Introduction

Banks in the United Kingdom are generally associated with the Big Four and the traditional banking and financial accounting approach. However, since 2015, applicant banks have been actively obtaining a license, often without physical offices to serve clients occupying specific niches in lending, clearing, mortgages, and business financing (Blomstrom, 2018, p. 18). Starling Bank is a similar institution, not the name of the offices for clients, providing full support to them remotely. This bank was founded in 2014; after a series of successful project financing by investors, it was able to fully launch by 2017-2018 with the support of business accounts (Starling Bank, 2021). The gradual expansion of the bank included partnerships with post offices, international payment processing, and euro accounts (Starling Bank, 2021). Although significant banks have repeatedly expressed interest in the takeover of Starling, the management itself rejects such statements (Lunden, 2021). The bank is about to exit with an initial public offering on the stock exchange, still funded by various funds (Hodson, 2021, pp. 863-864). Basically, the bank’s activities aim to maintain accounts, transfers, business support, and lending.

In fact, the capitalization of the bank is steadily growing every year. Moreover, Starling has been the best bank in Britain for the past four years (Hodson, 2021, p. 870). The absence of office maintenance costs and the implementation of advanced technical developments make this institution as competitive as possible in a reasonably diversified market. In addition to the big four, about a dozen other challenger banks are also battling to service business accounts, mortgages, and retail customers (Ramdani, Rothwell, and Boukrami, 2020, p. 12). The target audience of Starling is quite large and wide due to the fact that the range of services for individuals includes all the necessary and frequently used banking operations, which are accompanied by an ergonomic mobile application. The bank has about 3 million customers (Starling Bank, 2021). An innovative approach coupled with compliance with social and environmental responsibility requirements makes Starling a modern, sustainable and promising enterprise in a competitive market. This report contains an analysis of the macro-environment and external factors that influence the bank’s performance, its internal resources and strategies to cope with challenges and challenges, and recommendations for maintaining a competitive advantage in the banking environment.

Main Analysis

Macroenvironment

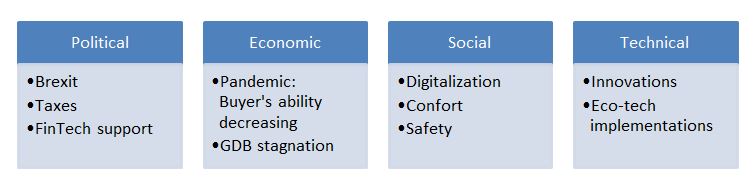

Starling Bank initially stated its vision as a sustainable, modern bank. Sustainability was dictated by concern for the environment and people, which was manifested in conserving essential natural resources due to the absence of offices and an ergonomic approach to goals. The range of bank services is quite broad, including business financing; therefore, Starling appeared in one of the most competitive markets and offered a new approach to the service, thereby creating a unique product that found its audience. Nevertheless, creating any bank is a fairly complex undertaking, depending on many external factors of the macro environment.

Various mechanisms manifest political influence on the financial sector. Firstly, the latest most striking event is Brexit, which took place in 2016-2017 and fell just at the launch of the main range of bank services (Samitas, Polyzos, and Siriopoulos, 2018, p. 185). Against the background of this exit, convenience in various payment systems in the provision of depository and clearing services will suffer regulatory due to the more complicated procedure for conducting international transactions (Samitas, Polyzos, and Siriopoulos, 2018, p. 183). The UK has become a “third country” in various statutes and acts of the European Union, which implies a unique relationship in the legal and financial environment with the countries (Vázquez‐Ordás and García‐Olalla, 2020, p. 570). Consequently, the most affected by this political factor are international companies and the judicial system, which will have to change the procedures for interacting with transnational documents and counterparties. However, despite these factors, Starling Bank allowed opening euro accounts in 2019.

We can assume that Brexit did not have a significant impact on the bank’s activities; on the contrary, such a political environment turned out to be favorable for obtaining a license. It is due to the fact that foreign European banks with their branches in Britain are faced with the need to reorganize business processes affected in the legal or economic field. The British exit ended the European Communities Act 1972, which required a significant change in legislation to close legal gaps due to the termination of EU laws in the country (Vázquez‐Ordás and García‐Olalla, 2020, p. 571). Potential disadvantages for Starling bank are connected only with possible potential expansion into the international arena, which is currently not in the corporation’s plans. On the other hand, the control and regulation of transnational instances have weakened, which is a plus for Starling, positioning itself as an exclusively private bank, not dependent on anyone else for its decisions.

Secondly, political support for financial technologies has been on the agenda of the highest authorities more than once. In April 2021, the Chancellor outlined the principal plans to create a dedicated new working group dealing with the bank’s digital currency, spurring innovation, and reforming capital markets (HM Treasury, 2021). For Starling, this factor would provide new opportunities for obtaining government grants as one of the country’s most innovative and sustainable banks. In fact, the financial support of representatives such as the Kalifa Review of UK Fintech and Tech Nation (Paige, 2022) became evident first. The last listed company has partnered with Starling in the form of practical development cooperation since at least 2019 (Tech Nation, 2019). As a result, the bank’s innovation policy has reliable allies who receive significant government support for new projects.

The built-in potential of state intervention turned out to be very useful on the eve of the pandemic. Starling’s operating expenses even led the company to a net profit loss in 2020, with a notable decline in 2019 (Starling Bank, 2021). If, in 2019, the company was forced to increase operating expenses to implement the technology for opening accounts in euros, then in 2020, the pandemic became an apparent reason. The UK has cutting-edge fintech developments in peer-to-peer lending, insurance, cybersecurity, blockchain, and artificial intelligence (Blomstrom, 2018, p. 20). Financial support accompanies not only government injections into venture capital but also the provision of accounting and legal support at an early stage, which makes the R&D opportunities equal for prominent players and start-ups (Treasures, 2021). Similar events took place before the pandemic, but their persistence shows that potentially innovative projects in finance and banking are welcome at the state level.

However, the pandemic had a much more significant impact on the macroeconomic environment. After the most successful 2018 with a net income of more than $63 million, Starling suffered a single loss in 2020 (Starling Bank, 2021). The company managed to bounce back from 2021 to 2019 levels, but the low pre-pandemic net income was driven by a surge in R&D (Starling Bank, 2021). Economically, Britain recovered from the crisis quite quickly during the pandemic, which is generally in line with Starling’s financial statistics (Trading Economics, 2022). GDP is growing slightly, but banking and insurance account for only 8% of the total service sector, which is key to Britain (Trading Economics, 2022). In parallel, there is a decline in market trade, which is reflected in the purchasing power of the country’s citizens (Trading Economics, 2022). Starling mainly works for the domestic market and, as a result, is more exposed to just such indicators.

Economic factors in the form of taxation are commensurate with the corresponding state support. With a relatively large amount of resources being explicitly invested in fintech, banking is a sector that has paid no fewer taxes in 2020 than in 2019, despite falling revenues (PWC, 2021). At the same time, corporate tax should potentially increase from 19% to 28%, according to government forecasts (Seely, 2022). Accordingly, Starling must expand its capabilities by diversifying services or capturing new target audiences for its products. It is because, in the new reality, the corporate tax will be significantly increased, the current stagnation in terms of GDP growth rates is predicted to continue, and purchasing power will decrease (Trading Economics, 2022). All these complications are caused by the consequences of Brexit, the pandemic, and the complicated geopolitical situation around Ukraine. Normalization of exports and imports, supply chains normalize only after a while, and during this period, Starling must adapt to the new situation.

Social factors include a natural increase in demand for digital products and a drop in interest and the need for physical bank offices. The younger generation, millennials, for the most part, prefer to manage their finances entirely remotely, and these survey indicators were statistically significant even before the pandemic (Sharpe and Lucht, 2021, p. 79). Moreover, over the past few years, investment tools have become more accessible to individuals with the same convenient and ergonomic presentation in applications (Mbama et al., 2018, p. 444). As a result, the number of investment literacy courses and materials on similar topics has increased. People have become more and more deeply interested in finance, using more financial instruments.

However, security remains a crucial issue, along with comfort and the ability to remotely solve any problems. Against the background of possible data leaks, which primarily damage the reputation of any company and provoke an outflow of employees and customers, financial security is the most critical aspect of Starling’s success. Although the only critical piece of information regarding personal data leaks in UK banking structures is the FinCEN case, which showed the involvement of institutions in money circulation of unknown origin, it has an entirely different scale compared to Starling’s local activities (BBC, 2020). The commitment to the security of personal data among individuals is associated with leaks in other areas of activity, both IT-related and non-IT (Mikalauskas, 2021; Cimpanu, 2021). Privacy issues are closely related to technological factors in the macro-environment.

The most promising developments and implementations are cloud storage of information, artificial intelligence with a predictive function, and work with big data. In terms of technology, Starling primarily relies on an environmental approach: the company’s offices run entirely on renewable energy, cards are made from recycled plastic, and document management was completely electronic from the very beginning (Starling, 2022). Starling does not disclose the implementation of advanced financial technologies in open sources; however, support for the comfort of using the application, and instant transfers, including those abroad, shows that quite a lot of work has been done. The PEST analysis is shown in Figure 1.

Opportunities and Threats

Starling Bank primarily competes with similar challenger banks with roughly the same capitalization as the big four. However, most of them have completely different tasks and, accordingly, the target audience. For example, Atom Bank, which has no physical offices, offers a broadly diversified deposit and mortgage offering (Atom Bank, 2022). Banks such as Tide and The Bank of London are entirely focused on business clients, diversifying their services into secure bank accounts and clearing obligations, respectively (The Bank of London, 2022; Tide, 2022). At the same time, Starling competes in the area of the most common banking services with the big four, which have much more significant experience in the local market.

Using Porter’s Five Forces Model, the main threats and recommendations for Starling Bank should be outlined to help maintain the competitive advantage that has allowed it to remain the best bank in the country for four years. It should also be taken into account that Starling Bank is a new player in the market, the threat of which was relatively low until relatively recently due to the difficulty of obtaining a license to operate a bank (Blomstrom, 2018, p. 28). The dominance of challenger banks has created a highly competitive environment in many banking services such that, for example, a 0.4% fee for transfers between GBP and EUR could be a factor to consider another service provider (Michael, 2021). Consequently, new players could threaten Starling in various ways, including better value propositions for customers, the use of a low service pricing strategy, and a more diversified range of services.

Accordingly, Starling may, in turn, consider product diversification as one of the solutions that not only provide the key to new audiences in business, investors, and many others but also allow old customers not to look for other applications for such purposes. Starling has a relatively high gross profit, which signals that the company has positive margins on the sale of its services, with the opportunity and resources for continuous development (Starling Bank, 2021). R&D spending is key to staying competitive, as technology solutions have enabled banks like Atom and Starling to provide quality customer support without offices.

The bargaining power of suppliers in the banking industry is quite strong but far from critical. Banks are turning to cloud storage providers, internet services, hardware support, and more. Most of these expenses are related to information technology, especially in the case of Starling Bank. The transition to other raw materials is critical since many things in the structure of a completely remote bank are tied to each other and may require cascading changes in others if changed in one branch. At the same time, there are practically no available mechanisms for regulating the forces of suppliers; however, Starling, being an entirely remote bank, has saved itself from the potential outsourcing costs associated with physical offices.

The trading power of buyers also turns out to be significant in a somewhat competitive environment, where each individual has a fairly wide choice. The uniqueness of a product or service in the field of finance can be dictated by both comfort, level of service, and its direct operational functionality. Starling was not the first bank without physical offices but was able to implement a similar model with the constant attraction of investments and a growing customer base. Product diversification will also be a protective mechanism against the outflow of potential customers, offering various options for managing financial resources.

Starling is a fresh player in the market, which was mainly able to get there due to technical innovation and the proper management approach. This approach will not change in the coming years, and technologies are not going to become obsolete; therefore, the threat of replacement should not be expected shortly, and if the development vector is maintained, then for many years to come. The cumulative competitive impact has been discussed above and generally leads to an inevitable conclusion. First, Starling has built its business around sustainable, modern, and innovative approaches that have resonated with investors and audiences. Secondly, to maintain a leading position, it is necessary to keep abreast of technology, pricing, and service. Innovation has always been the engine of progress in banking. The price of services will be a critical factor in the choice of representatives of the economy, which is in the process of uncertainty after several crises at once, such as Brexit, the pandemic, and the aggravation of the situation in Ukraine. Service, in turn, will reflect the quality of customer service.

Internal Resources

The company’s resources relative to competitors may be pretty small, but the approach in which they are used decides a lot. The company’s internal assets are nearly equal to its liabilities (Starling Bank, 2021). Therefore, Starling’s most crucial advantage is the management of these assets, which allows for increasing profits (Starling Bank, 2021). Revenues are split between liabilities and company development, and unlike competitors, property, equipment, and plant account for less than 0.5% of total assets (Starling Bank, 2021). This fact indicates that most cash flow passes exclusively through operating activities, which are not described by the costs of renting and electricity of offices for clients. At the same time, the company spends more and more on investments from year to year, adjusting the costs of financial and operational activities (Starling Bank, 2021). It can be concluded that the company’s assets are diversified and, therefore, represent a more flexible mechanism for its management.

When evaluating the company’s financial resources, it should be noted that they are of operational value, woven into the Starling organization, difficult to replace, difficult to imitate, but not rare. The capitalization of other banks, in some cases, reaches significantly higher values, but Starling has built a sustainable ecosystem that is based on the core values of a successful modern enterprise (Lunden, 2021). First, it is an environmental approach that translates not only as compliance with responsibility requirements but also as the company’s primary mission (Starling, 2022). Secondly, it is an entirely remote and high-quality service of the highest level, coupled with cutting-edge innovations in the field of technologies aimed at customers’ interests. The uniqueness of Starling’s offering lies in the more human touch in the bank’s automated and prominent structure, as outlined by CEO Anne Boden (Lunden, 2021). In addition, the value of remote support has been confirmed by global trends during social distancing and restrictions due to the pandemic.

In addition to financial assets, the company has human resources represented by the most sought-after experts on the market. One of Starling’s technical directors, after leaving the company, founded another bank, Monzo, which is a direct competitor to Starling (Lunden, 2021). This fact indicates the level of talents that make up the company’s team. At the same time, each employee is essential, as the hierarchical structure is minimal because Starling maintains only three offices across the country, ensuring interaction with customers remotely. The organization does not have employees who perform operational activities for customers in physical offices.

Consequently, according to the VRIN model, these resources are valuable in the context of Starling Bank’s success. Moreover, despite the trend of opening new banks since 2010, there are still few challengers. If a Starling employee could break into this market with a competitive offer, then such resources are rare in this industry. An innovative culture requires an appropriate mindset that anticipates the needs of the times, a capability that is difficult to imitate. Finally, employees are nonsubstitutable resources that cannot be attracted through outsourcing or other mechanisms.

Strategy

The company’s strategy is also complex, responding to the main competitive advantages and values outlined above. The company aims to become a net-zero organization with zero consumption of non-renewable energy (Starling Bank, 2021). Profitability is a key operational objective for a company (Starling Bank, 2021). Attracting investors allows unusual projects to come to life, including plastic cards for children with specific security mechanisms, online check issuance, and much more (Starling Bank, 2021). As a result, the company’s entire strategy is based on innovation, which is a competitive advantage in a relatively densely occupied market. At the same time, Starling does not tend to create alliances with such players; the company’s position is evident concerning acquisitions.

The social impact was manifested through high-quality service and the continuation of the trend of moving the financial management functionality online, following Atom Bank. To organize their business strategies, Starling relied on information technology, where they looked for possible ways to diversify products and services. As a result, the Starling culture allowed the bank to become one of the best in the country within four years. Financing comes from various investors interested in the project, including international ones (Starling Bank, 2021). Qualified employees created this product, which was able to attract significant funding, and now the project, for its part, is also attractive to new specialists, which contributes to sustainable development. At the same time, Starling preaches a more open, close, and humane attitude towards all interested parties without physical offices, overriding the classic officialdom in banks.

Conclusion

Starling Bank turned out to be a promising financial institution that appeared on the market just in time, correctly assessing the main trends and joining them. The absence of physical offices amid the pandemic has left management with problems with rent, employee salaries, and many other expenses. Ergonomic open-supported apps are a preferred feature of the company, which values time and comfort in managing its resources. Qualified employees and an innovative approach allow the bank, despite possible financial difficulties, to remain the best in the country. All these signs give the right to say that Starling Bank has laid a solid foundation for the company’s sustainable development.

At the same time, against the background of the analysis, it can be seen that the provision of opening accounts in euro against the background of the empty niche of European banks due to Brexit was a far-sighted and vital decision of the company. Such decisions should also be made in advance and guided by the geopolitical situation in the world. For example, now, during the crisis of the supply chain, export, and import due to military actions in Ukraine, Starling Bank may try to extrapolate its services to the international market. Such opportunities are opened to bring a similar level of service and comfort to business support against the backdrop of these problems. Given the ever-increasing investment in the project, Starling Bank should sooner or later consider potential expansion.

In addition, the current economic situation in Britain with a stagnant GDP is an opportunity for the company to realize more significant potential by diversifying products. With no domestic sources of income, Starling is attracting many foreign investors, showing growing financial performance. These opportunities open up a competitive advantage for the company by capturing potential new markets, such as clearing, mortgages, and more profound business support. The most important thing for Starling is to maintain the level of quality in services, humanity in support, environmental friendliness of the business, and innovative policies that have already led to success and allow them to retain several million customers. Only such an integrated approach can lead to sustainable development and constant struggle in a highly competitive environment.

Reference List

Atom Bank. (2022) Web.

BBC. (2020) ‘FinCEN Files: All you need to know about the documents leak’, BBC News. Web.

Blomstrom, D. (2018) ‘FinTech—Trends, Players, Challengers, and Bubbles’, in Emotional Banking (pp. 17-30). London: Palgrave Macmillan, Cham.

Cimpanu, C. (2021). ‘Hackers leak LinkedIn 700 million data scrape’, The Record. Web.

HM Treasury. (2021) ‘Ambitious plans to boost UK fintech and financial services set out by Chancellor’, UK Government. Web.

Hodson, D. (2021) ‘The politics of FinTech: Technology, regulation, and disruption in UK and German retail banking’, Public Administration, 99(4), pp. 859-872.

Lunden, I. (2021) ‘UK challenger bank Starling raises $376M, now valued at $1.9B’, TechCrunch. Web.

Mbama, C. I., et al. (2018) ‘Digital banking, customer experience and financial performance: UK bank managers’ perceptions’, Journal of Research in Interactive Marketing, 12(4), pp. 432-451.

Michael, C. (2021) ‘Got a Starling Euro account? – Beware the new 0.4% conversion fee’, Moneysaving. Web.

Mikalauskas, E. (2021) ‘12,000+ workers’ IDs, banking details, and other personal data leaked by UK staffing agency’, Cybernews. Web.

Paige, W. (2022) ‘UK fintech funding surges amid government drive to create global hub’, eMarketer. Web.

PWC. (2021) ‘The total tax contribution of UK financial services in 2020’. Web.

Ramdani, B., Rothwell, B., and Boukrami, E. (2020) ‘Open banking: The emergence of new digital business models’, International Journal of Innovation and Technology Management, 17(05), pp. 1-33.

Samitas, A., Polyzos, S., and Siriopoulos, C. (2018) ‘Brexit and financial stability: An agent-based simulation’, Economic Modelling, 69, pp. 181-192.

Seely, A. (2022) ‘Taxation of banking’, UK Parliament. Web.

Sharpe, A., and Lucht, W. (2021) ‘Banking on youth–young people champion sustainability futures for multilateral development banks in 2040’, Journal of Futures Studies, 25(4), 71-81.

Starling Bank. (2021) ‘Annual Report’. Web.

Starling. (2022) ‘Sustainable banking’. Web.

Tech Nation. (2019) ‘Introducing the 23 companies selected to join Tech Nation’s 2019 Fintech programme’, Tech Nation. Web.

The Bank of London. (2022) Web.

Tide. (2022) Web.

Trading Economics. (2022) ‘United Kingdom GDP growth rate’. Web.

Treasures. (2021) ‘Chancellor unveils massive venture capital pot for fintech start-ups, plus funding for national network of industry experts’, Act. Web.

Vázquez‐Ordás, C. J., and García‐Olalla, M. (2020) ‘The Differential Impact of Brexit on Banking: UK vs. Europe’, Global Policy, 11(5), pp. 569-577.