Which company are we looking at?

The Toronto-Dominion (TD) Bank

Where does it take place?

In Canada

What is the time frame?

In 2021

What industry are we analyzing?

The paper analyzes the banking industry but with more focus made on digital banking

External Analysis (PESTEL + CDG)

Political Factors: The TD Bank Group may benefit from trade blocs and treaties developed and signed by the respective country of origin. TD Bank Group may benefit from trade agreements that the various companies initiate and complete. For example, striking a trade deal with Nutmeg, a UK investment firm, might help the company expand its customer base (Ross et al., 2022).

Economic Factors: The banking industry’s online world has been fast altering due to smartphone use, big data, machine intelligence, and prescriptive modeling. In Canada, smartphone acquisition exceeded 85%, with rates exceeding 95% among those aged 44 and younger, 87% among those aged 44 to 64, and around 60 percent among those aged 65 and older (Ross et al., 2022).

Sociocultural Factors: The more significant proportion of younger people benefits TD Bank Group in developing an effective corporate data management policy, as it provides the organization with a broader consumer demographic base. Ross et al. (2022) enumerated that 95% of smartphone users in Canada were youth, thus, implying that TD Bank Group will have access to more competent and educated individuals and human resources.

Technological Factors: Fintech, a technology innovator, has gained significant traction in the financial sector in recent years due to its mechanization and effectiveness in building connections with consumers. Fintechs bridged the gap between financial institutions and clients by offering innovative technologies-based services (Ross et al., 2022).

Legal Factors: The Canadian federal government demanded that banks subject applicants to a comprehensive financial hardship assessment to qualify for a mortgage. Fintech borrowers often entered the sector by concentrating solely on substandard loans, as Canadian banks have historically avoided these consumers (Ross et al., 2022).

Capital Markets: TD partnered with Kasisto in 2017 to provide consumers with immediate feedback to particular spending queries, such as how much they paid on a recent vacation, their most outstanding payment during a week, or how much they spent on areas such as coffee. TD purchased Layer 6, a pioneer in cognitive computing, in 2018 to bolster its strengths in delivering reactive, tailored, and insight-driven consumer experience (Ross et al., 2022).

Demographics: Compared to the 44 to 64 age category, the 44 and younger age bracket has a higher smartphone adoption rate. Digital banking adoption was highest among millennials and generation z (Ross et al., 2022). On the other hand, middle-aged persons are more likely to generate additional revenue sources than younger generations, as they have a secure income.

Globalization: The banking sector is a dynamic landscape where individuals are consistently on the go, making it more difficult to attract consumers because they are constantly on the lookout for efficiency and the bank with the best rates.

External Analysis – Industry Facts

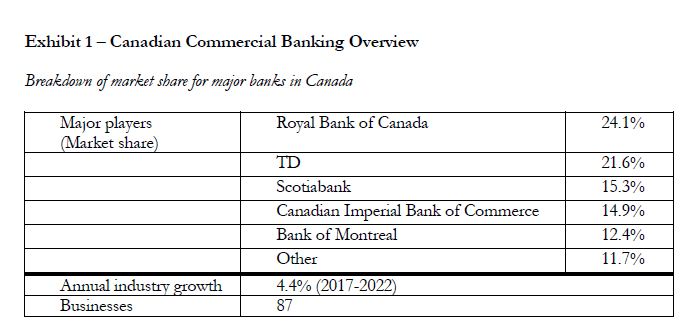

Size: The country’s top five banks, namely the Royal Bank of Canada, TD Bank, Imperial Bank of Commerce, Bank of Nova Scotia, and Bank of Montreal, control 90% of the sector’s asset value (Ross et al., 2022).

Life Cycle Stage: TD Bank is at the shakeout stage of a business’ life cycle. Organizations are inevitably liquidated because they cannot keep up with industry growth or generate negative cash flows. Certain companies combine with opponents or are bought by those that grew their market share during the growth period (Bhattacharya et al., 2020).

Competitor Facts: While TD wishes to continue along the digital path and increase some of its recent operations, it may be challenging to do so given Fintech’s alliances with large businesses and entrenched status. The cost reductions associated with being entirely digital provided cheaper rates and more significant incentives than conventional banks.

Industry Trends: Banks are increasingly integrating online payments into their regular operations. According to the Canadian Bankers Association, 56% of Canadians utilized internet banking in 2019, with 76% conducting most of their banking through internet channels (Ross et al., 2022). Most banks are dedicated to providing a diverse mix to their customers to satisfy them.

MSF/KSF (Minimal Survival Factors/Key Survival Factors): Businesses must establish long-term connections with users, as they are continuously changing banks. Recruiting and retaining customers is critical to prosperity; thus, this is accomplished through superior quality and service and a diversified assortment of products and services offered via various retail channels.

External Analysis – Attractiveness

Ease of Entry: Entrance into the banking sector is more complicated, as physical institutions functioning in Canada are subject to government regulations and demand a significant amount of capital to open. It is quite challenging to enter because of legal standards and requires significant finance to fund an institution’s start-up.

Power of Buyers: Although consumers have considerable negotiating power since they can readily switch banks, they nevertheless rely on banks to fund prospective savings and lending possibilities that may come in the near term. Ross et al. (2022) stated that it was not simply convincing people to migrate from their lenders to a new Fintech solution for everyday routines.

Power of Suppliers: Suppliers wield tremendous influence, as the state controls the economy’s money resources, whether through printing more money, withdrawing some from the market, or even supplying rates to banks. The Canadian legal authorities decided this through a financial stress test administered to bank debtors.

Threat of Substitutes: There is a high risk of substitution, as there is not just commercial banking but also online banking, which has generated a lot of buzzes, such as Neobanks and challenger institutions, as consumers are more receptive to going digital.

Rivalry Intensity: There is fierce competition in Canadian digital banking since it all comes down to price and range of service offers. Additionally, depending on the quality that financial institutions provide to their audience.

Competitor Facts: Fintechs were bridging the gap between financial institutions and consumers by offering innovative technologies-based services. They provided loans, mortgages, savings, trading platforms, and other standard banking services. While Fintechs continued to rely on banks to complete the items they marketed, the Fintechs interacted with their users, thereby isolating banks from their consumers (Ross et al., 2022).

External Analysis – Competition Evaluation

The competition assessment of digital banking in Canada is a wealthy one. TD’s customer base in Canada was approximately 21%, ranking first or second in market dominance for most retail items (Ross et al., 2022). It was a top three financial broker in Canada in 2018 and employed approximately 38,800 people.

External Analysis – OT Summary

Opportunities

The development of Fintech intelligent automation enables firms to reduce their operating costs.

Additionally, one of the factors for the change to e-banking was growing technological use, mainly banking through smartphones. According to the Canadian Bankers Association, 56% of Canadians utilized online banking in 2019, with 76% utilizing online and mobile financing to perform the majority of their transactions. Therefore, this provides a more extensive client base to appeal to, which increases the likelihood of increased revenues (Ross et al., 2022).

Threats

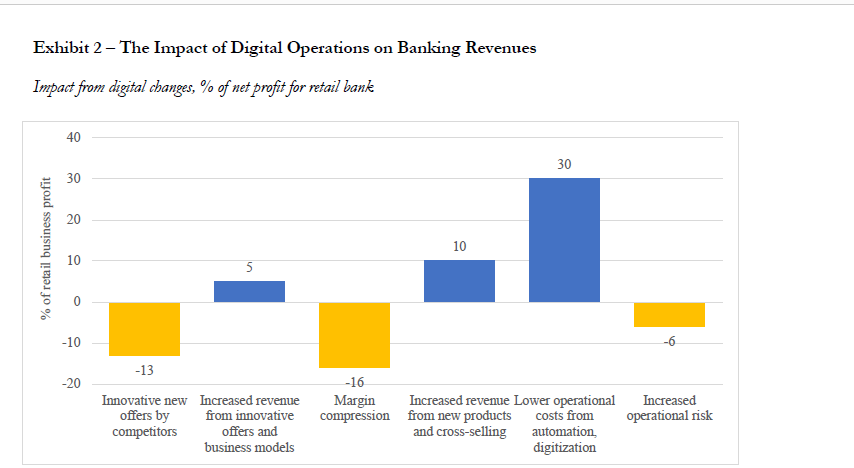

The figure below illustrates that fierce competition from other well-established and upcoming financial institutions threatened TD.

TD faces stiff competition from the Royal Bank of Canada that has the most market share of 24.1%. However, with the increasing industrial development, other players such as Scotiabank poses significant threats. Disintermediation that entails the elimination of the middleman who played a critical role in linking TD Bank to its consumers. The emergence of non-tech enterprises that offer their tiny payment methods to customers.

Internal Analysis – Operations

Supply Side: Collaborate with vendors who may benefit from digital technology in their activities. Investment in the digital realm to restructure its online presence. Application programming interfaces were created to enable third-party developers to develop facilities and strategies that interacted with the technology.

Conversion Cycle: TD has a digital customer base of approximately 12 million. It has a long history of pushing limits and being inventive to provide clients with digitally enhanced experiences. In 2017, TD launched speech banking capabilities on Alexa, a Wi-Fi-enabled gadget that can be used to do a range of functions via voice requests (Ross et al., 2022).

Distribution: Understanding that over 56% of Canadians were apprehensive about homeownership, TD partnered with Flybits to launch the homeowners’ adventure. Additionally, they could obtain a computerized mortgage pre-approval and lock in a rate for 120 days (Ross et al., 2022).

Liquidity: TD Bank’s earnings in the third quarter of 2018 in its three retail outlets indicate a higher liquidity ratio, thus in a position to pay off its debts and finance its operations.

Financial Ratios Leverage: With the impact of digital finance influencing the net incomes of TD Bank negatively, its consumer leverage ratios are higher, stipulating more debts, thus affecting its ability to finance some of its activities.

Activity: Investing heavily in the bank’s entire infrastructure upgrade and talent acquisition. Developing collaborations or purchases by understanding that the Fintech environment’s rapid expansion presented issues and provided diverse small businesses the institution could engage or buy for creative technologies and speedy exposure to technological capabilities.

Profitability: TD’s sales volume in Canada was approximately 21%, and the company was rated for most retail items (Ross et al., 2022).

Growth: Canadian retail provided nearly 60% of revenues in the third period of 2018, while the US retailing generated 26%. Consumer banking accounted for about half of the Canadian businesses’ total income, while corporate banking accounted for 13%, asset management accounted for 18%, and insurance accounted for another 18% (Ross et al., 2022).

Manage Other Risks: Other issues about technology should be managed effectively, such as Fintech’s copyrights for start-ups, allowing them to maintain a hold over their discoveries.

Internal Analysis – Customer

Segmentation: Digital banking was created for authorities and influential organizations, but it could also be used by adolescents opening their initial savings account. Younger consumers, such as undergraduates, were beginning their independent lives and lacked substantial bank deposits or the need for various financial goods, such as a mortgage.

Attracting New Customers: TD Bank can attract new potential clients through mergers and acquisitions of other financial institutions. For instance, viewing Fintech as an opportunity and not a threat enabled it to merge, thus increasing its customer base (Ross et al., 2022).

Retaining: In retaining its clients, TD Bank must accomplish its mission statement to them. While the size and financial laws provide certain hurdles to TD Group, their consistency and competence work in its favor (Ross et al., 2022). Users’ major aspects are safety and security, and we have significantly more critical expertise negotiating the complicated legal regime.

Increase Order Size: With the increasingly digital environment, the number of people accessing smartphones is likely to increase. Therefore, TD should improve the ease and efficiency of accessing their services. Increasing its order size attracts more customers, thereby increasing its market share.

Internal Analysis – Innovation

Market Research: The financial institution’s market research is based on provocative insights, comprehensive coverage, and impactful outcomes. Therefore, quick and precise information is essential in acquiring a competitive edge in today’s industries.

R&D: TD has made significant investments in modernizing its IT architecture, ensuring that new features may be seamlessly incorporated into its digital environment while guaranteeing cyber security (Ross et al., 2022).

New Development: Planning to do in the Future: TD, through its CEO, had plans for mergers and acquisitions with other multinational companies to improve its market potential. Hogarth understood that while the explosive development of the Fintech ecosystem posed issues, it also provided a plethora of small businesses with which the company could collaborate for creative solutions (Ross et al., 2022).

Internal Analysis – CSR

Environmental: TD was one of the first institutions in North America to see the climate crisis as a factor that would affect how people do commerce. Since then, it has created an enterprise-wide sustainability strategy to establish a long-term perspective on the possible dangers and benefits associated with global warming.

Employee Policies: TD is committed to training its employees and cultivating an atmosphere that fosters greatness. TD measures its effectiveness using a personnel engagement score, optional labor turnover, and industry comparison.

Health and Safety: TD’s commitment to providing an exceptional environment includes safeguarding and encouraging the wellness of its workforce. To accomplish this, it has developed significant initiatives to assist employees in assessing, managing, and improving their well-being across three essential domains: physiological, economic, and cognitive.

Community Support: As a responsible company, TD strives to make a good impact on the economies in which it operates. TD’s growth strategy aims to achieve sustainable, profitable development by strengthening strong franchises and providing value to consumers, stakeholders, and the wider population.

Internal Analysis – Intangibles

Leadership: TD’s CEO, Tim Hogarth, was a strategic manager who understood the dynamics of the evolving banking industry. He sought novel strategies in making TD survive the digital transformations despite the fierce rivalry from well-established firms and new upcoming ones.

Management: The administration at TD was robust management as it carried out intensive research to determine the cause for the shift from physical banking to online banking and to have appropriate mechanisms to adopt that change

Human Capital: TD has employed roughly 38,000 employees in all its storefronts, according to Ross et al. (2022).

Organizational Structure: TD Bank’s divisional structure enables it to execute various procedures across different areas successfully. Retail banking, wealth management, corporate finance, and insurance are examples of this.

Culture: TD’s commitment to inclusiveness, transparent governance and community participation energizes its culture. A career at TD entails possessing the resources necessary to maximize an employee’s potential.

IT: TD’s massive investment in information technology enabled it to catch up with other technology industries providing it with a strategic advantage.

Internal Analysis – Current Strategy

TD seeks to separate itself from its competitors with a distinctive brand grounded in a corporate framework and motivated by empowering its consumers, neighborhoods, and employees to flourish in a complex environment.

Evaluation

Table 3: Evaluation

Internal Analysis – SW Summary

Strength: TD served a diverse consumer base and functioned in various retail markets. Governments and major organizations were on one end of the scale, while small children opened their first savings account on the other (Ross et al., 2022).

Weakness: The shorter technological cycles of TD were a challenge, thus requiring banks to respond rapidly with instruments that changed frequently and were beyond their core competencies.

Issues

Table 4: Issues Analysis

Alternatives

Selected Issues that Are Meant to Address

- Fierce competition

- Cyber security

- Upcoming Neobanks

Proposal

Selection Criteria Logic

- Cost and benefits selection criterion

Implementation

Does Everything FLOW?

Do Issues Flow from the SWOT analysis?

The issues selected represent some of the SWOT analysis of TD bank.

Do Alternatives Address the Issues?

The chosen alternatives provide insights into what TD could improve its competitiveness.

Is the Solution the best of the Alternative?

For sure, investing more in R&D is both a long and short term solution because the digital landscape is prone to technological changes

Have we found a way & timeline to implement the Solution?

Increasing financing in the R&D department in three months would increase TD’s market position.

References

Bhattacharya, D., Chang, C. W., & Li, W. H. (2020). Stages of firm life cycle, transition, and dividend policy. Finance Research Letters, 33, 1-29. Web.

Ross, M., Carayannopoulos, S., & Donovan, M. (2022). TD – Preparing for the future of banking. North American Case Research Association, 41(1), 1-20.