Executive Summary

Effective inventory (cash) management is crucial for achieving optimised supply chains and cost reductions to remain competitive and resilient in turbulent times. Retail banks must efficiently process and deliver cash to customers to lower inventory levels and reduce costs.

They employ demand/supply strategies to ensure optimised replenishment of branches and ATMs. The cash supply chain consists of merchant and retail customers who transact through a bank’s ATM and branch networks. Therefore, effective logistics planning and outsourcing of the cash management function can reduce operational costs, achieve efficiency, and improve productivity.

Introduction

Although global sourcing has contributed to a more integrated multilateral trade in the automobile manufacturing industry, it has made production riskier and uncertain. This reality has made supply chains (SC) more complex and distribution networks less predictable. In practice, conventional SC risk management strategies can only be applied to familiar and measurable SC risks.

However, managing risks in an uncertain landscape require resilience and responsiveness as such tools are less effective (Pettit, Fiksel & Croxton 2010). SC resilience is needed to navigate through obstacles such as the bullwhip effect, high inventory levels, and demand fluctuations, among others. This paper analyses the inventory management as a tool for achieving successful supply chains and resilience in the banking services industry.

Inventory Management in Banking

Inventory turnover is considered a crucial asset of a firm that determines its net earnings. In practice, effective inventory management requires knowledge of available stock, ways of presenting key brands, and inventory replenishment. Service inventory management not only determines a firm’s revenue but also its customer base. Undisclosed inventories affect company profits because they contribute to additional costs (Pettit, Fiksel & Croxton 2010).

Offering inadequate service causes the product to be unavailable, a scenario that may force a customer to go for competitor products. Therefore, inventory practices of a firm constitute a good indicator of its performance and stability over a business year. For example, during an economic crisis, inventories may accumulate due to a decline in sales. As a result, the firm’s management could decide to write down the value of the inventory, resulting in lower sales revenue when the goods are eventually sold. Thus, inventory decisions in times of turbulence or external pressures would determine its stability.

The motivations that drive inventory decisions vary between firms. Pressure on the management to record a profitability growth may lead to considerable inventory levels. The way a firm handles external pressures, i.e., maintains stability, depends on its inventory turnover and value of inventories (Sturgeon et al. 2009). A low inventory turnover often leads to a devaluation of inventories in a bid to perform better in turbulent environments. However, inventory write-downs affect long-term firm performance as the inventory will be sold at a lower price than its value. Therefore, inventory management practices constitute a good indicator of a firm’s stability in unstable economic conditions.

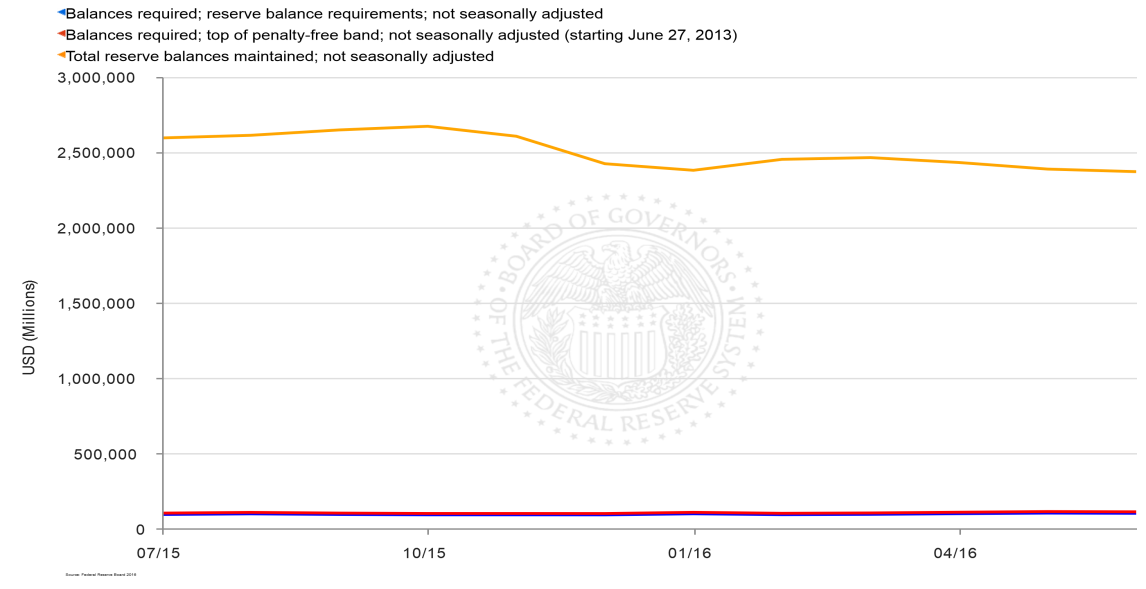

In the banking services sector, maximising profits while complying with statutory laws is a common practice. Major central banks, e.g., the Federal Reserve and the Bank of England require commercial banks to “hold statutory reserves against transaction deposits” at a 10% reserve-requirement ratio (Anderson & Rasche 2012). The statutory reserves include an institution’s deposits at the feds and vault cash. Violation of these regulations attracts sanctions. Banks have devised ways of making use of the statutory reserves.

The deposit sweep program is an inventory management scheme entails connecting two related accounts, “the bank transaction account (BTA) and the money market deposit account (MMDA)” (Anderson & Rasche 2012, p. 53). While funds held at the BTA are subject to the 10% reserve requirement, those in MMDA are not. Thus, using the sweep program, banks can maintain low or high reserves (inventory) depending on the existing interest rates. The level of reserves maintained by commercial banks against the required reserves is shown in Figure 1 below.

Inventory management in banking entails the control of cash flows through two methods, namely, the threshold method and cushion method. In the threshold method, a BTA limit is indicated for every customer (Anderson & Rasche 2012). The volume of money BTA-MMDA transfers is usually unrestricted and the cost of such transactions is nil. In case the BTA account balance goes beyond the BTA limit in a particular day, a BTA-MMDA transfer is made before the close of business (Anderson & Rasche 2012). Threshold values are set to ensure that cash in the BTA is maintained at acceptable levels.

In the cushion method, cash deposits received within a particular month are put in the MMDA account, provided that the monthly BTA-MMDA transfers are maintained below six (Anderson & Rasche 2012). MMDA debits come from the BTA account. Therefore, a single debit transaction leads to an MMDA-BTA transfer in addition to “a day-specific cushion amount” (Anderson & Rasche 2012, p. 61). In cases where the BTA cash cannot service debit transactions, more funds are transferred from MMDA. The idea here is to provide a cushion for each cash transfer.

The Banking Services Supply Chain

The advent of integrated payment methods has contributed to increased customer’s accessibility to cash. In particular, automated teller machines or ATMs have increased the volume of daily transactions. However, managing these platforms increases the banks’ operational costs and constrains the cash supply chain. Operational expenses are related to the costs of keeping, counting, transporting, and securing the cash.

According to Silvestro and Lustrato (2014), handling cash costs banks over $300 billion annually. In this view, commercial banks need efficient cash handling strategies. Consumer Business (CB) institutions have emerged as efficient models of managing the cash supply chain to enhance competitiveness in this industry. Reducing costs in the supply chain is one way of improving productivity in the banking supply chain. For example, banks are implementing operational changes targeting their branch operations to reduce costs and provide low-interest rates to customers.

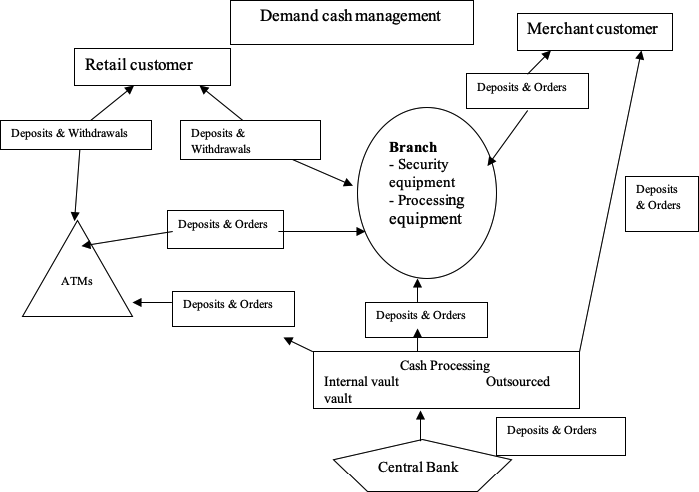

The commercial bank supply chain is highly complex. Therefore, the cost of maintaining cash SCs is huge. It ranges from funds required to maintain technologies and equipment to costs related to transportation of cash to branches and ATMs. The cash SC is shown in figure 2 below. The rising volume of cash in circulation makes the SC costs even higher.

For example, the Feds and the European Central Bank indicate that the cash in circulation has increased by 9% since 2013 due to the rising demand for cash (Anderson & Rasche 2012). As a result, banks have to contract more agencies and open more ATMs to supply cash to customers. For example, in the US, more than 400,000 ATMs have been deployed over the past decade, representing a 23% increase (Anderson & Rasche 2012).

Besides the use of ATMs in the cash supply chain, technology deployment is another key feature of banking services SCs. Modern ATMs use sophisticated systems and security modules to curb cybercrime. Also, a range of hardware components, e.g., optical scanning, have been deployed to enhance efficiency. The enhanced features have increased the cost of cash management, with the cost of operating one ATM estimated to be $1700 monthly in North America (Anderson & Rasche 2012).

Supply Chain Resilience

Resilience, as a concept, originates from the Engineering field. Klibi and Martel (2012) describe resilience as the capacity of a system to revert to its initial state “after a stressful situation, without any change in its nature” (p. 887). In business, the instability of the competitive landscape and the possibility of unforeseen risks call for supply chain resilience to maintain a strong competitive position. A firm’s ability to endure, adapt, and thrive in a risky environment determines its resilience.

Widespread supply chain disruptions elicited interest in SC resilience as a competitive driver (Muller 2009). Therefore, SC resilience is central to effective supply chain management. SC resilience is the capacity of the supply chain to overcome the effects of unforeseen risks and return to its initial state or become more efficient after the disruption (Peck 2005). It refers to the ability of a firm to deal with SC disruptions that affect performance and competitiveness in the long-term.

Resilience requires a high level of flexibility, especially concerning “process redesign, sourcing decisions, and collaborative SC relationships” (Sturgeon et al. 2009, p. 16). By creating SC flexibility, firms can enhance resilience during turbulence and maintain a high operational efficiency to match sudden demand increases. Also, strategies such as cooperation, information exchange, SC integration, can build resilience during disruptions.

Ambe and Badenhorst-Weiss (2011) suggest that firms should learn from their experiences to develop a framework for increasing SC resilience and reduce vulnerabilities to maintain a strong competitive position. Implementing an SC risk management strategy can help build a firm’s resilience capability such as cooperative relationships, resource mobilization, and information sharing with other supply chain members.

The Concept of Flexibility

In banking services, SC flexibility is required to reconfigure the system’s ability to overcome constraints associated with cash flows. In contrast, SC inflexibility reduces responsiveness and SC resilience. Flexibility is, therefore, a core component of SC resilience that denotes a firm’s capacity to change or respond to external shocks. Flexibility in production systems can be divided into four types, namely, “product, mix, volume, and delivery” (Stevenson & Spring 2007, p. 689). Product flexibility describes the capacity of a firm to launch new merchandise or modify the current products to meet market demand and preferences.

In contrast, mix flexibility is the capability to change the product mix without affecting the output (Stevenson & Spring 2007). Volume flexibility enables a manufacturer to alter the quantity of its output in response to demand fluctuations while delivery flexibility allows a firm to adopt flexible delivery schedules for orders. Besides system flexibility, inter-firm flexibility can help a firm re-align its SC and build strong relationships with SC members. Achieving inter-firm flexibility requires flexible logistics to maintain optimal inventory to meet demand changes efficiently. Sourcing flexibility is also important to create SC resilience in the automotive industry.

Sourcing flexibility enables firms to find alternative suppliers for car parts, especially when faced with an unanticipated demand rise. It is defined as the capacity to “rapidly change inputs”, such as product design, or alter supplier contracts to fulfil orders (Bowersox, Closs & Cooper 2010, p. 56). Firms also use alternate distribution channels or re-route their freight to meet demand increases. Therefore, flexibility not only creates resilience, but it also improves SC performance. Bowersox, Closs, and Cooper (2010) argue that close supply relations impede flexibility because manufacturers cannot change suppliers with ease, creating a domino effect on the supply chains.

The Retail Banking SC Model

In retail banking, cash can be considered as inventory in the SC. Therefore, CB strategies for inventory control, handling/processing cost reduction, and enhancing efficiency are required. The CB methods used in SC management involve four stages: plan, source, make and deliver.

Plan

Planning entails demand forecasts to control excess inventory and enhance efficiency. Excess inventory (cash) increases operational costs while shortages affect the reputation and may lead to losses. Therefore, inventory planning can result in significant cost savings.

A bank’s ATM or branch should always have cash, as shortages can affect the institution’s public image. On the other hand, excess cash in an ATM should be used to generate revenue. According to Silvestro and Lustrato (2014), the amount held in ATMs is 40% in excess. Through proper planning of transfers, banks can maintain optimal cash inventory and reduce costs while ensuring sufficient funds for customer transactions. The table below shows the impact of planning on cash inventory.

Table 1: Impact of Planning on Cash Inventory

Source

The second stage of the model, i.e., sourcing, involves reducing the supplier spending to save costs. Business organizations use collaborative approached to create value for their products or services. Furthermore, firms consolidate their suppliers, increase their buying power, and achieve uniform standards to reduce costs and generate value (Silvestro & Lustrato 2014).

In banking, strategic sourcing relates to cash SCs, including cash processing and transportation. A significant amount of the expenditure goes into the deployment of cash distribution equipment and technologies and transportation of cash in the SC. Banks employ diverse supply- and demand-side approaches to achieve strategic sourcing and reduce costs. Examples of such strategies are summarised in the table below.

Table 2: Supply and demand sourcing strategies

Commercial banks tend to outsource their services to onshore and offshore suppliers. However, industry-wide sourcing strategies can yield greater cost savings than regional sourcing. Enterprise-wide sourcing of hardware and services has been shown to reduce costs by up to 20% (Silvestro & Lustrato 2014). Outsourcing the cash management function is common in the retail banking industry. For example, TD Canada Trust contracted out the replenishment of cash in ATMs to G4S (Silvestro & Lustrato 2014). The bank also outsourced the maintenance of its ATMs to HP to enhance efficiency and reduce costs. Outsourcing of certain functions brings multiple advantages to banks. Examples of advantages (cost savings) derived from outsourcing are summarised in Table 3 below.

Table 3: Outsourcing costs and savings

Make

The common strategies utilised by most firms to cut costs include Six Sigma and lean production. In the banking SC, lower costs are achieved through streamlining the currency processing service (Silvestro & Lustrato 2014). Since banks handle a large sum of cash, it is important to minimise the cost of processing it to achieve efficiency. Lean operations in the context of banking mean reducing waste, expanding capacity, and minimising maintenance costs.

It entails expanding the internal processes to minimise the duration between cash collection and replenishment. Deploying ATMs that support cash replenishment based on deposits can help improve capacity. Additionally, the use of predictive tools can help banks anticipate cash flows to reduce maintenance costs.

Deliver

Firms use efficient logistics strategies to provide goods/services to the customer on time. They use optimised routes to reduce costs and avoid inventory obsolescence. In the banking industry, the key concern is delivering cash to the customer at the right time in convenient locations. Another concern relates to the security and reliability of the transportation system or third-party agency. The central aim of this industry is to minimise the costs of delivering the product (cash) to the customer. Therefore, the strategic placement of branches and ATMs can help optimise the delivery routes and reduce costs.

Silvestro and Lustrato (2014) suggest two ways banks can optimise their logistics to achieve efficiency in cash delivery, namely, network optimisation and logistics planning. Banks can achieve lower delivery costs by optimising their branch and ATM placements. The delivery of cash should involve optimised routes to save time and costs during replenishment.

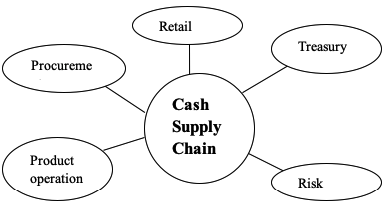

Another strategy involves outsourcing the function to third-party firms. This approach can help reduce maintenance costs and achieve high productivity by focusing on the core business objectives. Examples of core business objectives include risk, procurement, treasury, and retail business. Adopting optimised logistics approaches can strengthen the cash supply chain to support the core business functions as shown in the figure below.

Conclusion

Inventory (cash) management in banking requires optimised supply chains to achieve cost reductions and enhance efficiency. Supply chain planning in banking entails the use of a demand-driven logistics strategy to deliver products at the right time and reduce costs. It also entails cost-effective sourcing of third-party agents and the use of lean and Six Sigma principles to enhance cash flows.

References

Ambe, I & Badenhorst-Weiss, J 2011, ‘An automotive supply chain model for a demand-driven environment’, Journal of Transport and Supply Chain Management, vol. 1, no. 2, pp. 1-11.

Anderson, R, & Rasche R 2012, ‘Retail Sweep Programs and Bank Reserves’, Federal Reserve Bank of St. Louis Review, vol. 83, no. 1, pp. 51-72.

Bowersox, D, Closs, J & Cooper, M 2010, Supply chain logistics management, McGraw-Hill, Singapore.

Klibi, W & Martel, A 2012, ‘Modeling approaches for the design of resilient supply chain networks under disruptions’, International Journal of Production Economics, vol. 135, no. 2, pp. 882-898.

Muller, M 2009, ‘Current automotive industry: how leaders practise CI’, Competitive Intelligence, vol. 11, no. 3, pp. 23-31.

Peck, H 2005, ‘Drivers of supply chain vulnerability: an integrated framework’, International Journal of Physical Distribution & Logistics Management, vol. 35, no. 4, pp. 210-232.

Pettit, T, Fiksel, J & Croxton, K 2010, ‘Ensuring supply chain resilience: development of a conceptual framework, Journal of business logistics, vol. 31, no. 1, pp. 1-21.

Silvestro, R & Lustrato, P 2014, ‘Integrating financial and physical supply chains: the role of banks in enabling supply chain integration’, International Journal of Operations & Production Management, vol. 34, no. 3, pp. 298-324.

Stevenson, M & Spring, M 2007, ‘Flexibility from a supply chain perspective: definition and review’, International Journal of Operations & Production Management, vol. 27, no. 7, pp. 685-713.

Sturgeon, T, Memedovic, O, Biesebroeck, J & Gereffi, G 2009, ‘Globalisation of the Automotive Industry: Main features and Trends’, International Journal of Technological Learning, Innovation and Development, vol. 2, no. 1, pp. 14-19.