Liquidity ratios

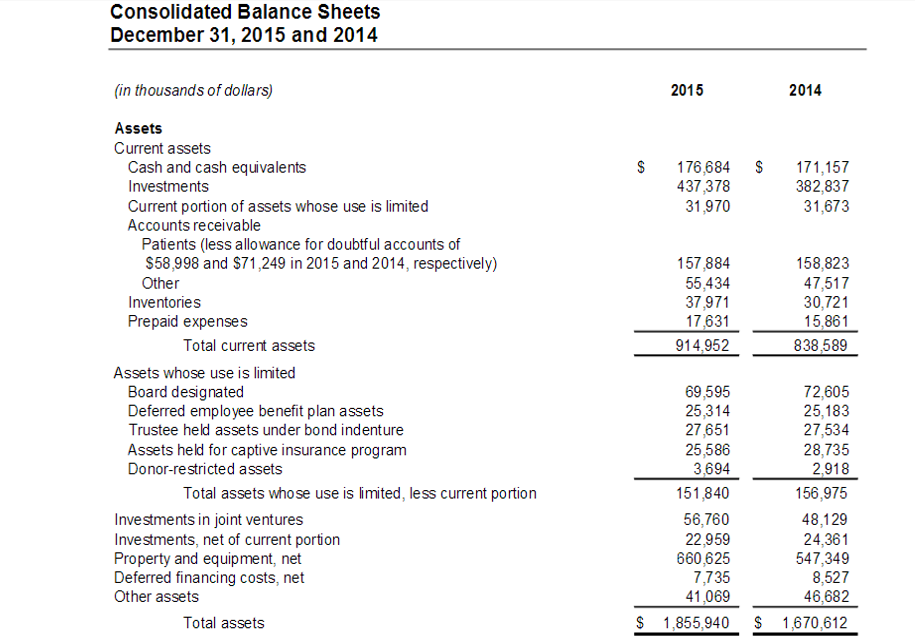

The calculations above show that there was a slight drop in current ratio. However, the values are high and greater than industry average. This shows that the Hackensack University Medical Center has a strong liquidity position. It can also imply that the company is holding a lot of cash in the form of current assets (Atrill & McLaney, 2013). The collection period dropped. This shows an improved efficiency in collection of accounts payable. The day’s cash-on hand and average payment period increased.

Profitability

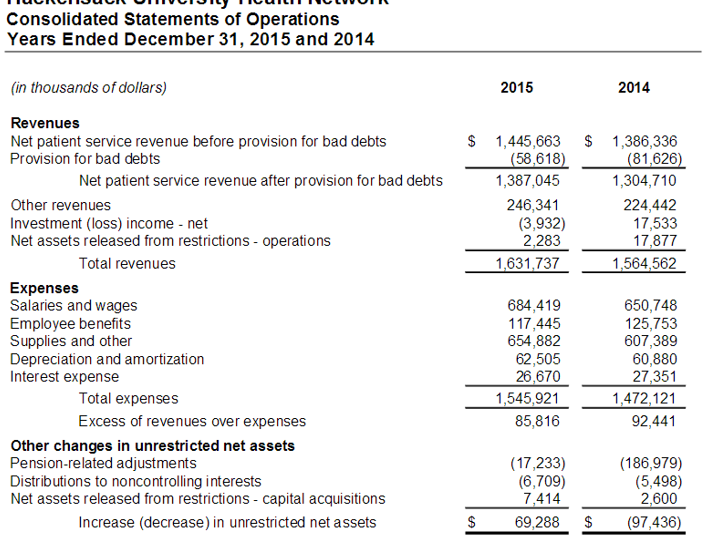

The three ratios show that the profitability of the company dropped in 2015. This can be attributed to a decline in net profit for the year (Hackensack University Health Network, 2015).

Asset efficiency

There was a drop in asset efficiency ratios. The efficiency in the use of total assets, fixed assets, and current assets deteriorated. Besides, the ratio shows that the average age of the fixed assets dropped. This can be an indication that the assets are wearing out and there is need to continuously replace them. Finally, inventory turnover dropped and it shows that rate of stock movement declined (Atrill & McLaney, 2013). Thus, overall efficiency deteriorated.

Capital structure

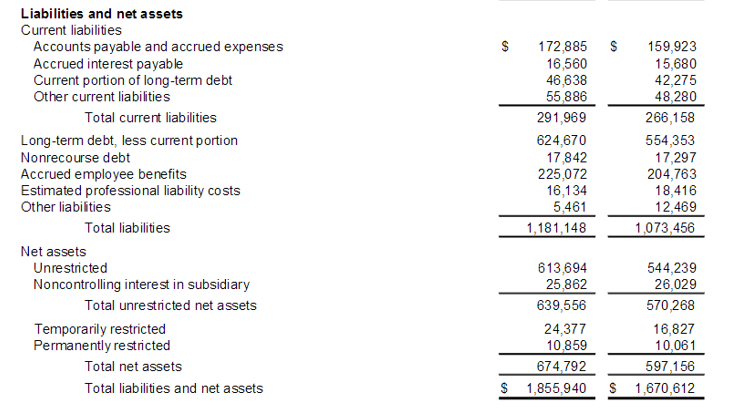

Long term to capitalization ratio remained constant in 2014 and 2015. However, there was a slight decline in debt service coverage. This can be attributed to a decline in net income. Finally, cash flow to debt ratio also deteriorated. Thus, the capital structure ratios dropped.

References

Atrill, P., & McLaney, E. (2013). Accounting and finance for non-specialists (8th ed.). Harlow, UK: Pearson Publishing.

Hackensack University Health Network. (2015). Consolidated financial statements December 31, 2015 and 2014. Web.

Exhibit

Balance sheet

Income statement