Introduction

Integration in a given firm and/or industry refers to the process of organizing production based on organizational unification as well as technology of different production processes. The management of any given firm should employ a method of integration which offers the specific company technological efficiency. A firm is said to be technologically efficient if it produces a certain quantity of output by employing the lowest amount of production factors and / or inputs. Integration method employed should also offer a given firm economic efficiency. Economic efficiency is the ability of a given company to produce a specific output level using the lowest possible costs. Production can be organized in three different ways (Craig and Campbell, 2005, p. 114).

Firms diversify in various means. They integrate vertically, horizontally or agglomerate. Vertical integration involves mergers of firms in the vertical; line of production. A firm can merge with other firms up or down the line of production. Mergers up the line of production are called forward vertical integration while mergers down the line of production, the backward vertical integration. Horizontal integration involves mergers between firms at the same level of production.

Conglomerate integration involves the merging of companies in different line of production. The benefits of the above diversification methods are that firms are able to improve their performance hence growth and increase in capacity. They increase their market shares, synergies, and due to large-scale production, they realize economies of scope and economies of scope. Low production costs lead to maximized profits. This study examines the impact of mergers and acquisition on the performance of Santander Group of banks between 2002 and 2010.

Santander Group

Banco Santander SA is a multinational corporation that operates n many countries including Spain, U.S., UK, EU and other countries. The group provides many financial products to its clients. The company operates in four main segments that are UK, Sovereign, Latin America and Europe. The bank is involved with business in retail banking, wholesale banking, insurance and management of assets. The bank began its operations as a small business entity and expanded to become the present multinational corporation with many branches in different countries.

Literature Review

Mergers and Acquisition

According to Rajeev and Yun (2009, p. 3), diversification is the process through which an organization enters new processes of business in the market with the possibility of manufacturing new products. Mergers and acquisitions are a form of entry that a firm may use to enter a market. Many firms in the financial industry have utilized this means to enter new markets. Mergers and acquisitions can take the form of vertical integration, horizontal integration or conglomerates. Horizontal integration is a form of integration in which firms combine at the same stage of production.

Ison and Griffiths (2001, p. 75) note that horizontal integration may help a certain company to increase their share value. Firms that undertake horizontal integration do benefit from economies of scale that result from capacity expansion, technical economies of scale, social economies of scale, financial economies of scale, marketing and managerial economies of scale.

Vertical integration is the ability of the firm to own subsidiaries downstream and upstream it line of production. Vertical mergers involve backward and forward linkages in an industry. Backward vertical integration occurs when firms merge or acquire subsidiaries that supply it inputs. Firms that undertake vertical integration realize reduced transaction costs hence increased profitability.

Conglomerate integration occurs when an enterprise combines with other companies, which operate in different line of production. Companies Conglomerate to diversify their portfolio and hence spread the risk. These types of diversification are not common in the banking and financial industry. The most common types of mergers and acquisition in the banking industry are horizontal diversification where banks merge with other banks in other countries.

Financial institutions such as banks do diversify through mergers and acquisitions because of many reasons. Banks can diversify with the aim of increasing their financial performance, exploiting the available business opportunities or other reasons. According to Shimizu, et al. (2004, p. 341), financial institutions may be influenced by the profit that their competitors are making in the global industry to engage in mergers and acquisitions. Diversification in form of mergers and acquisitions can enable banks to exploit many opportunities in the global economy. For instance, the advance in technology has enabled firms to be managed from different places cheaply.

Therefore, banks can undertake mergers due to the ability to management subsidiaries from far. Other reasons for mergers and acquisitions include ability for growth, need to reduce operating costs and increased competition in domestic market. In a study conducted by Badreldin & Kalhoefer (2009, p. 5), it was established that banks that participated in mergers and acquisitions increased their financial performance. Despite these findings, the study also established that integration is costly when integrating firms have dissimilar terms of loans and size strategies among other factors.

According to Altunbas & Marques (2008, p. 15) the ability of a strategic fit is an important element in determining the success of mergers and acquisitions in terms of performance. It is important that merging banks have similarities in their balance sheets. A survey by Altunbas & Marques (2008) to measure the importance of strategic similarities in mergers and acquisitions indicates that the size of the bank is important in determining the post merger performance of the bank.

A large size for a domestic merger compared to the size of the bidder results in lower post merger performance. However, for cross border mergers, a large size for the target firm is important because it results in high post merger performance for the bank. Empirical literature indicates that a high pre-merger return on capital has a negative effect on the performance of the bank after the merger both for domestic mergers and cross border mergers. Therefore, banks that perform well before the merger may not be able to improve their performance after merging because their base rate of performance was initially high.

The analysis of efficiency of banks measured in terms of cost to income ratio indicates that they are counter productive in performance perspective. This is due to the difficulties that banks face in integrating the different their cost structures that are different in the short term. According to Altunbas & Marques (2008, p. 17), the differences in capital structure between the merging banks enhances the post merger performance. Capital structure differences for cross border merger is useful at low performance levels. It is difficult for banks involve din cross border mergers to integrate institutions with capital structure that are different. Return on earnings (ROE) is usually positive after mergers.

Recent History of Mergers and Acquisitions

Mergers and acquisitions can be traced to many years ago when companies began integrating at different levels. Since mergers have occurred in different periods and involving different levels of capital, the mergers are known by their history. There are five merger waves with the fifth having occurred in the 1990s. The first merger wave occurred between 1897 and 1904. This fist merger was characterized by the transformation of firms from small firms to large dominant corporations. The first wave occurred about ten years after passing the Sherman antitrust act. The courts had a difficult time in interpreting the act leading to lack of antitrust enforcement. However, the situation changed in 1914 when the Federal Trade Commission was established.

The second wave of mergers occurred between 1916 and the first economic down turn in 1929. Horizontal integration was very common during this phase leading to increased oligopolies. The phase ended with the market downturn. The third wave of mergers was witnessed between 1965 and 1969. The phase witnessed conglomerate acquisitions that were witnessed because organizations wanted to expand but were limited by antitrust laws. The fourth wave of mergers was witnessed in the 1980s while the fifth was realized in the 1990s. All of the merger and acquisition waves happened during periods of economic expansion while they ended during period of economic slump.

The current conditions for mergers and acquisitions are still the same. However, there are challenges that affect the merging firms. Firms have mismatch in expectations. As one firm may expect the valuation of the firm after a merger to rise, the other may be expecting the valuation to decrease. The business environment is still risky and raising enough capital for carrying out mergers and acquisitions is challenging. Since financial institutions are valued highly, raising enough capital for acquisition of a given company is challenging. In the U.S and other countries such as India, the Post poll policies affect mergers and acquisitions.

Firms are uncertain of the policies after elections and therefore, the rate of mergers and acquisitions is affected. Major legal challenges facing mergers and acquisition in the world today are issues related to regulation, tax liabilities and guidelines to pricing.

Santander Group has always utilized mergers and acquisitions to exploit the existing opportunities in the banking industry throughout the world. The recent history of Santander group mergers and acquisitions include the acquisition of Banco Santiago in 2002, acquisition of Italian consumer finance company in 2003, Abbey National bank in 2004 and a merger with Sovereign Bancorp in 2005. In 2007, the bank merged with Fortis SA/NV and The Royal Bank of Scotland Group plc to acquire ABNAMRO Holdings. In 2008, the bank bought British mortgage bank Alliance and Leicester plc. The bank was also nationalized in Venezuela in 2008.

As the effects of the global economic crisis was being felt over the world, the bank managed to acquire some insolvent banks such as Bradford & Bingley’s client deposits (Banco Santander, 2010). In 2009, the bank sold part of its Brazilian unit while in 2010 the bank bought back 24.9% of Santander Mexico from the Bank of America. From all these mergers and acquisitions, the bank exploited banking and business opportunities in different countries.

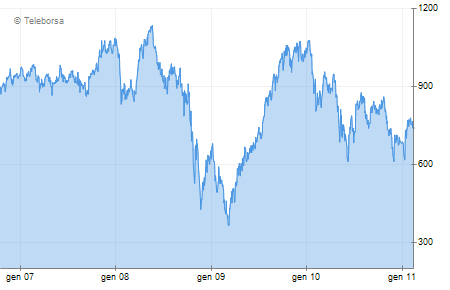

The long-term performance of the stock of the bank has been good since 2002 to 2010. The performance of the stock of the company as indicated in the graph below shows that the stock of the bank performed well until the year 2009 when the stock price decreased. It seem that the stock price of the bank is improves when the merger has a positive impact on the performance of the bank and decreases when the bank performance is poor due. This is the reason for the low fluctuations in the stock price. However, the large decrease in the share price in 2009 can be attributed to the global economic crisis rather than mergers and acquisitions.

Empirical Support

Mergers have always led to better performance of involved companies. According to Altunbas & Marques (2008), banks that diversify through mergers and acquisitions usually perform better. Empirical evidence from Santander Group corresponds to these findings from past studies. To prove the impact of mergers and acquisitions to the performance of banks, this study will analyze five ratios from the bank.

Efficiency Ratios

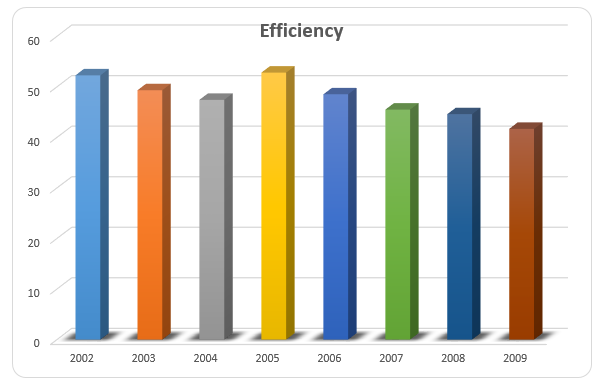

The efficiency ratios indicate the level of receivable in an organization, the repayment period, equity usage and the use of machines and inventory in the bank. The Santander Group has been involved in many mergers over a period. Since 2002-2009, the bank has realized fluctuating efficiency even after mergers and acquisitions. From the table below, the efficiency of the Santander group has been fluctuating over years. Efficiency of the bank decreased consecutively since 2002 from 52.28 to 47.44 in 2004. However, efficiency of the bank began to increase again in 2005 after the Santander Group merged with a U.S. bank Sovereign Bancorp. However, the subsequent mergers and acquisition that were made by the bank did not improve the efficiency further, but led to its gradual decrease from 52.82 in 2005 to 41.7 in 2009.

Table 1.

Return on Assets ratios

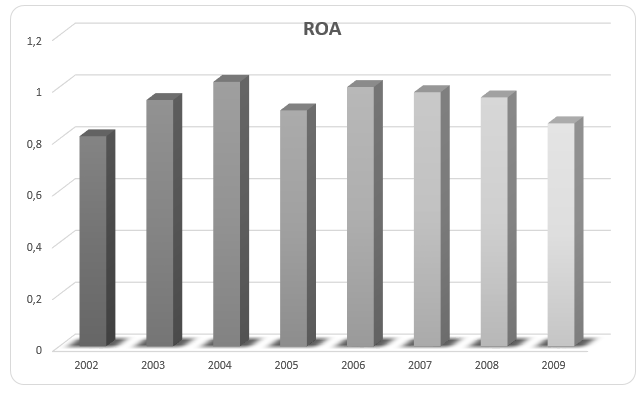

The return on assets ratio indicates the profitability of the bank when compared to the assets of the firm.

The return on assets ratio indicates that initial mergers made by the bank in 2002 and 2003 led to increased performance of the bank. The return on assets increased from 0.81 in 2002 to 1.02 in 2004. However, the merger of the bank in 2004 led to reduced performance in 2005 as is indicated by reduced return on assets. The ration rose to 1.0 in 2006 and then declined again gradually to 0.86 in 2009.

Gross Profit Margin

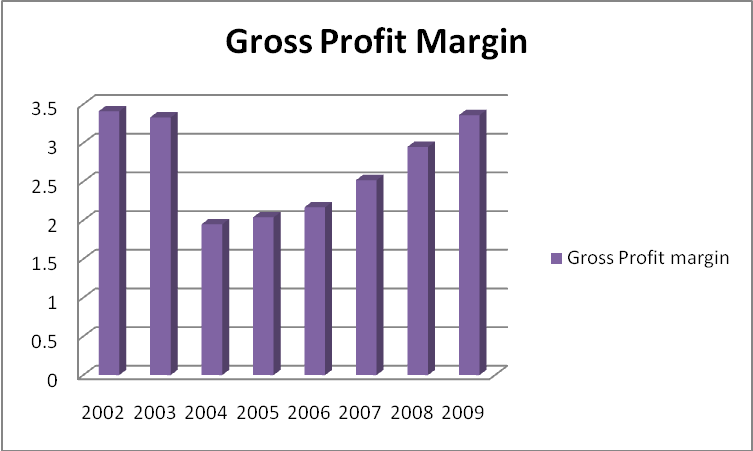

The gross profit margin indicates the profitability of an organization. The gross profit margin of Santander as indicated in table 1 fluctuated for the eighth years between 2002 and 2010. The ratio fell from 3.41 in financial year 2002 to a low of 1.95 in 2004 and began to rise again to a high of 3.36 in 2009. The fall and rise in the ratio indicates that initial mergers did not help in improving the profit of the company. However, subsequent mergers helped the company improve its profit.

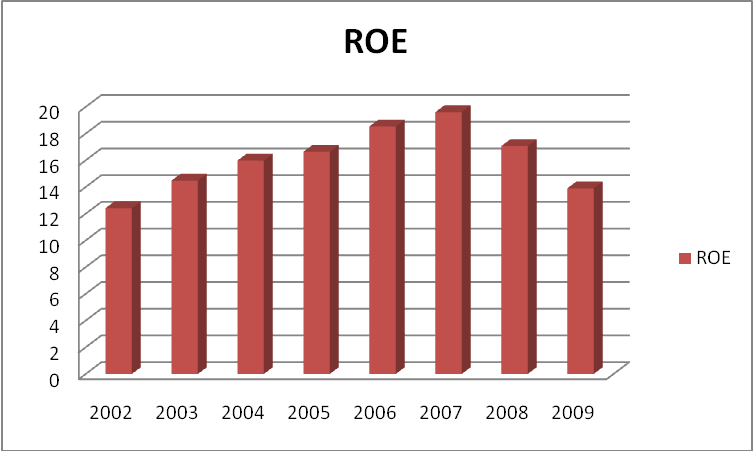

Return on Earnings

This ratio measures the income that the bank realizes on invested shareholders’ equity. Fig. 3 below provides the return on equity ratio for Santander Group since the year 2002. From the figure, it is clear that the mergers and acquisitions that the bank made led to the increase in performance that in turn led to increased return on investors’ equity. Return on equity rose from 12.42 in 2002 to 19.61 in 2007 before declining to 13.9 in 2009. The increase in the ration can be attributed to the mergers made by the bank during the period 2002 to 2006.

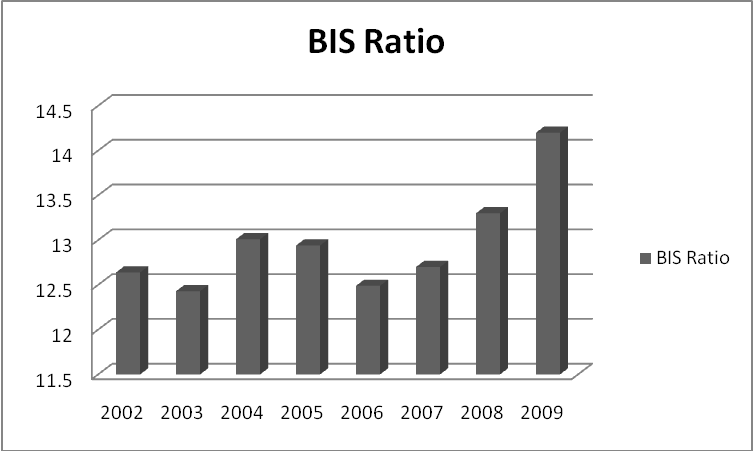

BIS Ratio

The solvency of a given financial institution such as bank is given by the BIS ratio. The ratio provides the capital of the bank that is risk bearing and the risk weighted assets. The BIS ratio is an international standard that measures the stability assets and capital of internationalizing banks. The ratio maintains a balance between assets and capital.

The BIS ratio for Santander Group decreased from 12.64 in 2002 to 12.43 in 2003 before increasing to 13.01 in 2004. The ratio then continues to increase in subsequent years reaching a high of 14.2 in 2009. This indicates that although some mergers led to the decrease in the solvency of the bank, later mergers and acquisitions that were conducted by the bank led to increased solvency of the bank by increasing its capital adequacy.

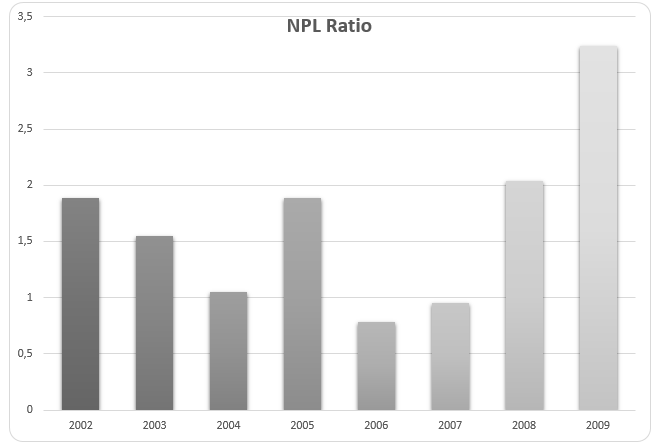

Non-Performing Loans Ratio

This ratio measures the level where loans are at default due to lack of performance. The ratio for the Santander group fluctuated over time. It initially reduced from 1.89 in 2002 to 1.05 in 2004 only to increase again to 1.89 in 2005, 0.78 in 2006 and 3.24 in 2009 (see table 1).

Non-Performing Loans Coverage ratio

The NPL coverage ratio measures any loss that a bank may realize resulting from loss of non-performing loans. The ratio is calculated by the division of probable non-performing loans by the total non-performing loans of the bank. The NPL coverage ratio of Santander has been improving over years especially since 2002 to 2009. The ratios was 139.94 in 2002 and it kept on improving to as low as 75 in 2009 (see table 1). The reduction in the ratio indicates the positive effect of mergers that have led to reduced loss that the bank could suffer from non-performing loans.

Conclusion

Santander Group bank has been involved in various mergers and acquisitions as outlined in the study. In all the mergers, the bank sought to exploit the available opportunities in the business environment in the banking industry. although some barriers such as insufficient capital has affected the merging and acquisitions of the bank leading to the sale of some of its subsidiaries, the group has always managed to come back and merge with other banks.

The above ratio analysis indicates that mergers and acquisition of Santander Group had some effect on the performance of the bank. Santander Group has been involve din a number of mergers and acquisitions that have led to improved financial performance of the bank. Just as the literature review indicated that mergers and acquisition could lead to improved performance of the firm, the empirical findings of Santander group confirmed the findings. The ratios analysis indicated that not all mergers could improve the financial performance of the bank. While some mergers led to improved profitability performance that is designated by increased ROE, ROA and solvency, some mergers can lead to reduced performance indicated by fluctuating efficiency. In conclusion, mergers and acquisition lead to improved performance of an organization.

References

Altunbas, Y. & Marques, D. 2008. Mergers and acquisitions and bank performance in Europe: The role of strategic similarities. Journal of Economics and Business, 60(3). 204-222.

Badreldin, A. & Kalhoefer, C. 2009. The Effect of Mergers and Acquisitions on Bank Performance in Egypt. German University in Cairo, Working paper No. 18.

Banco Santander, 2006. Key Group Figures. Web.

Banco Santander, 2010. Spain Bank Merger and Acquisitions (Banco Santander). Web.

Craig, T. & Campbell, D. 2005. Organizations and the business environment. London, UK: Butterworth-Heinemann.

Ison, S. & Griffiths, A. 2001. Business economics. London, UK: Heinemann publishers.

London Stock Exchange, 2011. Banco Santander S.A. Web.

Rajeev, S. & Yun, Z. 2009. Benefits and Costs of Diversification for Firms in Chapter 11. Web.

Shimizu, K. et al. 2004. Theoretical Foundations of Cross-Border Mergers and Acquisitions: A review of Current Research and Recommendations for the Future. Journal of International Management, 10, 307–353.