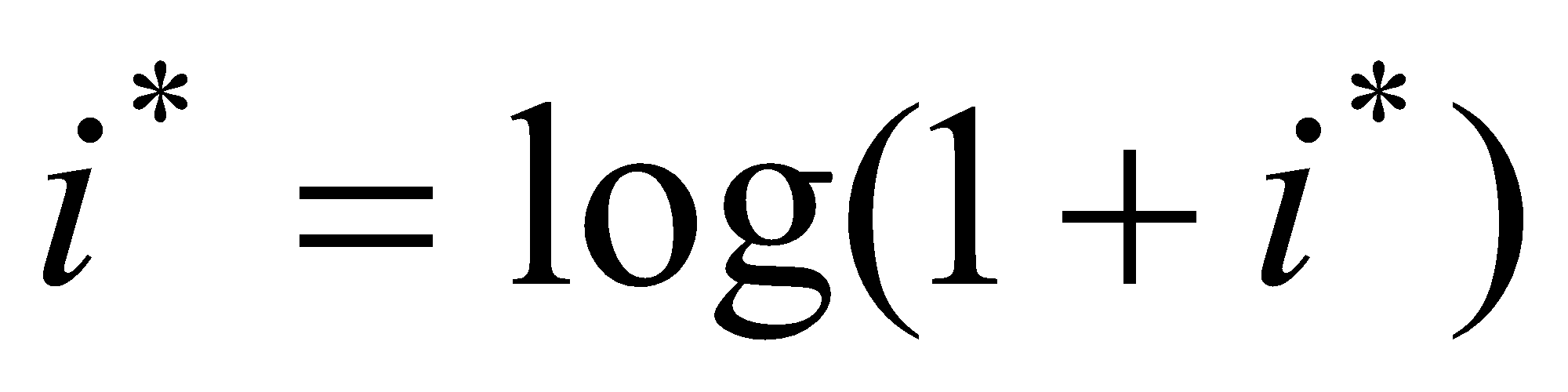

Under the dornbusch model, the uncovered interest rate parity and the monetary model are retained. Sticky prices are used as instead of having varying prices. The first condition of the of this model is the money equilibrium which is represented as:

Where M is the monetary supply, P is the domestic price level, γ is the domestic output, η and φ are the positive parameters. In this model, it can be seen that the opportunity costs of holding the money increase with high interest rates. Subsequently, the demand for money reduces. Also the price levels affect money demand. The second condition is the uncovered interest rate parity which is expressed as:

Where e is the logarithm of the exchange rate ye denotes the market expectation at a time:

With regard to the uncovered interest rate parity, the interest rate at home must be equal to the foreign. The Dornbusch model assumes that the prices are sticky and cannot be adjusted immediately.

Capital budgeting in corporations

One of the most imperative decision made by a manager is capital budgeting. To maximize on the wealth of shareholders, a manager must evaluate all the projects and investment opportunities so as to select the best. There has been an observation that most of the methods selected and used are not in line with the academician point of view. According to studies done by Ryan (2002), the methods different managers use during capital budgeting differ and are not consistent with what is taught by the academicians. Capital budgeting decisions for the fortune 1000 companies is done through the use of method such as the Net Present Value (NPV), the Internal Rate of Return (IRR) and the payback method. A study was done to determine the most preferred method of capital budgeting in the fortune 1000 companies (Ryan, 2002).

According to research done by Miller (1960), Schall, Sundam and Geijsbeek (1978) and Pike (1996), the most preferred method of capital budgeting was the payback method while the internal rate of return was shown as the most preferred by some researcher. Interestingly, these studies show that the NPV is the least preferred method as compared to the others. One common observation is that these studies were done before computer and information technology became more sophisticated. Klammer (1972), on the other hand, shows that the internal rate of return is the most preferred method. In the past, most of the researchers who analyzed the usage of the different capital budgeting techniques found out that the least preferred method of capital budgeting was the profitability index. These researches were done between 1970 and 1983. Also, studies were done by Jog and Srivastava (1995) and Pike (1996) show that there has been a reduction in the use of the internal rate of return in the United Kingdom and Canada. In all the research done, NPV trails among all the other methods. In the past, managers have considered that the use of IRR is a better method as compared to NPV. Managers view IRR as more efficient when it comes to comparison as compared to the NPV (Evans and Forbes, 1993). The current research however shows that managers are moving towards NPV as their preferred choice. This presents contradictions as past managers preferred IRR to NPV. However, the academicians believe that NPV is superior as compared to the IRR method.

It has been observed that for mutually exclusive projects, the NPV method assumes that all the cash flows got are invested at the cost of capital. On the other hand, IRR assumes that all the intermediate cash flows are put back to the business at the IRR rate, which is higher than the capital cost (Ryan, 2002). NPV method is also not sensitive to the multiple changes in the cash flows (Ryan, 2002).

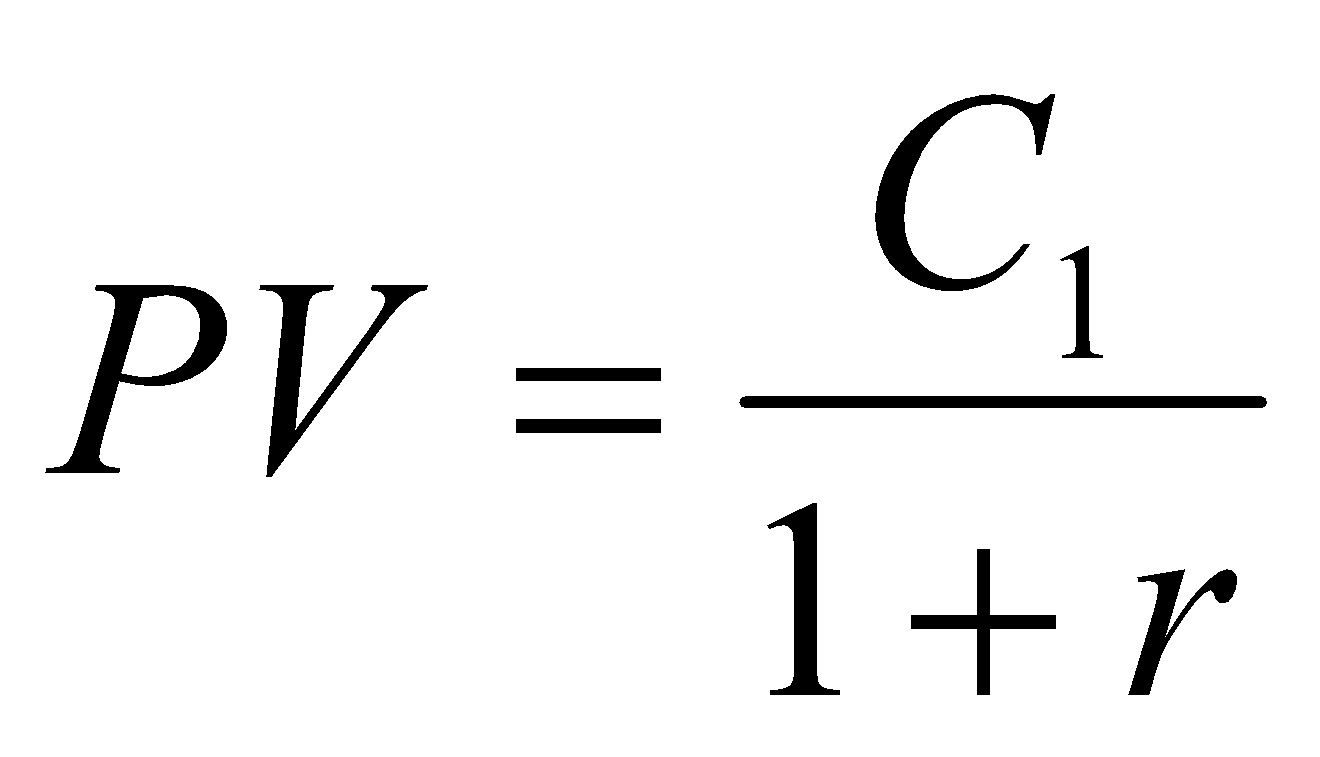

Net present value method (NPV)

The NPV or the Net Present Worth compares the money at the current day with money in the future. It shows the relation of money today with the same amount tomorrow. The net cash inflows and the net cash outflows are compared. It compares the present value of money today with the value of money in the future. The present value represents the amount of money that should be put in alternate investment so as to obtain an expected amount after some years. The method also takes into account the value of money in the future. The method is used in capital budgeting and to make other economic, financial and accounting decisions.The general formula for the NPV method is:

Where:

PV is the present value.

C1: is the cash flow at the beginning.

R: is the discount rate.

Internal Rate of Return

This is a capital budgeting method where the net present values of all cash flows of a given project are made equal to zero. It is one of the discounted flow technique used in capital budgeting method. The IRR is the interest rate at which the NPV of all the positive and negative cash flows is equal to zero. It is used to measure and compare different alternatives that a company has and to determine the most profitable venture in which the company can adapt. The project with the highest IRR is considered as the best for the company to invest in. it is also referred to as the economic rate of return.

The formula for IRR is

Payback method

The payback period can be defined as the period of time that a project or an investment takes so as to return the money that the company invested in the project. When a company invests in a given project, they pay a significant amount of money as capital. After completion of the project or an investment, it is expected to generate money, that is, the cash inflows. If the annual cash inflows are high, then the project will recover the initial cost much faster. However, if the initial costs are lower, then the project will recover the initial cost much slower. The time taken to recover the initial cost is the payback time. Projects with a small payback period are more favorable than those with a high payback period. The payback period can be computed using:

Payback period =Amount invested /annual cash inflows

Even though the payback method is a simple method of determining the attractiveness of a given project, it does not factor into consideration the time value of money. This is a principal disadvantage of the method. Other than the time value of money, the payback method does not take into consideration other factors such as the excepted project life and it only measures the time required to recover the original amount.

In conclusion, there are various capital budgeting methods used by various multinational corporations. In the past, the managers relied on the use of IRR and the NPV, however, the IRR method was highly recommended as compared to the use of NPV. According to the research that was done by Ryan (2002) on the preferred capital budgeting method, it was shown that the NPV method was the most preferred method as opposed to the IRR method. Both the IRR and NPV were ranked higher as compared to all other methods.

References

Balassa, B 1964, “The Purchasing Power Parity Doctrine: A Reappraisal,” Journal of Political Economy, vol. 72 no.1, pp. 584-596.

Bergsten, C and Williamson, J 2003, Dollar Adjustment: How Far? Against What?, Institute for International Economics, Washington.

Claudio, M 2007, On the macroeconomic causes of exchange rates volatility International Centre for Economic Research, Torino.

Dornbusch, R 1976, “Expectations and Exchange Rate Dynamics”, Journal of Political Economy, vol. 84, pp. 1161–76.

Evans, D and Forbes, S 1993, “Decision Making and Display Methods: The Case of Prescription and Practice in Capital Budgeting,” The Engineering Economist, vol. 39 no. 1, pp. 87-92.

Genberg, H 1978, “Purchasing Power Parity under Fixed and Flexible Exchange Rate,” Journal of International Economics, vol. 8, pp. 247–76.

Giovannini, 1988, “Exchange Rates and Traded Goods Prices,” Journal of International Economics, vol.24 no.1, pp. 45–68.

Jog, V and Ashwani, K 1995, “Capital Budgeting Practices in Corporate Canada”, Financial Practice and Education, vol.5 no. 2, pp. 37-43.

Klammer, T 1972, Empirical Evidence of the Adoption of Sophisticated Capital Budgeting Techniques, The Journal of Business, vol.45 no. 3, pp. 387-397.

Miller, J H 1960, A Glimpse at Practice in Calculating and Using Return on Investment, N.A.A. Bulletin (now Management Accounting), pp. 65-76.

Mussa, M 1986, “Nominal Exchange Rate Regimes and the Behavior of Real Exchange Rates: Evidence and Implications”, Carnegie-Rochester Series on Public Policy, vol. 25, pp. 117– 214.

Nguyen, M 2005, “Purchasing Power Parity”, sage publishers, New York

Obstfeld, M and Kenneth R 2000, “New Directions for Stochastic Open Economy Models”, Journal of International Economics, vol. 50, pp. 117–153.

Pike, R 1996, “A Longitudinal Survey on Capital Budgeting Practices”, Journal of Business Finance and Accounting, vol. 23 no. 1, pp. 79-92.

Rogoff, K 2003, Deflation: Determinants, Risks, and Policy Options- Findings Of An Interdepartmental Task Force, IMF, New York.

Rogoff, K 2002, Dornbusch’s Overshooting Model After Twenty-Five Years, IMF Working Papers 02/39, International Monetary Fund.

Ryan, P 2002, Capital Budgeting Practices of the Fortune 1000: How Have Things Changed? Colorado State University, Colorado.

Samuelson, P 1964, “Theoretical Notes on Trade Problems,” Review of Economics and Statistics, vol. 46, pp. 145–54.

Schall, Lawrence D., Gary L. Sundem, and William R. Geijsbeek, Jr., 1978, “Survey and Analysis of Capital Budgeting Methods,” Journal of Finance, vol. 33 no. 1, pp. 281-288.

StudyCorgi. (2022, July 11). Movement of Exchange Rate Volatility and Capital Budgeting. https://studycorgi.com/movement-of-exchange-rate-volatility-and-capital-budgeting/

Work Cited

"Movement of Exchange Rate Volatility and Capital Budgeting." StudyCorgi, 11 July 2022, studycorgi.com/movement-of-exchange-rate-volatility-and-capital-budgeting/.

* Hyperlink the URL after pasting it to your document

References

StudyCorgi. (2022) 'Movement of Exchange Rate Volatility and Capital Budgeting'. 11 July.

1. StudyCorgi. "Movement of Exchange Rate Volatility and Capital Budgeting." July 11, 2022. https://studycorgi.com/movement-of-exchange-rate-volatility-and-capital-budgeting/.

Bibliography

StudyCorgi. "Movement of Exchange Rate Volatility and Capital Budgeting." July 11, 2022. https://studycorgi.com/movement-of-exchange-rate-volatility-and-capital-budgeting/.

References

StudyCorgi. 2022. "Movement of Exchange Rate Volatility and Capital Budgeting." July 11, 2022. https://studycorgi.com/movement-of-exchange-rate-volatility-and-capital-budgeting/.

More Essays in Economics

This paper, “Movement of Exchange Rate Volatility and Capital Budgeting”, was written and voluntary submitted to our free essay database by a straight-A student. Please ensure you properly reference the paper if you're using it to write your assignment.

Before publication, the StudyCorgi editorial team proofread and checked the paper to make sure it meets the highest standards in terms of grammar, punctuation, style, fact accuracy, copyright issues, and inclusive language. Last updated: .

If you are the author of this paper and no longer wish to have it published on StudyCorgi, request the removal. Please use the “Donate your paper” form to submit an essay.

(1)

(1) (2)

(2) (3)

(3) (4)

(4) (5)

(5) (6)

(6) (7)

(7) (8)

(8)